![China's Brain-Computer Interface Revolution: Why the West Is Falling Behind [2025]](https://tryrunable.com/blog/china-s-brain-computer-interface-revolution-why-the-west-is-/image-1-1771778583584.jpg)

China's Brain-Computer Interface Revolution: Why the West Is Falling Behind [2025]

Elon Musk keeps talking about Neuralink like it invented brain-computer interfaces. Meanwhile, China's building an actual industry.

It's not hype. It's not marketing. Over the past 18 months, something genuinely different has been happening in Shanghai, Shenzhen, and Beijing. Dozens of startups are moving BCIs from research papers into operating rooms. Government agencies are setting reimbursement rates. Hospitals are running trial after trial. Investors are writing checks that actually clear.

This isn't the story tech media tells. The narrative usually goes: "Neuralink is pioneering BCIs." But that's like saying American space companies pioneered rockets because Elon's talking about Mars while China quietly built a space station.

What's happening in China right now represents a fundamental shift in how emerging technologies scale. And if you're building anything in neurotechnology, artificial intelligence, or biomedical devices, this matters.

Let me walk you through exactly why China is winning this race, what the market looks like, and what it means for the next decade.

TL; DR

- China's BCI market grew 68% year-over-year, reaching 17 billion by 2040. According to a report by Whalesbook, this growth is driven by strategic government policies and rapid commercialization.

- Four specific factors (policy, clinical resources, manufacturing, investment) are creating advantages that Western companies can't easily replicate. SL Guardian highlights these factors as pivotal in China's BCI industry expansion.

- Over 50 implantable BCI clinical trials have been completed in China, with the first fully wireless trial on record after Neuralink. TechBuzz reports that China's clinical trial completion rate far exceeds that of Western companies.

- Insurance coverage is expanding rapidly, with provinces like Sichuan and Zhejiang already pricing BCI procedures, dramatically shortening commercialization timelines. As noted by TechCrunch, this rapid insurance integration is a key factor in China's BCI market acceleration.

- The market is shifting from pure R&D to actual deployment, meaning profitable companies will exist in China before most Western startups even finish their first FDA trial.

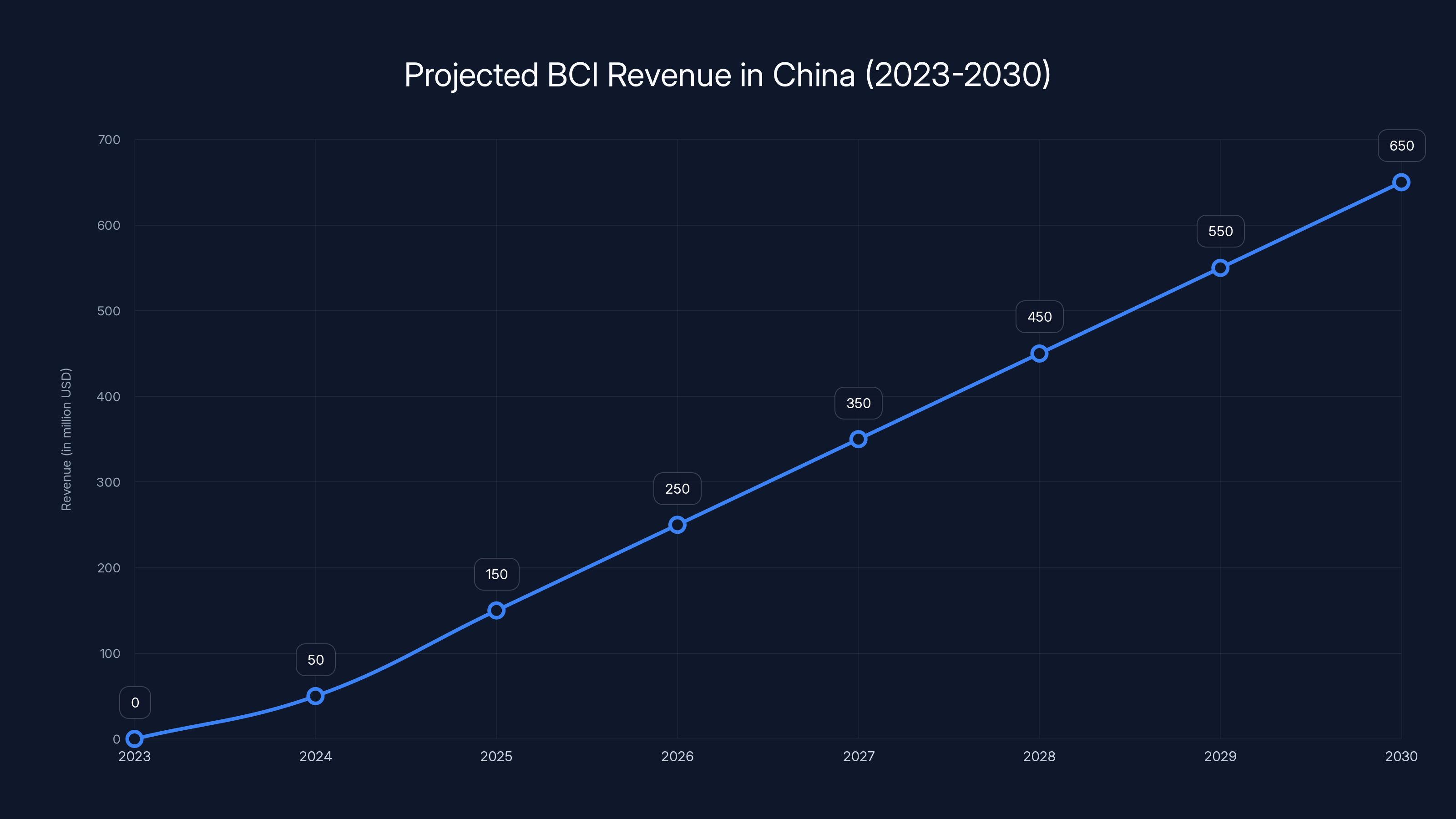

Chinese BCI companies are projected to grow from zero revenue in 2023 to $650 million by 2030, driven by healthcare applications. Estimated data.

The Gap Between Narrative and Reality

Here's what most people don't understand about BCIs: they're not one technology. They're dozens of approaches to the same fundamental problem.

You can implant electrodes directly into brain tissue (invasive). You can place them on the scalp (noninvasive). You can use ultrasound to read neural activity without cutting anyone open (novel). You can decode movement, language, intention, emotion, memory. The applications span paralysis recovery, stroke rehabilitation, treating seizures, managing pain, and eventually enhancing cognition.

When Neuralink shows videos of a paralyzed patient moving a computer cursor with their thoughts, it's impressive. It's also one very specific technology solving one very specific problem.

Meanwhile, Chinese companies are building a portfolio approach. Neuro Xess focuses on flexible implants. Gestala specializes in ultrasound-based interfaces. Neuracle works on noninvasive systems. Brain Co has pivoted to bionic limbs integrated with BCIs. Zhiran Medical targets stroke recovery. Bo Rui Kang Tech is working on spinal cord injury applications.

Instead of one moonshot company, you've got an ecosystem where different teams are making progress on different fronts simultaneously. That's how you scale an industry.

The difference shows up in the numbers. By mid-2025, Chinese companies had completed over 50 clinical trials with implantable BCIs. Think about what that means. Fifty different proof points. Fifty different datasets. Fifty different clinician relationships. Fifty different pathways to regulatory approval.

Neuralink has completed one trial. Synchron has completed a handful. The math here isn't complicated.

