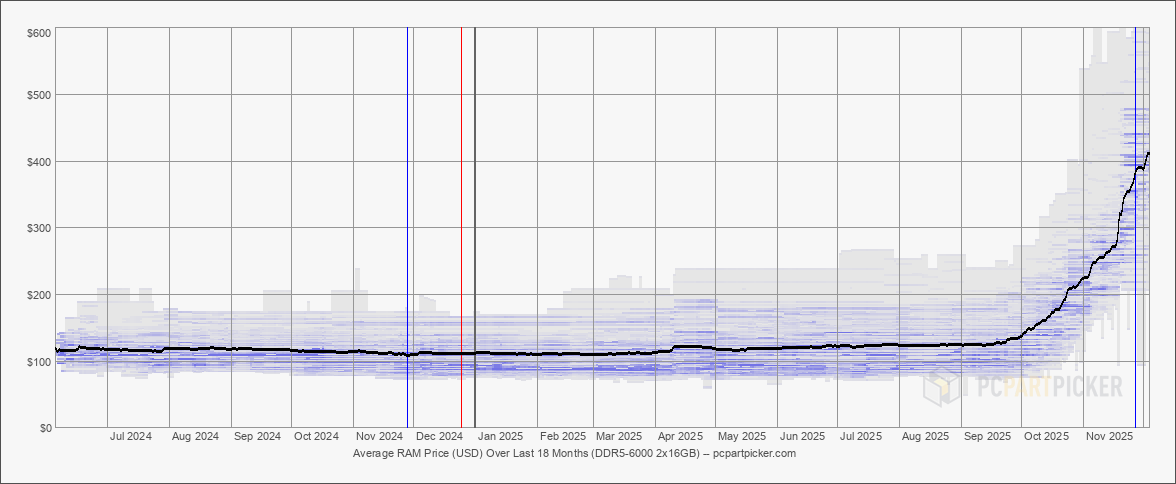

![RAM Crisis 2025: Why Lenovo and the Industry Face Inevitable Price Hikes [2025]](https://tryrunable.com/blog/ram-crisis-2025-why-lenovo-and-the-industry-face-inevitable-/image-1-1771878908992.jpg)

Understanding the RAM Crisis: What's Actually Happening Right Now

You've probably noticed something lately: good laptops are getting expensive. Really expensive. And it's not just inflation or corporate greed. There's a legitimate supply chain crisis hitting the memory chip industry, and it's affecting everyone from Lenovo to Dell to HP. According to Bloomberg, the rampant demand for AI is significantly contributing to this crisis.

Lenovo recently made headlines by essentially throwing up their hands and saying: "We can't prevent price increases in March." This is not CEO talk for "we're optimizing margins." That's a company admitting they've exhausted every option in their playbook, as noted by TweakTown.

The RAM shortage isn't new. We've been watching it develop for months. But what's changed is the resignation in how manufacturers are communicating about it. They're not promising to absorb costs anymore. They're not spinning hopeful narratives about supply normalization. They're just warning customers: prices are going up, and there's nothing they can do about it.

Here's what makes this crisis different from past memory shortages. Previous RAM crunches were usually about temporary bottlenecks. A tsunami in Taiwan. A factory fire. A geopolitical hiccup. These resolved in months, sometimes quarters. But this one? This is structural. The demand for memory chips has fundamentally outpaced production capacity, and the industry can't build factories fast enough to catch up, as detailed in Deloitte's semiconductor industry outlook.

When Lenovo says there's "no way around" price hikes, they mean it. They've locked in higher costs from suppliers. They've negotiated long-term contracts that suddenly look terrible. They're facing a choice between eating massive margin losses or passing the cost to customers. Most companies are choosing the latter.

The timing is brutal. We're heading into spring, when businesses refresh their tech budgets and students need laptops for the next school year. This is exactly when price sensitivity peaks. And instead of promotional pricing, we're getting sticker shock.

The Supply Side Collapse: Why Factories Can't Keep Up

Let's dig into the actual production problem. The RAM industry is dominated by a few companies: Samsung, SK Hynix, and Micron. These three firms control roughly 95% of global DRAM production. When there's a supply problem, it's not like they can quickly pivot to another supplier. These are highly specialized factories with billions of dollars in equipment, as explained by Tom's Guide.

Building a new memory fab takes years and costs $10-20 billion. You don't spin one up to meet temporary demand spikes. So when demand surges, production capacity becomes the hard ceiling that no amount of money can immediately breach.

What's driving demand? Multiple factors are converging simultaneously. AI workloads require more memory than traditional computing tasks. A machine learning training job might need 64GB to 256GB of RAM. Consumer interest in AI has exploded, pushing data centers to upgrade. Meanwhile, regular business computing hasn't stopped. Enterprise workloads have actually grown post-pandemic, with more cloud infrastructure and remote work systems needing higher specs, as noted by Google Cloud.

On top of that, phones need more memory. Modern flagships ship with 12GB or 16GB of RAM standard. Gaming consoles needed memory refreshes. Even automotive computing now requires significant memory capacity. The pie got bigger across every segment simultaneously.

Memory manufacturers have been increasing production, but not fast enough. They're running existing fabs at maximum capacity. They're reallocating resources from commodity RAM production to higher-margin specialized memory products. But even at full throttle, they're losing ground to demand.

Lenovo and other manufacturers have been calling their suppliers obsessively, trying to secure allocations. But here's the thing about supply crunches: when suppliers have limited stock, they're not negotiating on price. They're setting prices, and buyers are competing for allocations. This inverts the normal negotiating dynamic. A large manufacturer like Lenovo might normally leverage their volume to negotiate better terms. Instead, they're desperately trying to secure any allocation at whatever price the supplier demands, as reported by Futurum Group.