Factor 1: Government Policy as a Competitive Advantage

Western tech companies love to complain about government regulation. And they're right that regulation can slow things down. But there's another side to that equation: government support can accelerate things dramatically.

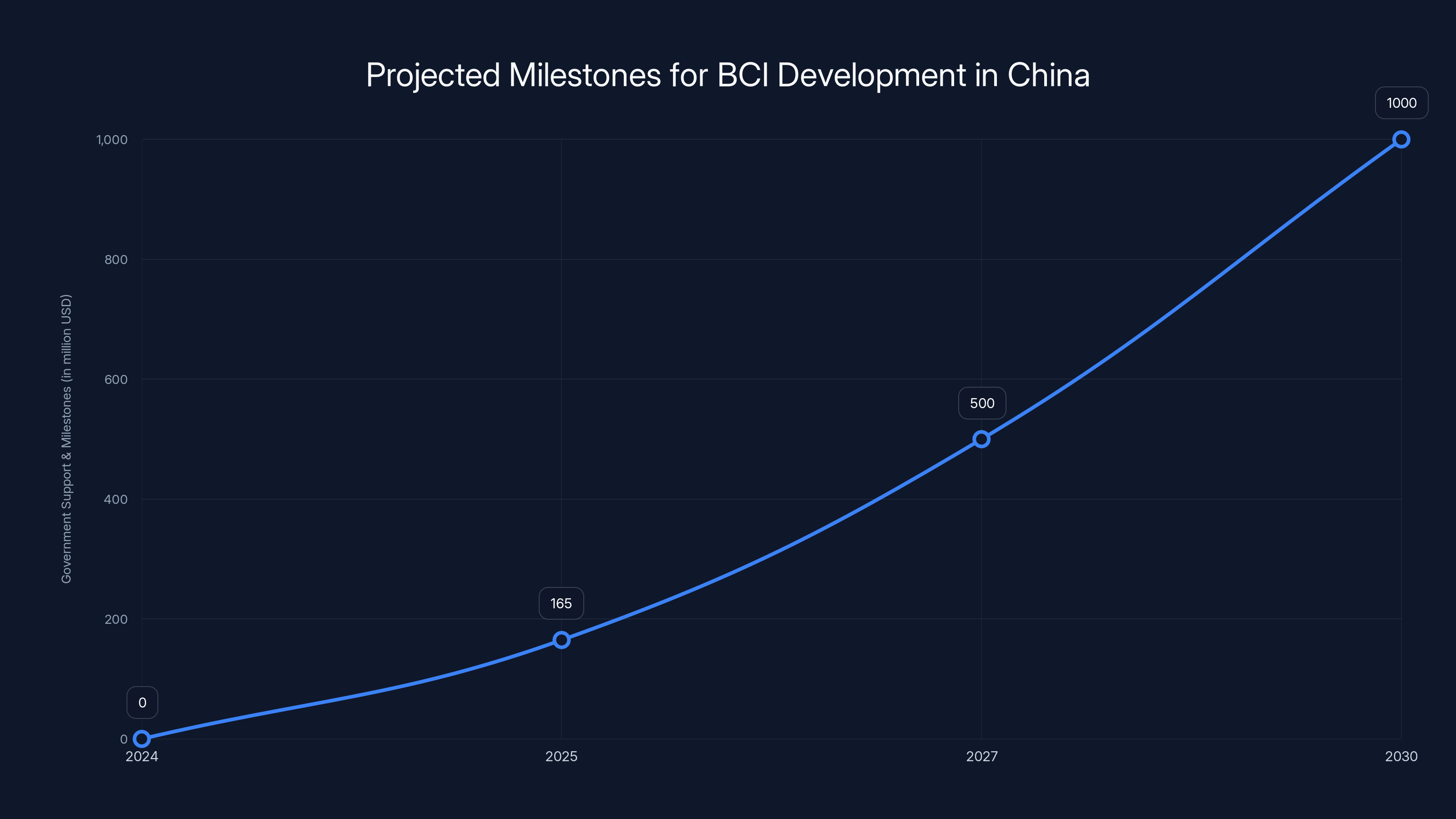

In December 2024, China's Ministry of Industry and Information Technology, along with six other government agencies, released a coordinated national roadmap for BCI development. This wasn't a suggestion. This was a multidepartment commitment spanning technical standards, manufacturing coordination, clinical guidelines, insurance reimbursement, and supply chain development.

The stated targets were specific: major technical milestones by 2027, industry-wide standards by that same year, and a complete domestic supply chain by 2030. The goal wasn't just to support companies. It was to build globally competitive BCI companies.

Then in December 2025, at the Shenzhen BCI & Human-Computer Interaction Expo, the government announced an 11.6 billion yuan fund ($165 million USD) dedicated to supporting BCI companies from early research through commercialization.

Let that sink in. That's not venture capital. That's not dilutive equity. That's government money moving through designated channels to push an entire industry forward.

But here's the part that actually matters: provincial governments started setting medical service pricing for BCIs. Sichuan province. Hubei province. Zhejiang province. These aren't suggestions. Once a province prices a procedure, hospitals can bill for it. Once hospitals can bill, insurers get involved. Once insurers are involved, the procedure moves toward the national health insurance system.

This is radically different from how it works in the US. In America, after the FDA approves a device, you still need to convince private insurers to cover it. Each major insurer makes its own determination. Each determination takes months or years. You might have FDA approval before you have insurance coverage. Some devices never get covered even though they're legal.

In China's system, once the government approves something and prices it, insurance coverage follows almost automatically. This compresses the timeline between "we have regulatory approval" and "we have customers paying us" from 24 months to maybe 6 months.

There's also something subtler happening here. When government is coordinating standards across multiple departments, companies don't waste energy fighting regulatory battles that shouldn't exist. One team at one company doesn't need five lawyers to understand the clinical pathway. The pathway is published. Everyone knows the rules.

This reduces what economists call "regulatory friction." And regulatory friction is a silent cost that most people don't account for. It's not just the cost of compliance. It's the uncertainty. The back-and-forth. The "we need to talk to legal about whether this is even allowed." All of that disappears when government has already coordinated the answer.

Clinical trials in China can be conducted at approximately 20% of the cost compared to the US, enabling more trials and faster data collection. (Estimated data)

Factor 2: Clinical Infrastructure That Actually Scales

Here's something that rarely gets discussed in tech coverage: clinical trials are hard in the US because people are sick and hospitals are expensive.

China has something different. It has a massive population, centralized healthcare system, lower cost of operations, and government capacity to prioritize BCI trials within that system.

This creates three specific advantages:

First, patient recruitment. When a government health system decides to run BCI trials, hospitals nationwide can participate as a coordinated network. Patient recruitment doesn't mean finding people willing to volunteer. It means integrating BCI trials into the standard clinical pathway for paralysis, stroke, and spinal cord injury.

In the US, a startup running a BCI trial needs to convince individual hospitals to participate, then recruit individual patients, then negotiate individual insurance coverage questions. It's sequential and fragmented.

In China, a company can work with the healthcare system to integrate trials across dozens of hospitals simultaneously. The scale is incomparable.