The suppliers know this. They're raising prices because they can. Because every customer needs memory and there's nowhere else to go.

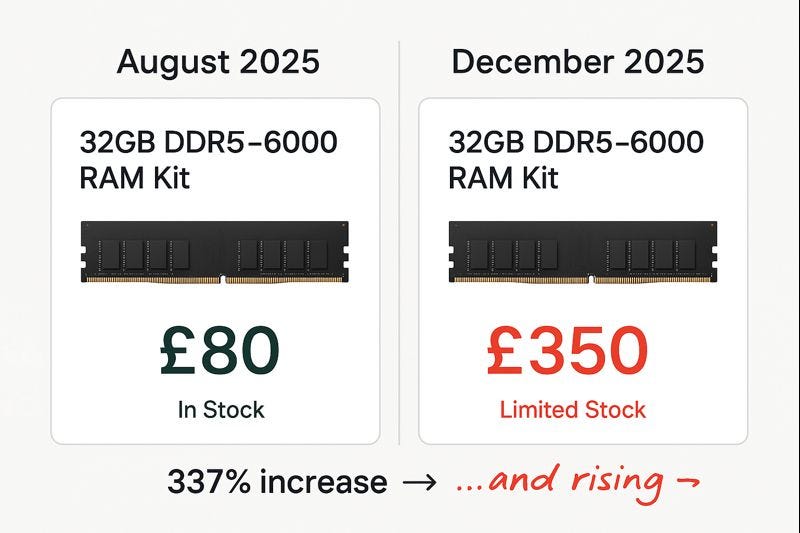

Laptop prices are expected to increase by March 2025, with gaming laptops seeing the highest rise at around 18%. Estimated data based on market forecasts.

How This Crisis Differs From Previous Shortage Cycles

Memory shortages happen periodically in computing. We saw significant ones in 2016-2017 and again in 2018. But this one has characteristics that make it more challenging to resolve.

First, the drivers are more diverse. Previous shortages were usually triggered by one or two factors: a production accident, geopolitical tension, or cyclical demand swings. This shortage has multiple structural causes that aren't going away anytime soon. AI demand is growing exponentially, not cyclically. Data centers are in permanent expansion mode. Consumer devices aren't reverting to lower memory requirements, as highlighted by Tom's Hardware.

Second, the manufacturing response is slow. Memory companies are investing in new capacity, but a fab that breaks ground in 2025 won't be producing chips at scale until 2027-2028. There's a 2-3 year lag between recognizing you need more capacity and actually producing from that capacity. Meanwhile, demand keeps growing.

Third, the price floor is higher than before. Even after previous shortages resolved, memory prices didn't always return to pre-shortage levels. Instead, they stabilized at elevated prices that reflected new production costs and investor expectations. This shortage might establish a new price baseline that persists even after supply normalizes.

Previous shortages also had clearer communication about timelines. Manufacturers would say: "We expect supply to improve by Q3" or "We're diversifying suppliers to get more allocation." This time? The narrative is: "We don't know when this ends." That uncertainty creates its own problems. Retailers can't price inventories confidently. Manufacturers can't plan margin structures. Consumers don't know if they should buy now or wait.

Lenovo's statement about March price hikes is notable because it's openly admitting the uncertainty. They're not saying supply will improve. They're not promising price decreases down the line. They're saying: "March will cost more, and we can't stop that." That's capitulation from a manufacturer perspective.

Estimated data shows potential price increases in early March with a peak, followed by a slight moderation in April. Prices may rise again by August for back-to-school demand.

The Domino Effect: Why This Impacts Every Laptop Buyer

You might be thinking: "Okay, RAM prices are higher. That's annoying, but how much more expensive can a laptop get?" The answer is: significantly more expensive, because RAM isn't the only cost driver being affected.

When memory suppliers raise prices, it cascades through the entire supply chain. Lenovo pays more for RAM. They pass that cost to retailers. Retailers pass it to consumers. But manufacturers don't just mark up the component cost directly. They usually add a percentage margin on top. So a

More importantly, RAM shortages often correlate with shortages in other components. The suppliers of memory chips, solid-state drives, and processors are often the same foundries and manufacturers using similar technology. When one type of chip is constrained, others often are too. So you might simultaneously be facing higher prices for RAM and storage.

Lenovo specifically manufactures across multiple tiers: consumer laptops, business machines, gaming rigs, and workstations. Different models use different memory configurations. A gaming laptop might use 16GB or 32GB standard. A business machine might use 8GB. A workstation might need 32GB or 64GB. When component costs rise universally, the impact on workstations and gaming machines is proportionally larger.

This creates a squeeze on consumer choice. The base models that were already affordable get more expensive, making the upgrade to the next tier less attractive price-wise. The premium models become genuinely unaffordable for many buyers. The sweet spot of value disappears.

Retailers will absorb some of this by reducing promotional offers and discounts. A laptop that might have normally been on sale gets reduced discounts in March. Your effective price floor for any given model rises.

Businesses that planned to refresh laptops see their budgets going further. Ten laptops that cost

Understanding RAM Specifications: What Changed in Recent Years

To really grasp why this crisis is hitting so hard, you need to understand how RAM requirements have evolved. Memory isn't a static component—what we consider "normal" keeps increasing.

Five years ago, a mainstream laptop came with 8GB of RAM. That was the standard sweet spot. Power users went to 16GB. Workstation and gaming enthusiasts maxed out at 32GB.

Today? The standard has shifted. New mainstream laptops ship with 16GB as base. Power users are moving to 32GB. Workstation users want 64GB or more. Gaming laptops are increasingly 32GB standard.

This shift is driven by real application requirements. Modern web browsers consume more memory. AI integrations in operating systems need more headroom. Video editing software demands higher specs. Development environments with containers, virtual machines, and multiple services running simultaneously eat RAM like nothing else.

When requirements increase, component demand increases proportionally. If the industry shifts from 8GB average to 16GB average across millions of laptops, that doubles memory demand. Memory manufacturers didn't plan for that demand doubling to happen on this timeline.

The other critical shift is in memory technology. Manufacturers are pushing LPDDR5 (low-power RAM) into laptops, especially ultraportables. LPDDR5 offers better performance and power efficiency than traditional DDR5, but it's harder to manufacture and more expensive. When manufacturers upgrade their entire lineup to newer memory standards for performance and battery life benefits, supply challenges intensify because they're not just dealing with more volume—they're dealing with more complex manufacturing.

Standards matter. A laptop that requires DDR5 at 5600MHz has different sourcing constraints than one requiring LPDDR5. Manufacturers can't easily switch between them. When one type is constrained, you can't just source the other. This rigidity makes the supply crunch worse.

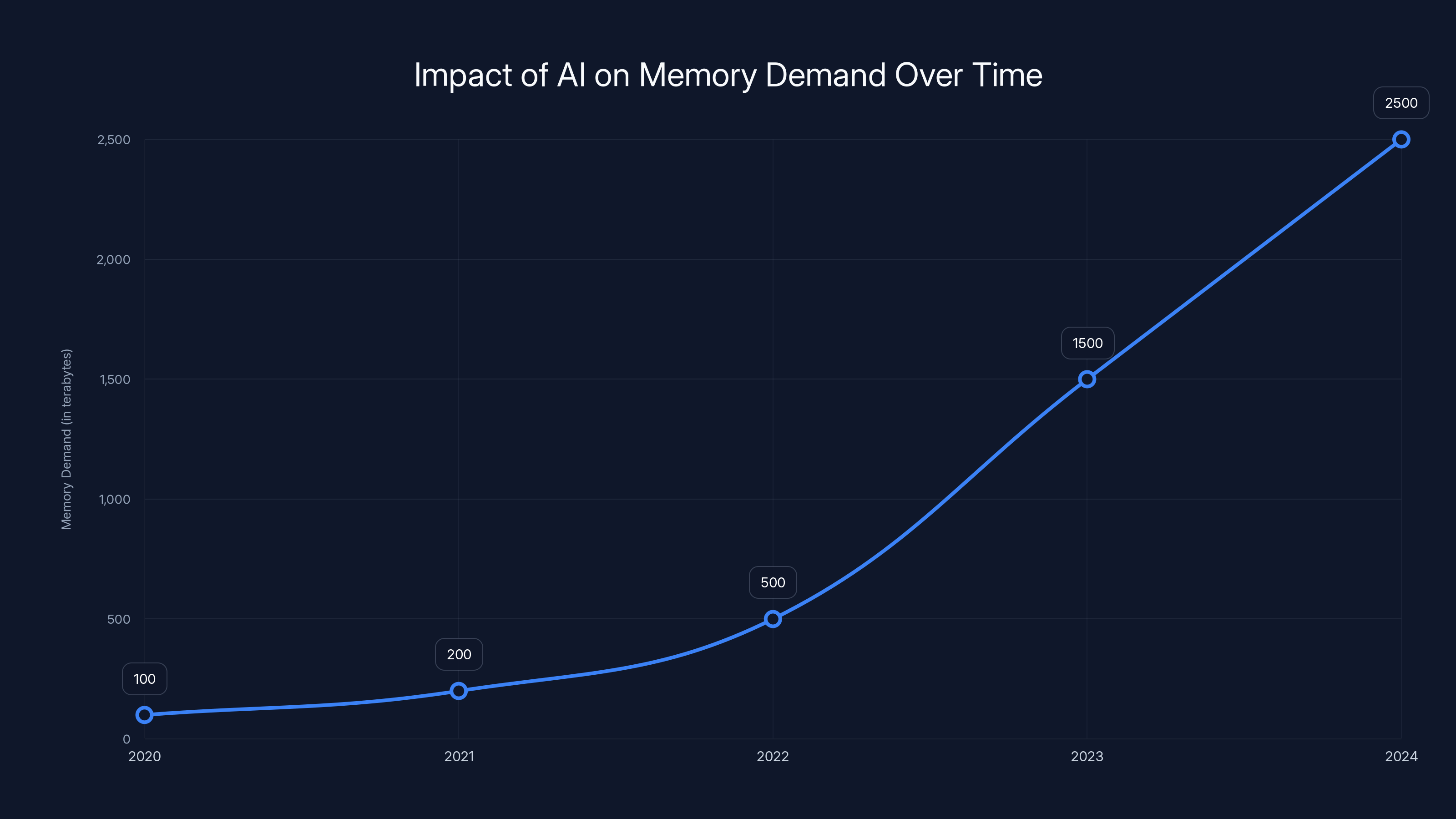

The demand for memory has skyrocketed since 2020, driven by AI infrastructure needs, with an estimated increase from 100 terabytes in 2020 to 2500 terabytes by 2024. Estimated data.