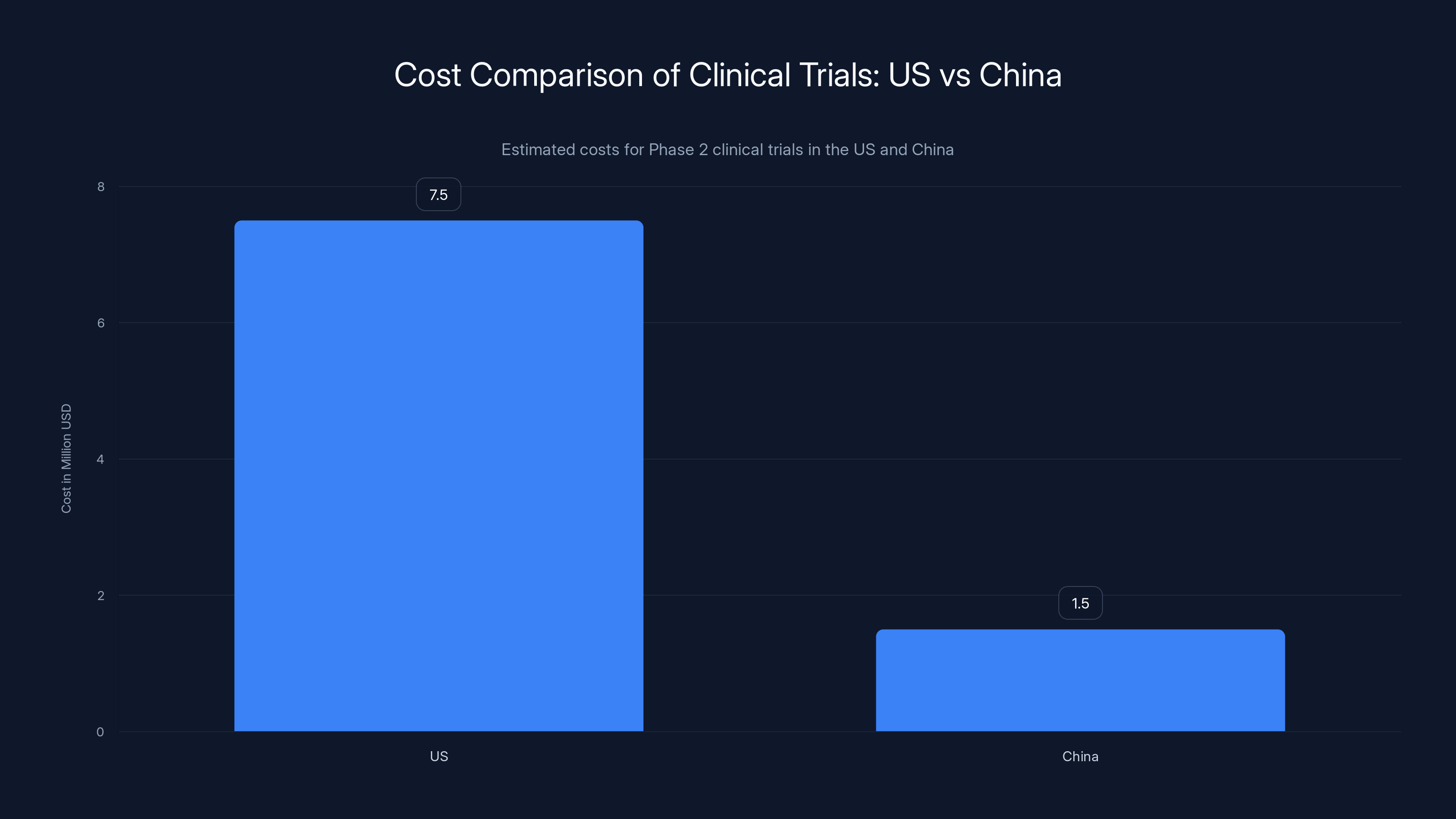

Second, cost structure. Clinical trial operations in the US are expensive. Salaries are high. Facility costs are high. Regulatory overhead is high. A Phase 2 trial might cost $5-10 million.

The same trial in China, with the same number of patients and similar quality standards, might cost $1-2 million. That's not cutting corners. That's the difference in operating costs.

If you can run clinical trials at 20% of the cost, you can run five trials for what one trial costs elsewhere. More data. More evidence. Faster learning.

Third, regulatory speed. Once a trial completes in China, regulatory approval typically follows within months, not years. The data review process is faster. The decision timeline is faster. The entire cycle moves quicker.

This matters because time is money in drug development. Every month a trial extends costs money. Every month approval delays costs money. Shave six months off the timeline and you've saved millions.

Accumulate this across 50 trials and you're looking at a fundamental efficiency advantage that compounds over years.

Factor 3: Manufacturing Capacity That Already Exists

The semiconductor industry taught us something important: you can't build a world-class tech sector without world-class manufacturing.

China already has this across semiconductors, biomedical devices, and advanced materials. This isn't aspirational. Companies have been manufacturing medical devices at scale there for 20 years.

What does this mean for BCIs? It means companies can move from prototyping to manufacturing without building entirely new facilities or supply chains.

Want to manufacture flexible electrode arrays? There are already companies doing this for other medical applications. You're not starting from zero.

Need to source specialized semiconductors? China has vertically integrated semiconductor manufacturing specifically designed to serve medical device companies. Lead times are shorter. Costs are lower. Quality control is established.

Require custom materials for electrode coatings? Materials science companies are available and experienced.

This sounds mundane compared to the AI and software hype, but it's actually what separates companies that stay in the lab from companies that scale. Neuralink builds implants. Manufacturing those implants at scale? That's the hard part.

China's advantage here isn't that it has "cheaper labor." That's outdated thinking. The advantage is that the entire ecosystem for precision biomedical manufacturing is already optimized and operational.

A Chinese BCI startup doesn't need to reinvent manufacturing. It needs to adapt existing capabilities. An American startup basically needs to build manufacturing from scratch.

That's a 3-5 year head start.