The Timing Element: Why March Specifically

Lenovo mentioned March specifically for price hikes. That's not random. Spring is when several market forces align in ways that make price increases stick.

First, spring is peak consumer laptop buying season. Students buy laptops for summer projects and incoming fall semesters. Businesses execute their annual refresh cycles. Retailers promote heavily. But in 2025, that demand bump is hitting a constrained supply market. Prices tend to rise when demand peaks and supply is fixed. This is basic economics.

Second, Q1 contracts between manufacturers and suppliers typically expire around this time. When renewal negotiations happen, suppliers have leverage. The contract renewals for Q2 2025 are happening right now, and suppliers are demanding higher prices. Manufacturers can't refuse because they need memory allocation. Contracts are priced accordingly.

Third, fiscal year timing matters. Many companies operate on calendar years for budgeting and reporting. March marks the transition into a new fiscal cycle. Companies budget for increased costs starting April/May. They're willing to accept cost increases that felt painful in February but necessary by March.

Fourth, storage and shipping costs interact with memory pricing. Component costs in February are locked into inventory that ships in March. There's a natural lag between when components are purchased and when products reach consumers. Lenovo's warning about March isn't just about their input costs in March—it's about products manufactured in February with February's component costs hitting retail in March.

The manufacturing industry also thinks in product cycles. A new generation of laptops is often timed to spring release windows. When new models launch, they incorporate new components at higher prices. Existing models get discounted to clear inventory. But if component costs are universally higher, even clearance pricing won't reach previous levels.

Manufacturer Strategies: How Companies Are Responding

Lenovo and other manufacturers aren't sitting passively accepting margin compression. They're executing strategies to mitigate the impact, but these strategies have limits.

One common approach is component tiering. Instead of offering one model with a given set of specs, manufacturers offer multiple variants. A "13-inch laptop" becomes available with 8GB, 16GB, or 32GB configurations. Users who don't need maximum specs pay less. This shifts demand toward lower-tier models where component costs are lower. But it requires inventory planning across multiple SKUs, which adds complexity when supply is tight.

Another strategy is supplier diversification. Lenovo is working with additional memory suppliers to reduce dependence on Samsung or SK Hynix. But here's the catch: secondary suppliers often have higher unit prices. Diversifying away from primary suppliers improves allocation security but increases per-unit costs. Manufacturers absorb this initially but eventually pass it to consumers.

Some manufacturers are negotiating longer-term contracts that lock in supply at agreed prices. This protects against further price spikes but usually means accepting higher prices upfront to secure supply certainty. Lenovo likely did this—they're paying more now to ensure they have allocation for coming months.

Manufacturers are also adjusting product roadmaps. Some lower-end models might be discontinued if they're not profitable at new component costs. Mid-range models get repositioned as the new entry point. This creates an upward shift in the product line where fewer affordable options exist. It's not eliminating the market—it's repositioning the market toward higher price points where higher memory costs are more absorbed.

Promotion strategy is shifting too. Instead of aggressive discounts, manufacturers are using bundling, extended warranties, or free software to add value without cutting prices. A laptop that would have been $100 cheaper in previous years might instead stay at full price but include premium software or extended support. This maintains margin while appearing to offer value.

Estimated data shows that RAM and component shortages can significantly increase laptop prices, with workstations and gaming models seeing the largest hikes.

The Consumer Impact: What This Means for Your Wallet

Let's get concrete about what this crisis means if you're shopping for a laptop.

Budget: You budgeted

Alternatively, if you insist on the same specs (16GB, 512GB), you're now paying $950-1050. The price jump is real, and it's substantial.

For gaming laptops, the impact is more dramatic. Gaming rigs often start with 32GB of RAM as standard. When memory prices double, that's a significant swing in total cost. A gaming laptop that was

For business users buying in bulk, the impact scales. A company refreshing 100 laptops instead of 10 feels the cumulative effect significantly. Budget that was allocated for systems might only cover 85-90 units at new prices. Either refresh cycles get extended, or companies accept lower specs.

For students and first-time buyers, the impact is particularly painful. If your budget is tight and you needed a laptop to start, watching prices increase forces harder choices. Do you delay purchase? Do you accept lower specs? Do you look at alternative brands or older models?

Refurbished and used market dynamics shift too. When new prices rise, used prices typically rise in sympathy. A refurbished laptop that cost

Freelancers and small businesses notice this acutely. A developer replacing their workstation or a designer upgrading their system faces a much higher cost at exactly the time when memory needs are rising due to larger file sizes and more demanding software.

Supply Chain Vulnerability: Why One Industry's Problem Is Everyone's Problem

You might wonder: can't memory manufacturers just increase production? Why doesn't capital investment solve this?

The answer involves manufacturing physics that most people don't appreciate. Memory chip fabs are among the most complex and expensive facilities humans build. A single chip-making facility can cost $15-20 billion. The machinery inside is specialized and often custom-designed. The cleanroom conditions are extraordinary—we're talking about making structures measured in nanometers, where a single dust particle ruins millions of chips.

When memory demand spikes, manufacturers start building new fabs. But the timeline is measured in years, not months. Construction takes 2-3 years. Equipment installation takes another year. Ramping production to maturity takes 2+ years more. So the decision to build a new fab made in 2023 won't contribute meaningful supply until 2027-2028.

Memory manufacturers face a classic chicken-and-egg problem. If they build capacity for peak demand and demand drops, they're stuck with expensive idle factories. If they build conservatively and demand surges, they lose market share to shortages. They always prefer the latter problem (shortage = high prices = high margins) to the former (excess capacity = low prices = thin margins).

This creates an interesting dynamic in the current crisis. Memory manufacturers are absolutely making record profits due to high prices. From an incentive standpoint, they're motivated to build more capacity. But that capacity takes years. Meanwhile, they're happy to produce at maximum efficiency from existing fabs and let prices stay elevated.

Regulatory dynamics also matter. Memory manufacturing requires expertise and investment that exists only in a few countries. There are geopolitical tensions around semiconductor supply chains. If manufacturers want to build fab capacity in new regions for diversification, they face regulatory hurdles, finding specialized workforce, and building infrastructure. This further constrains how quickly supply can increase.

The China dimension is also important. China has been investing heavily in memory production, but their facilities are often a generation behind the most advanced nodes. When global supply is constrained, advanced node production (what high-end laptops need) can't be replaced by Chinese capacity. This creates a two-tiered market where different regions face different constraints.

All these factors mean that when memory demand outpaces manufacturing capacity, the lag to resolution is measured in years, not quarters. Prices stay elevated long-term. Manufacturers eventually expand capacity, but supply and demand only rebalance after new fabs come online and market dynamics shift.

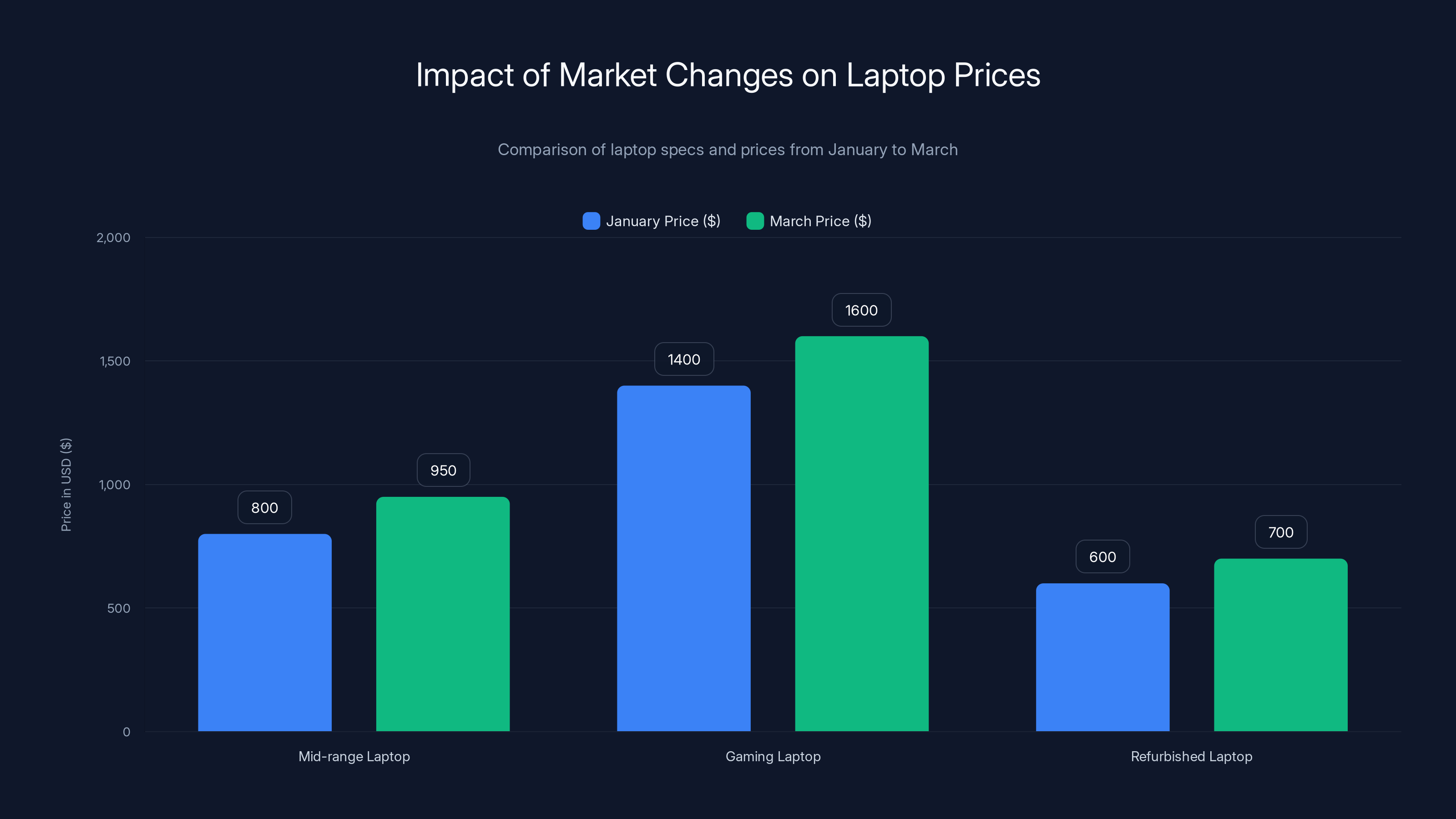

Estimated data shows a significant increase in laptop prices from January to March, with mid-range laptops rising by around

Historical Context: Learning From Previous Crises

Memory shortages aren't new. Understanding how previous ones played out helps us predict what comes next.

The 2016-2017 NAND flash shortage pushed SSD prices up 50-100% for extended periods. Manufacturers eventually diversified suppliers and new capacity came online, but it took 18-24 months for prices to normalize. Even then, they didn't return to pre-shortage levels. Instead, they settled at a "new normal" that was 20-30% higher.