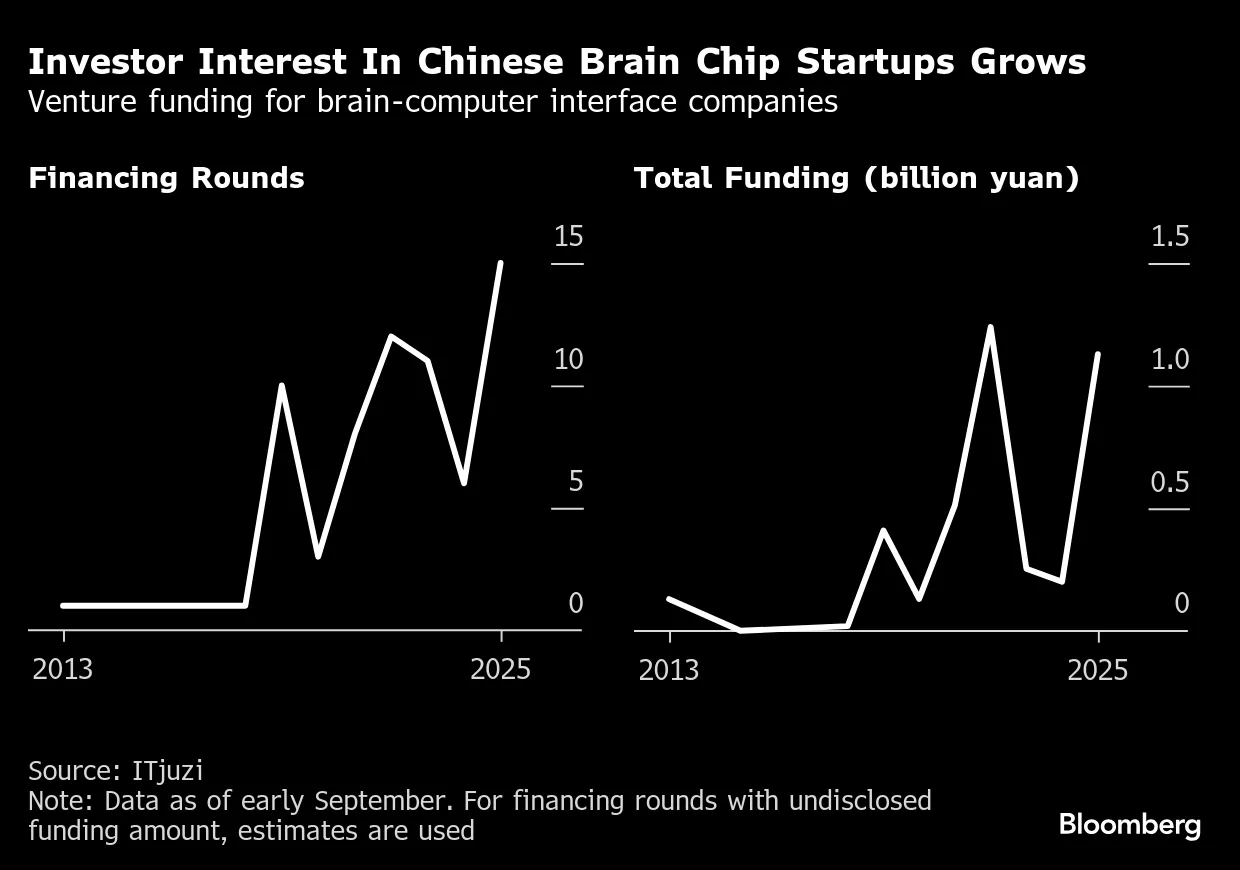

Factor 4: Strategic Investment Creating Real Momentum

When government puts money on the table and shows commitment, private investors pay attention. This isn't unique to China, but the scale here is notable.

In February 2025, Shanghai-based Stair Med Technology closed a $48 million Series B round (350 million yuan). This wasn't a seed stage company. This was a company that had already raised money, completed trials, and had enough traction to get institutional investors excited.

Brain Co, developing noninvasive BCIs and bionic limbs, raised $287 million earlier in 2025. The company subsequently filed for a Hong Kong IPO, which would make it one of the first BCI companies to go public anywhere in the world.

These aren't small rounds. These are serious institutional bets that the market will exist and will be large.

Why does this matter? Because investment capital determines speed. If you're raising money at standard US venture rates (18-24 months between rounds, steep dilution, contingent on hitting specific milestones), you move more slowly. If you're raising capital in an ecosystem where investors are bullish and capital is flowing, you move faster.

Faster capital means:

- Faster hiring

- More simultaneous projects

- Quicker pivots when needed

- Higher burn rate, which drives urgency

- Better talent acquisition (more money means better offers)

Over a 5-year period, a company funded aggressively will accomplish 2-3x what a company funded conservatively accomplishes. Not because the conservative company is worse. Because time compounds.

The other thing happening is state-led venture funds are mixing with private capital. This reduces downside risk for traditional VCs. A successful round has state participation, which implies the government is committed to supporting the sector. That confidence propagates.

China's BCI market is projected to grow from

The Technology Split: Two Paths Forward

Understanding the Chinese BCI ecosystem requires understanding that these companies aren't all building the same thing.

Invasive BCIs: Electrodes in the Brain

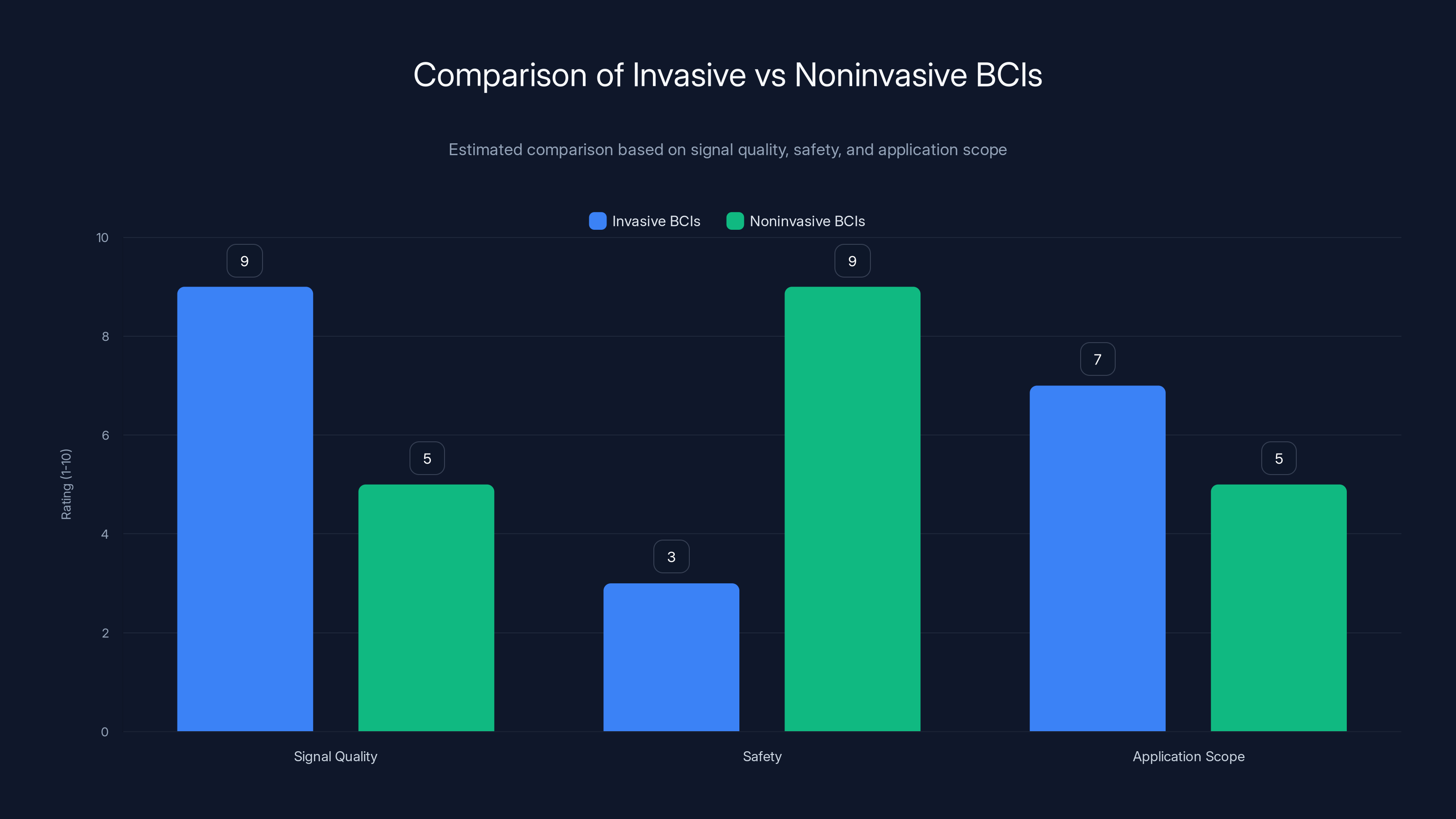

This is the Neuralink approach. You implant electrodes directly into neural tissue, usually in the motor cortex. These electrodes can pick up signals from individual neurons.

Advantages: High signal quality. Precise spatial resolution. Strong decoding performance. You can read from hundreds of neurons simultaneously.

Disadvantages: Requires brain surgery. Always some risk of infection, bleeding, or damage. Electrodes can shift over time. Body recognizes them as foreign objects and can encapsulate them, reducing signal.

Chinese companies doing this: Neuro Xess (flexible electrode arrays), Neural Matrix, Neuracle.