The 2018-2019 memory cycle saw DRAM prices surge due to supply constraints and healthy demand. Prices peaked and then dropped sharply when demand cooled. This created the boom-bust cycle that manufacturers both fear and tacitly enable. They'd rather have volatile prices trending upward than stable low prices.

The 2021-2022 shortage pushed memory prices up again, though less dramatically because demand was uncertain (pandemic fears, economic uncertainty). Prices rose maybe 30-40% before stabilizing.

The pattern we see is consistent: shortages last 12-24 months, prices increase 30-100% depending on severity, then gradually normalize over several quarters. New price baselines are usually higher than pre-shortage levels.

Applying that historical pattern to the current crisis suggests we're looking at elevated prices throughout 2025 and potentially into 2026. The crisis probably doesn't fully resolve until new fab capacity comes online in 2027-2028. Even then, prices don't necessarily drop back to 2024 levels.

What's different this time is the structural demand shift. Previous shortages were usually driven by temporary factors that eventually resolved. This shortage has AI driving sustained high demand. AI data centers aren't building out temporarily—they're expanding continuously. Consumer AI features are sticking around. That creates a demand floor that doesn't evaporate, even if supply improves.

The AI Dimension: Why AI Changed Everything

If you trace back to what triggered this particular crisis, AI is the single biggest factor.

AI model training requires enormous amounts of memory. Training a large language model requires hundreds of gigabytes or terabytes of working memory. Data centers building out AI infrastructure aren't thinking about "Do we need enough memory?" They're thinking about "How much GPU memory and system RAM can we install?" More is always better.

When Chat GPT launched in November 2022 and exploded in popularity, every tech company suddenly realized AI was real and they needed infrastructure. Microsoft poured billions into cloud infrastructure for Open AI. Google accelerated data center builds. Amazon, Meta, and every major tech company started massive AI infrastructure projects.

All these data centers need memory. They need lots of it. And they need it fast. When the biggest tech companies on earth are all bidding for memory allocation simultaneously, prices have nowhere to go but up.

Consumer side, AI integration in operating systems and applications created new demand. Windows 11 with Copilot requires more RAM to function smoothly. Graphics software with AI upscaling features needs more memory. Game engines with AI-generated content features need more resources. None of this demand is going away.

Manufacturers also started pushing more memory in consumer devices as a feature. "AI-ready" became a marketing claim, which meant laptops with 16GB or 32GB standard became the new aspiration. This pulled demand up the stack.

Memory suppliers didn't anticipate how fast AI adoption would drive infrastructure expansion. They've been caught off-guard. When data centers started ordering 10X the memory they previously needed, suppliers were already sold out. The allocation that was supposed to cover consumer laptops and phones got diverted to data centers at premium prices.

From a supplier perspective, this is perfect. Data centers pay more per unit than laptop manufacturers. They're less price-sensitive because AI ROI is so compelling. A data center that pays 20% more for memory but gets their AI models trained and deployed faster is saving money overall. So suppliers rationally prioritize data center orders over consumer orders at normal prices.

This means consumer laptop memory demand is getting squeezed. Suppliers have allocation for data centers at high prices and can't fulfill all consumer demand. Laptop manufacturers either pay higher prices or accept lower allocations. Lenovo's March price warning reflects that they've chosen to pay higher prices to maintain allocation.

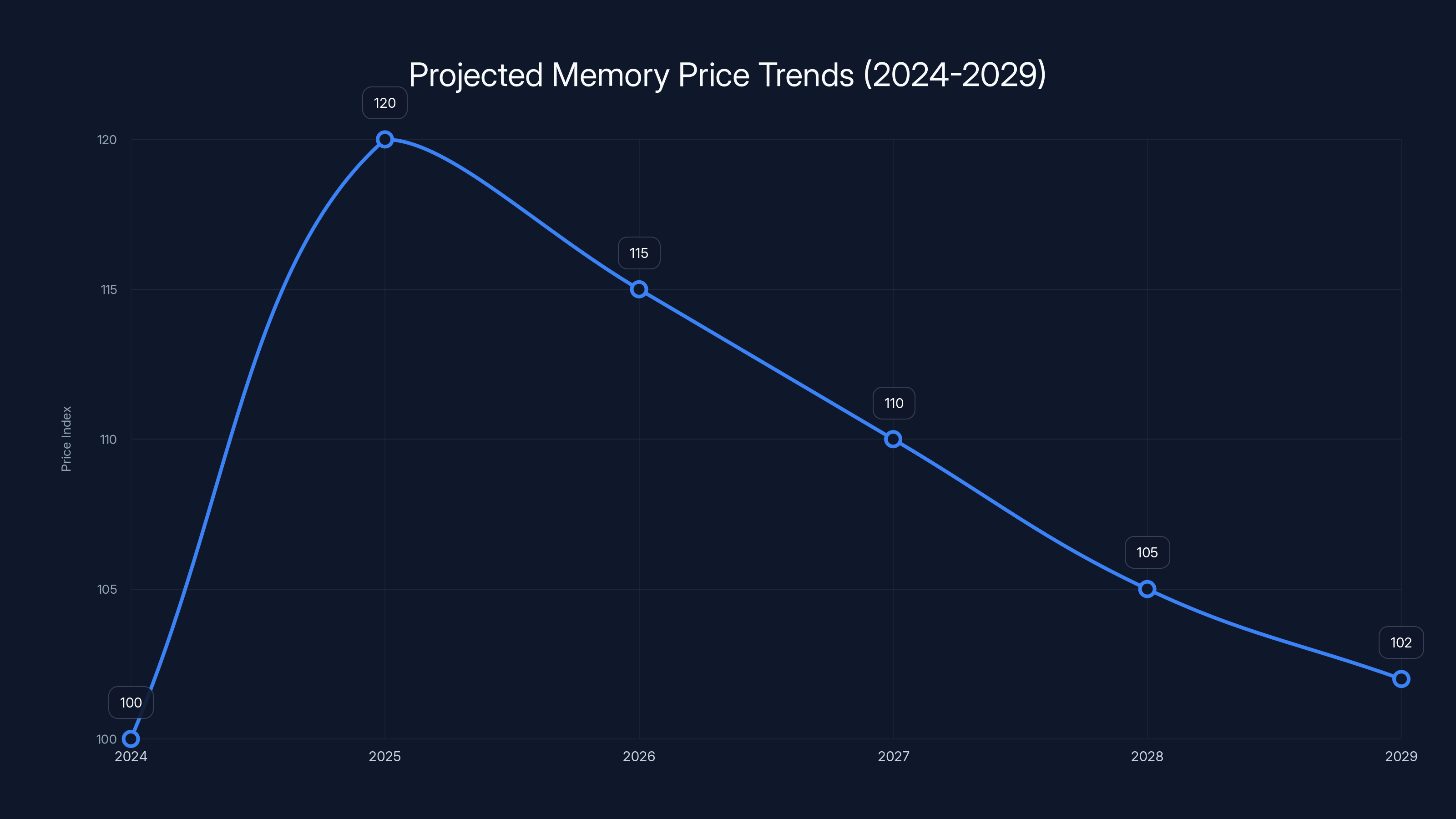

Memory prices are projected to remain elevated through 2025, with gradual moderation starting in 2026. Prices are expected to stabilize 15-25% above 2024 levels by 2029. Estimated data.

Regional Variations: Why Prices Differ Globally

One thing that gets overlooked in these discussions is that memory shortages don't affect all regions equally.

In the United States, where most major manufacturers are headquartered, they have leverage to secure allocations. They're big enough that memory suppliers listen. Prices will rise, but less dramatically than in smaller markets.

In Europe, there's slightly more complexity because there are strong local manufacturers with their own supply relationships. Lenovo has different supplier relationships in European markets than in North America. Pricing might differ accordingly.

In Asia, particularly in countries where memory manufacturers are headquartered (South Korea, Taiwan, Japan), there's more direct access to supply. Premium prices exist globally, but manufacturers in these regions might secure allocations faster.

In emerging markets, the impact is more severe. Smaller manufacturers and local companies don't have the negotiating power of Lenovo. They're paying higher proportional premiums. What costs

Lenovo specifically operates globally, so their supply planning has to account for regional differences. They might absorb some costs in North America and Europe where they have market power, but pass more through to prices in other regions where they're less dominant.

Currency fluctuations also matter. If you're a European manufacturer buying memory in US dollars, a weak euro makes memory more expensive. Regional pricing reflects not just memory costs but also currency dynamics and local competitive pressures.

The global dimension means this isn't just a US problem. Laptop buyers worldwide are facing price increases, but they're experiencing them at different magnitudes. Understanding your regional market dynamics helps predict how much worse things might get.

What This Means for Alternative Devices

Laptops aren't the only devices hit by memory shortages. Desktops, tablets, and specialty devices all use memory and face similar constraints.

Desktop PCs use DDR5 memory, and desktop RAM is experiencing similar price pressure as laptop memory. A 32GB DDR5 kit that cost

Tablets use different memory types, but supply is similarly constrained. iPad prices might increase, as might Android tablets. The component cost inflation affects everything.

Specialized devices—think gaming peripherals with RGB memory controllers, workstation-class systems, servers—all face memory cost increases. The breadth of the shortage means there's no refuge where prices are stable.

This creates an interesting option for price-sensitive buyers: some might switch to alternative form factors. Instead of a laptop, buy a tablet with a keyboard. Instead of a gaming laptop, build a gaming desktop (though that has its own cost challenges). These workarounds have limitations, but for some users, switching form factors provides escape from the price increase.

Cloud-based alternatives also become more attractive. Streaming your gaming experience from the cloud requires no local hardware upgrades. Remote development environments mean you don't need a powerful local machine. These alternatives have tradeoffs (latency, internet cost, privacy), but when local hardware gets expensive, cloud solutions look more viable.

Strategic Buying Guide: When to Buy and What to Buy

If you need a laptop, the current timing is genuinely important. Here's how to think about it strategically.

If you can buy before mid-February, do it. You're ahead of the price increases. You get February-level pricing and you have the device immediately.

If you can't buy before mid-February, your next window is probably late March or April. The initial price shock will have settled, and you'll have better sense of whether prices stick or moderate. Early March will likely be peak pricing as retailers adjust inventories and old stock clears.

What to buy depends on your actual needs. There's a strong temptation to future-proof and buy more memory than you need right now because memory is a fixed cost. If you're buying a laptop with soldered memory (not upgradeable), this makes sense. Buy as much as you reasonably use. If memory is upgradeable, you might buy minimum specs now and upgrade memory later if needed.

Brand considerations: Lenovo explicitly warned about price increases, which suggests they might be earlier in absorbing costs than competitors. Competitors might implement price increases later or more gradually. That said, the underlying supply situation is the same for everyone, so price increases will probably appear across all brands.