These companies have all completed clinical trials. Neuro Xess specifically has demonstrated long-term stable recordings from flexible implants, which is technically difficult. Most flexible electrodes are flexible in theory but fail in practice because they crack or disconnect.

Noninvasive BCIs: Signals from Outside the Brain

No surgery required. You read neural activity from the scalp or through the skull.

The challenge is that the skull blocks signals. A signal from the motor cortex that registers as strong activity when measured directly at the electrode becomes diffuse and noisy when measured from the scalp. You lose resolution.

Existing noninvasive approaches: EEG (electroencephalography) has been around since the 1920s. It's terrible at spatial resolution but it's safe and non-invasive. f MRI can map neural activity but requires a machine the size of a car. f NIRS measures blood flow as a proxy for neural activity.

None of these have achieved the signal quality needed for practical applications like cursor control or communication at scale.

But here's where it gets interesting. New approaches are emerging. Ultrasound can penetrate the skull better than electrical signals. Gestala, founded by Phoenix Peng, is working on ultrasound-based BCIs. Early data suggests ultrasound can achieve much better resolution than EEG while remaining completely noninvasive.

If ultrasound-based BCIs work as promised, they're a game-changer. You get invasive-level signal quality without the surgery. That's the holy grail.

Other noninvasive approaches under development include optical imaging (shining light through the skull and measuring neural activity from the reflected light), magnetoencephalography (measuring magnetic fields from neural activity), and multimodal fusion (combining multiple signal types to compensate for individual limitations).

The smart money in China is betting on multiple approaches. Some companies will win. Some will lose. But by diversifying bets, the ecosystem improves faster.

Market Size: From Millions to Billions

Let's talk about the financial opportunity because this is where the rubber meets the road.

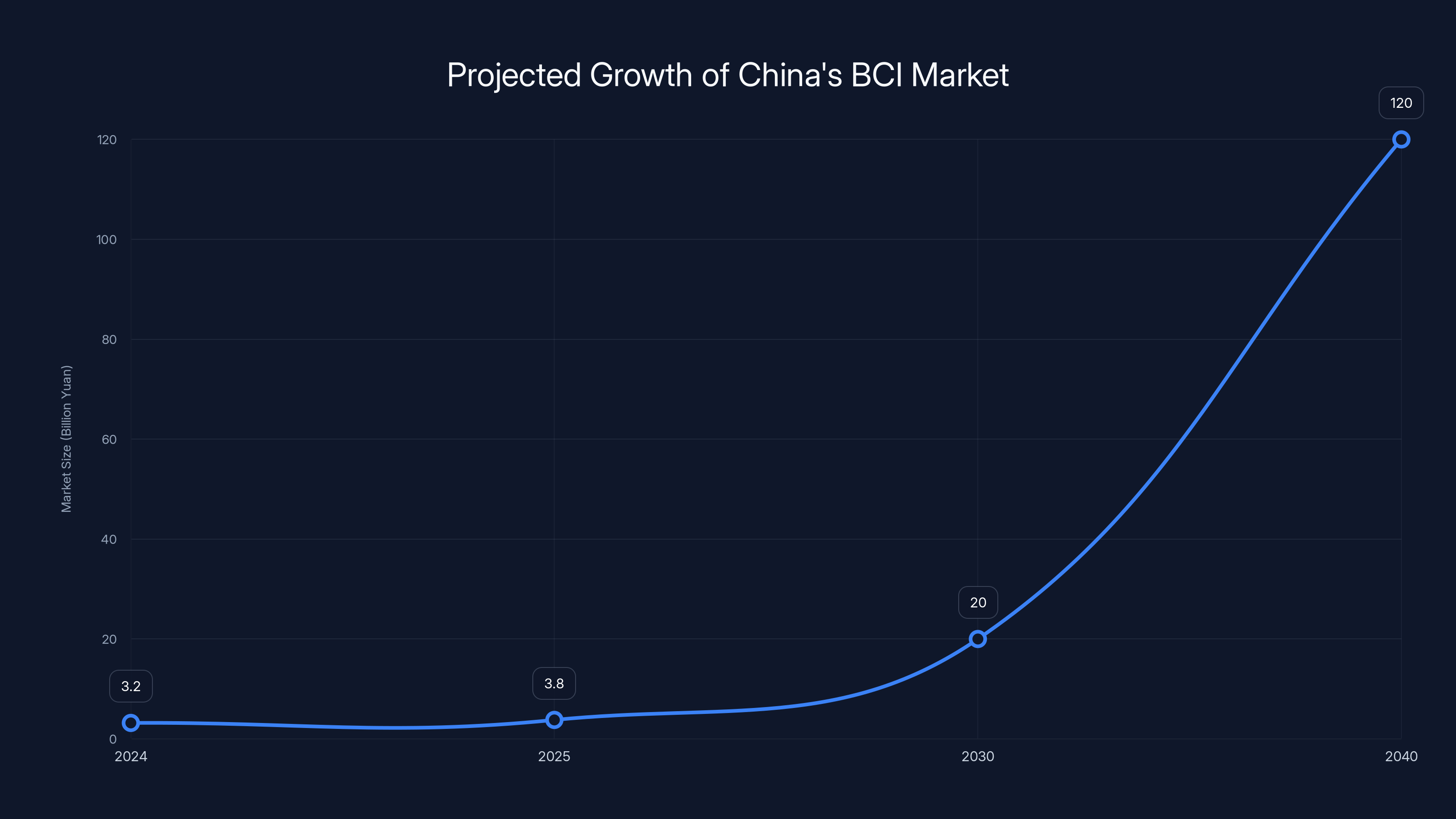

In 2024, China's BCI market was approximately 3.2 billion yuan (roughly

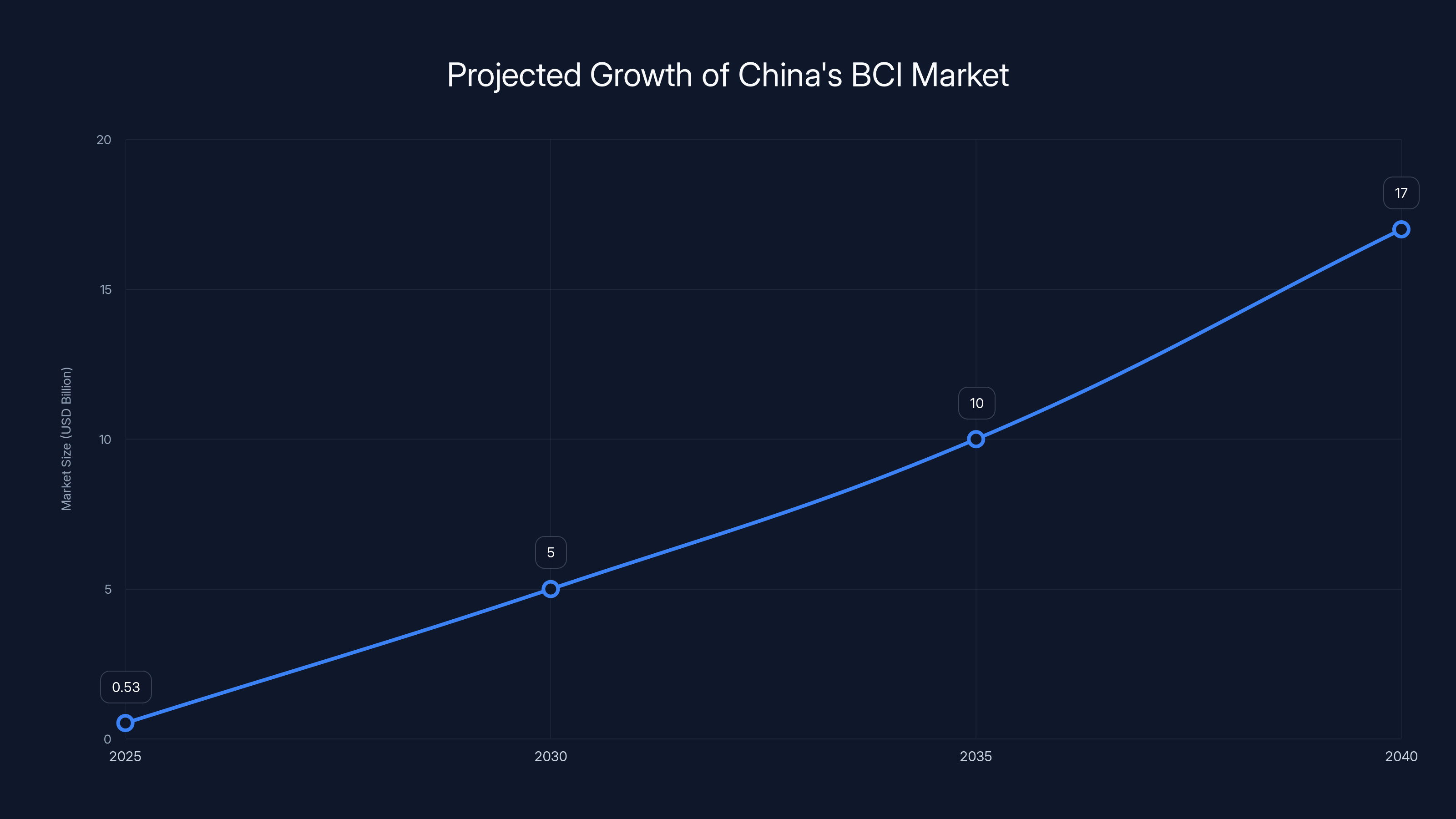

But growth doesn't stay linear when a market moves from research to commercialization. Projections for 2040 put the market at over 120 billion yuan ($17 billion USD).

That's 30+ years of 21% compound annual growth. It's not unrealistic.

Here's why: healthcare markets grow reliably when you have insurance coverage, regulatory approval, and clinical evidence of efficacy. BCIs will have all three in China before 2030. Once that happens, adoption accelerates.

Spinal cord injury alone affects 2-3 million people in China. If BCIs can meaningfully improve quality of life for even 20% of that population, and each treatment costs $50,000-100,000, you're looking at a market in the billions just for spinal cord injury.

Add stroke rehabilitation. Add paralysis from any cause. Add pain management. Add neurological disease management. The addressable market expands rapidly.

The Western market is smaller (US population is 1/4 of China) but wealthier (higher per-patient spending). Europe is smaller still but has higher regulatory barriers. Globally, the BCI market could reach $100 billion by 2040-2050 if technology develops as expected.

If China captures 60% of that market due to being first to scale, that's

This is not speculation. This is basic market math applied to a specific disease category with a large addressable population.

The Companies Building the Future

You probably haven't heard of most of these companies. That's because they don't have celebrity CEOs like Elon Musk. They don't post videos of paralyzed people twitching robot hands. They're just shipping.

Neuro Xess makes flexible implantable electrodes. The technology is advanced. The team has Ph Ds from top universities. They've completed clinical trials. They're raising money and hiring aggressively.

Brain Co is one of the most well-funded Chinese BCI companies. Started in 2015, they've raised over $287 million (2 billion yuan) and are moving toward a Hong Kong IPO. Their focus: noninvasive BCIs combined with bionic limbs. Their bet is that the real value isn't the BCI in isolation but the BCI controlling a physical device that gives people mobility back.

That's a smart insight. The BCI is the interface. The value is the outcome.

Gestala is newer (founded January 2025) and working on ultrasound-based BCIs. The team has published peer-reviewed research on the approach. They're in fundraising conversations with institutional investors. If ultrasound BCIs work, this company could be huge. If they don't work, the company won't exist in five years. High risk, high reward.

Neuracle focuses on noninvasive EEG-based systems. They're trying to push EEG technology beyond what it's traditionally been capable of.

Zhiran Medical targets stroke rehabilitation using BCIs. They understand that the market for "consciousness transfer to robot bodies" is speculative. The market for "help stroke patients regain mobility" is immediate and substantial.

Neural Matrix, Bo Rui Kang Tech, Brainland Tech, and Aoyi Tech are all pursuing variations on these themes with different technical approaches.

What's notable about this list is the diversity. You've got invasive, noninvasive, and hybrid approaches. You've got companies focused on motor control, language, rehabilitation, and enhancement. You've got public companies, well-funded privates, and early-stage startups.

This diversity is exactly how you scale an industry. You increase the probability that at least some approaches will work.

China's BCI market is projected to grow from 3.2 billion yuan in 2024 to 120 billion yuan by 2040, driven by healthcare advancements and increased adoption. Estimated data.

The Commercialization Timeline: It's Closer Than You Think

Most discussions of BCIs treat them as future technology. But the future is already arriving.

Over the next three to five years, Chinese companies expect BCIs to remain concentrated in healthcare. This isn't a bug. It's exactly the right market to pursue first.

Motor restoration (helping people regain movement control) is the most developed application. The clinical evidence is strongest. The patient population is large. The willingness to pay is high. Insurance should cover it.

Stroke rehabilitation is the next major market. Roughly 6.5 million new stroke cases happen in China annually. Maybe 30-40% of survivors have significant lasting motor impairment. BCIs could help millions of people. The treatment cost would be less than lifelong care and assistance. Insurance coverage becomes economically rational.

Spinal cord injury recovery is the third major application. Fewer patients but more severe disability per patient. Treatment willingness is highest here.

These are real markets. Real patients. Real problems that BCIs actually solve. By 2027-2030, I'd expect to see Chinese BCI companies with actual revenue in the $100-500 million range annually.

For comparison, Neuralink has probably $50-100 million in development costs and zero revenue. Chinese companies will have multiple times the clinical evidence and actual paying customers.

That's the difference between being first at something and being first to make it work.

The Western Response: Playing Catch-up

Neuralink is the most prominent Western BCI company, and Elon Musk's involvement gets a lot of attention. But Neuralink is not racing ahead. It's actually moving more slowly than Chinese competitors in terms of clinical evidence.

Neuralink is focusing on one specific problem: restoring communication to completely paralyzed people who can't move or speak. This is a real problem and solving it is admirable. But it's a smaller addressable market than the broader motor restoration space Chinese companies are targeting.

Synchron is also pursuing invasive BCIs but with a different approach (electrodes in blood vessels rather than directly in brain tissue). This might be safer but comes with potential performance tradeoffs. They've completed multiple trials but haven't demonstrated advantages over electrode-based systems.

Paradromics is working on high-channel-count invasive implants. More channels could mean better resolution and more practical applications.

But none of these companies have the clinical trial velocity or market development that Chinese competitors have achieved.

The regulatory environment in the US is also different. FDA approval is thorough and sometimes slow. This is good for safety. It's bad for speed. US companies will likely take 5-7 years from first human trials to actual commercialization. Chinese companies might accomplish it in 3-4 years.

Europe has even stricter standards and stronger emphasis on data privacy. A European BCI startup faces the most difficult regulatory and public opinion environment. But Europe is probably where strong alternative approaches to BCIs will develop. European companies are more likely to focus on privacy-preserving noninvasive approaches than on implantable systems.

The Technical Challenges: Why This Is Actually Hard

All this optimism about Chinese companies shouldn't obscure the fact that BCIs are genuinely difficult technology.

Signal Stability: Electrodes are foreign objects in the brain. The body responds by forming scar tissue around them. Over months or years, this reduces signal quality. Solving this requires either active immunosuppression (which has its own complications) or electrode materials that don't trigger immune response. Progress is happening but it's slow.

Decoding Complexity: The brain uses millions of neurons to create a single action. Extracting intention from that pattern requires sophisticated machine learning. The decoding gets better with more data. But gathering more data requires more trials. More trials take time.

Personalization: Every brain is different. Every patient's neural patterns are different. A decoder trained on one person doesn't work for another person. Companies are solving this through adaptive learning (the decoder updates based on each patient's specific patterns) but it's not simple.

Long-term Reliability: A device that works for a week is proof of concept. A device that works for a year is commercial. A device that works for a decade is transformative. Getting to decade-scale reliability requires years of real-world testing.

Integration with Prosthetics: Decoding neural intent is one problem. Controlling a physical device with minimal latency is another. A 100ms delay between intent and action breaks the sense of agency. Achieving sub-100ms latency while maintaining safety is difficult.

All these challenges are solvable. But they require time, money, and experimentation. Chinese companies have more of all three right now.

Invasive BCIs offer higher signal quality and application scope but are less safe due to surgical requirements. Noninvasive BCIs prioritize safety and are suitable for wider applications, albeit with lower signal precision. Estimated data.

The Integration with AI: The Real Story

Here's the part that most tech coverage gets wrong. BCIs aren't just about restoring lost function. They're about creating a high-bandwidth interface between human consciousness and artificial intelligence.

A normal person interacts with AI through text. You type a prompt into Chat GPT. The model generates text. You read it. This loop takes maybe 30 seconds.

With a BCI, the loop could be instantaneous. You think a question. The AI processes it and returns an answer directly to your visual cortex or language centers. You don't read text. You experience understanding.

This is still theoretical. But it's the direction the technology is heading.

China's advantage here is that the country has advanced AI research alongside advanced neuroscience research. Companies like Gestala, Neuro Xess, and Brain Co are all thinking about how to integrate their BCIs with AI backends.

Neuralink seems focused on the BCI hardware in isolation. That's understandable but potentially limiting. The real value might not be the BCI as a standalone device but the BCI as the interface to advanced AI systems.

If Chinese companies nail this integration before Western companies do, they get a 5-10 year head start on a technology that could become more important than smartphones.

That's not hype. That's just following the logic of where the technology goes.

The Healthcare System Advantage: Why Scale Happens Faster

China's government-coordinated healthcare system creates specific advantages for BCI commercialization that can't be replicated in Western systems.

When a hospital system decides to deploy BCIs, it can integrate them into treatment protocols quickly. Doctors get trained. Referral pathways are established. Insurance covers it. Supply chains are optimized.

In the US, this process is decentralized and slow. One hospital might adopt BCIs. Another hospital waits to see results. Another hospital has different insurance contracts and different coverage determinations. The rollout takes 3-5x longer.

This isn't criticism of the US system. It's just different. More distributed authority creates more flexibility and innovation but slower scaling for established technologies.

For BCIs, speed of scaling matters. The company that reaches 1,000 implants first will have:

- Largest dataset for training AI decoders

- Most clinical evidence

- Strongest relationships with hospitals

- Better brand recognition

- Clearer path to profitability

Being 2-3 years ahead in deployment probably means being 10+ years ahead in market dominance.

Investment Implications: Where the Value Accumulates

If you're thinking about this from an investment perspective, several implications follow:

-

Chinese BCI companies are undervalued relative to Western ones. Investors in the US pay premiums for Neuralink's valuation based on Musk's vision. But Chinese companies have more clinical evidence and faster commercialization timelines. In five years, Chinese companies will have actual profitable operations while Neuralink is still pursuing FDA approval. Valuations should invert.

-

The supply chain companies matter enormously. Companies that supply materials, semiconductors, or manufacturing capacity to BCI firms might be better investments than BCI firms themselves. These supply chain companies have lower technical risk and still benefit from the market growth.

-

The AI integration layer is critical. Companies that figure out how to integrate BCIs with advanced language models or reasoning systems first will dominate. This might not be the hardware company. It might be a software company, an AI company, or a hybrid.

-

Healthcare logistics companies might benefit. As BCIs move to scale, the logistics of getting devices to hospitals, training clinicians, managing supply chains, and handling post-market surveillance become valuable. There's a playbook from other high-end medical devices that applies here.

China's government has set clear milestones to support BCI development, with significant funding and policy initiatives aimed at creating a competitive industry by 2030. Estimated data.

The Path to Human Augmentation: The Real Endgame

All the talk about treating paralysis and stroke is just the beginning. The real trajectory of BCI technology leads to human augmentation.

Imagine a future where:

- Healthy people can augment working memory by connecting their brains to AI systems

- Language learning becomes 10x faster because you can directly interface with language processing systems

- Decision-making improves because you can access information systems in parallel with biological cognition

- Complex problems can be solved through collaboration between human intuition and AI reasoning

This sounds like science fiction. But the technical roadmap is clear. First you build BCIs that work in people with brain damage (proof of concept). Then you make them safer and more reliable (medical applications). Then you make them non-invasive or minimize invasiveness (broader applications). Then you optimize them for cognitive enhancement (augmentation).

Each step is 5-10 years. So we're probably looking at 2035-2045 before BCIs for augmentation are mainstream.

But the companies building the foundation now will be the ones capturing that market. And right now, Chinese companies are building that foundation faster than anyone else.

This is why government in China is investing so heavily. It's not charity. It's recognizing that whoever leads in BCIs in 2040 might lead in cognitive technology for the rest of the century.

Western governments are waking up to this. But waking up is different from acting. By the time US policy catches up to Chinese policy, Chinese companies will have 3-5 years of head start. In technology markets, that's an eternity.

Risks and Uncertainties: Nothing Is Guaranteed

I've spent this article explaining why Chinese BCI companies are winning. But let me be clear: this isn't guaranteed. Everything could go wrong.

Technology Risk: BCIs might not work as well as we think. Long-term electrode stability might prove unsolvable. Decoding algorithms might hit fundamental limits. Integration with AI might be more difficult than expected. If the technology doesn't deliver, market projections collapse.

Regulatory Risk: China's regulatory environment could change. What's fast today could become slow tomorrow. New safety concerns could emerge requiring more testing. Regulatory convergence with international standards could impose Western-level burden on Chinese companies.

Adoption Risk: Even if BCIs work, people might not want them. Surgery risk, implant risk, infection risk. Many paralyzed people might prefer other rehabilitation approaches. The willingness to pay might be lower than projections suggest.

Competition Risk: Western companies might catch up faster than expected. New technologies might emerge that are safer or more effective than implantable BCIs.

Geopolitical Risk: Trade restrictions could limit access to semiconductor components or materials. China might face international pressure on device exports. Tensions between US and China could disrupt supply chains.

None of these are likely to happen. But none are impossible either. Anyone investing in BCIs or betting on this market needs to understand these risks.

Lessons for Other Emerging Technologies

The BCI story in China teaches us something important about how emerging technologies scale in the modern world.

It's not always the most innovative country that wins. It's the country that can:

- Align policy across multiple government agencies

- Coordinate capital (both state and private)

- Build or leverage existing manufacturing

- Create clinical infrastructure for rapid testing

- Establish reimbursement pathways alongside technology development

The US is excellent at innovation. We generate breakthrough ideas. But we're not organized for scaling those ideas. China is organized for scaling.

This pattern will repeat in autonomous vehicles, quantum computing, advanced materials, and other complex technologies. The country that scales first wins the market.

For entrepreneurs, this means that being first with an invention is nice. But being first to scale is what creates billion-dollar companies. If you're building BCIs or similar technologies, think about scale from day one. Don't wait until the technology is perfect. Build the supply chains, regulatory relationships, and manufacturing infrastructure in parallel with the technical development.

What Happens Next: 2025-2030 Timeline

If trends continue:

2025-2026: Chinese BCI companies continue completing clinical trials. First commercial systems get installed in hospitals. Stair Med and Brain Co IPO in Hong Kong or mainland China. US companies are still in early trials.

2026-2027: China's government achieves stated goal of technical milestones and industry standards. Multiple Chinese companies reach $50-100M in annual revenue. First direct brain-to-AI integration systems are deployed in clinical settings. Western companies still in development phase.

2027-2028: Chinese BCI market reaches $2-3 billion annually. Insurance coverage is standard in most provinces. International companies start manufacturing in China or licensing Chinese technology. Neuralink might have FDA approval by now but minimal commercial deployment.

2028-2030: Chinese companies dominate the global BCI market. Market reaches $5-10 billion. First generation of augmentation applications emerge (enhanced memory, accelerated learning). Western companies are now licensing Chinese technology to play catch-up.

This timeline assumes technology develops as expected and regulations don't change dramatically. But it's a reasonable baseline.

The Bottom Line

China's BCI industry isn't "racing ahead" relative to Neuralink. It's multiple steps ahead in clinical development, commercialization planning, and market readiness.

Neuralink is building one impressive technology. Chinese companies are building an industry.

The difference matters. Industries scale. Technologies might not. If you're thinking about neurotechnology, artificial intelligence, or emerging healthcare solutions, watching Chinese BCI companies is watching the future arrive.

The companies, the teams, the applications that will define neurotechnology in 2035 are probably already in China, running trials, closing rounds, and preparing for commercial launch.

Western coverage of BCIs focuses on the celebrity entrepreneurs and moonshot narratives. Meanwhile, actual progress is happening in cities most tech journalists have never visited, with founders no one's heard of, building an industry that will reshape how humans interact with technology.

That's not a story about Elon Musk. That's a story about how technology markets actually develop in the 2020s.

FAQ

What exactly is a brain-computer interface?

A brain-computer interface is a system that reads electrical signals from the brain and translates them into commands that control external devices. This can range from reading motor cortex activity to control a cursor or robotic limb, to reading language centers to decode speech, to reading sensory areas to deliver information directly to the brain. Some BCIs require implanted electrodes for high-quality signals, while others use noninvasive methods like EEG or ultrasound. The core principle is always the same: decode neural activity into actionable information that bypasses damaged biological pathways.

How do invasive BCIs differ from noninvasive approaches?

Invasive BCIs implant electrodes directly into neural tissue, typically in the motor cortex, allowing them to read signals from individual neurons with high precision and spatial resolution. This creates strong decoding performance and control over complex tasks but requires brain surgery with associated risks. Noninvasive BCIs read neural activity from the scalp (EEG), through the skull (ultrasound), or from blood flow patterns (f MRI), avoiding surgery but losing signal quality and resolution. Noninvasive systems trade precision for safety, making them better for early-stage applications and broader populations, while invasive systems are better for applications requiring precise, nuanced control.

Why is China's BCI industry growing faster than Western companies?

China's advantage comes from four factors: strong government policy coordination that sets standards and reimbursement rates, creating fast pathways to commercialization; vast clinical resources including large patient populations and lower trial costs; mature manufacturing infrastructure for semiconductors and medical devices that enables rapid scaling; and strategic investment from both government and private sources. Additionally, China's healthcare system allows for faster adoption once regulatory approval is achieved because insurance coverage follows automatically. Western companies face more fragmented regulatory environments, higher costs, and slower insurance approval processes, which slows commercialization by 2-3 years or more.

What is the addressable market for BCIs?

The immediate addressable market is healthcare applications for people with paralysis, spinal cord injury, stroke recovery, and neurological diseases. With millions of potential patients and treatment costs ranging from

How long until BCIs are widely available?

For medical applications, particularly stroke rehabilitation and paralysis recovery, BCIs should be commercially available in hospitals in China within 2-3 years, with significant adoption within 5-7 years in China and perhaps 7-10 years in Western countries. For noninvasive systems, the timeline could be faster since they don't require brain surgery. For augmentation applications (enhanced memory, learning, cognitive enhancement), expect 10-15 years before they're safe enough and effective enough for widespread use in healthy people. The key bottleneck isn't the technology but regulatory approval and clinical evidence of long-term safety and efficacy.

What are the main risks with BCIs?

Invasive BCIs carry surgical risks including infection, bleeding, and potential neurological damage. Electrode degradation over time can reduce signal quality, eventually requiring replacement surgery. There's also the psychological adjustment to having a foreign object in your brain and the long-term effects of electrical stimulation in neural tissue. Noninvasive systems are safer but have lower signal quality. Privacy and security risks emerge from having a direct brain interface that records neural activity, which could theoretically be hacked or monitored. The biggest unknown is long-term safety and efficacy; most existing trials have been relatively short-term.

Which Chinese BCI companies are the most advanced?

Brain Co is the most well-funded with over

How do BCIs integrate with AI systems?

The integration happens at the software layer where AI algorithms decode neural signals into meaningful commands. As BCIs improve, this integration could become bidirectional, with AI systems sending signals back to the brain to deliver information. Long-term, this could create direct brain-to-AI communication where a person thinks a question and an AI system returns understanding directly to their consciousness, bypassing the need for language or visual processing. This is speculative technology but it's where the field is heading over the next 10-20 years.

What does this mean for Western BCI companies?

Western companies like Neuralink, Synchron, and Paradromics face a more challenging regulatory environment and slower commercialization timeline. They're doing excellent technical work but they're likely to be 3-5 years behind Chinese companies in terms of deployed systems and market revenue. Some Western companies might focus on niche applications or licensing technology from Chinese companies. Others might differentiate through noninvasive approaches or specific medical applications where they have advantages. The challenge is that Chinese companies are well-funded, moving fast, and have government support, making it difficult for Western companies to catch up without major breakthroughs or strategic partnerships.

Key Takeaways

- China's BCI market grew 68% in 2025 and is projected to reach $17 billion by 2040, driven by government policy coordination and fast-track commercialization pathways

- Chinese companies completed 50+ clinical BCI trials by mid-2025 compared to Neuralink's single trial, creating a significant evidence advantage

- Four factors (policy support, clinical resources, manufacturing capability, strategic investment) create a scaling advantage that Western competitors cannot easily replicate

- Insurance coverage and reimbursement rates are being established in Chinese provinces now, compressing the timeline from regulatory approval to revenue by 2-3 years

- The market is transitioning from research to commercialization, meaning profitable Chinese BCI companies will exist before Neuralink achieves FDA approval

Related Articles

- Merge Labs: How Ultrasound Brain Tech Could Redefine Human-AI Integration [2025]

- OpenAI's $250M Merge Labs Investment: The Future of Brain-Computer Interfaces [2025]

- Texas Sues TP-Link Over China Links and Security Vulnerabilities [2025]

- China's Optical Clock Now Defines Global Time: What It Means [2025]

- Fitbit Co-Founders Launch Family Health Tracker: What You Need to Know [2025]

- OpenEvidence's $12B Valuation: Why AI Medical Data Matters [2026]