Timing for different purposes: If you're buying for seasonal needs (back to school in August), buying in March is reasonable—you're only a couple months from when you need it. If you're buying for immediate use, the question is whether you wait for potential price moderation or buy now to avoid further increases.

Refurbished markets might offer better deals. Refurbished laptops from 2024 might have better specs at lower prices than new 2025 models with reduced specs at similar prices. This isn't always true, but it's worth checking.

Airbnb discount codes, corporate purchase programs, and education discounts still work, but they're applied on top of new baseline prices. So a 10% education discount on a

Looking Ahead: When Does This Crisis End

This is the question everyone wants answered: when are prices going back down?

Realistic timeline: Memory prices probably stay elevated throughout 2025. There might be modest relief in late 2025 or early 2026 as new fab capacity comes partially online. Meaningful normalization probably doesn't happen until 2027-2028 when new facilities reach full production.

The probability of prices actually dropping back to 2024 levels is low. They'll probably stabilize 15-25% above 2024 prices once supply catches up with demand. That becomes the new baseline.

What could accelerate resolution? A major recession that crashes demand. If companies stop building AI data centers and consumer demand drops, supply would suddenly be adequate. Prices would plummet. But that requires an economic shock, and it's not something anyone wants.

What could extend this crisis? Further supply disruptions. A geopolitical event affecting Taiwan or South Korea would be catastrophic. New AI applications that drive demand higher than expected would push resolution further out. Manufacturers building fab capacity slower than expected would extend shortages.

The base case scenario is: prices moderate gradually throughout 2026-2027, new products normalize in 2027-2028, and we reach a new higher equilibrium pricing around 2028-2029. That's a 3-4 year crisis from peak pressure. It's not forever, but it's also not quick.

For consumers, the practical implication is: don't expect pricing relief soon. Any purchases in 2025 are happening at elevated prices. Budget accordingly and don't assume prices will drop to rescue you.

For manufacturers like Lenovo, they're betting that accepting margin pressure now is better than losing market share to higher prices. But there's a limit to how much margin compression they can absorb. If supply stays tight through 2026, price increases will happen whether manufacturers want them or not.

The Bigger Picture: Competitive Implications

This crisis has winners and losers beyond just manufacturers and consumers.

Manufacturers with strong supplier relationships and scale win. Lenovo, Dell, HP, and Apple have the leverage to secure allocation. Smaller manufacturers struggle. A company like Framework, which makes modular upgrade-friendly laptops, might face more severe allocation challenges than Dell.

Manufacturers already positioned in the premium segment win. They were already operating on higher margins. A 10-15% memory cost increase is manageable. Budget laptop makers operating on thin margins get crushed. Some brands might exit categories entirely.

Brands positioned as premium get cover to raise prices. If Lenovo's premium models go from

Cloud computing and SaaS providers benefit. When local hardware gets expensive, cloud solutions become more attractive. Companies like Amazon (AWS), Microsoft (Azure), and Google Cloud benefit from longer-term cloud adoption shifts triggered by hardware cost inflation.

Memory manufacturers win significantly. Their profit margins improve dramatically. They're motivated to hold supply constrained and prices elevated. There's no profit incentive to quickly expand production when current margins are so good.

Secondary markets (used, refurbished, rental) benefit. When new hardware gets expensive, these alternatives become more attractive. Businesses that would buy might instead lease or refresh less frequently.

The competitive landscape shifts because different companies absorb the crisis differently. Some brands might lose market share to competitors better positioned to manage costs. New entrants using alternative form factors (tablets, Chromebooks, hybrid devices) might capture customers priced out of traditional laptops.

Final Thoughts: What Buyers Should Actually Do

Lenovo's statement about March price hikes isn't a prediction. It's a warning that they've already absorbed as much cost as they can and further increases are inevitable.

If you need a laptop, the buying decision comes down to: do you need it now, or can you wait? If you need it now, buy it. If you can wait until late spring to see if prices stabilize, waiting might save you $100-150. If you can wait until summer or fall hoping for better deals, you're gambling that prices moderate. They might, but betting on it is risky.

For anyone buying in March specifically, you're hitting the worst timing. First-month prices are peak as retailers mark new inventory at new costs. Waiting a few weeks into April might see modest discounts as retailers compete for sales.

The broader implication: this is what supply chain fragility looks like. One component type gets constrained, and it cascades through the entire industry. Prices rise, quality decreases, availability shrinks. We built efficient global supply chains, and efficiency means very little buffer capacity. When buffers disappear, shocks are sharp and long-lasting.

For manufacturers, the lesson is: source diversification and supply security matter more than quarterly margin optimization. Lenovo's willingness to accept cost increases to secure allocation reflects that lesson learned.

For consumers, the lesson is simpler: when key components are in short supply, pricing power shifts to suppliers. There's no shopping around, no alternatives, no escape. You either buy at elevated prices or you don't buy. That fundamental dynamic won't change until supply catches up with demand, which—based on current timelines—is years away.

The RAM crisis is here. March price hikes are coming. Lenovo and every other manufacturer will raise prices. The sooner you make peace with that, the better.

FAQ

What exactly is the RAM crisis in 2025?

The RAM crisis refers to a severe shortage of DRAM and memory chips caused by demand far exceeding manufacturing capacity. AI infrastructure expansion, consumer device memory upgrades, and data center buildouts have pushed demand to record levels while manufacturers like Samsung and SK Hynix can't produce enough supply. This fundamental supply-demand imbalance is driving prices up across all computing devices.

Why can't memory manufacturers just produce more chips to solve the shortage?

Building new semiconductor manufacturing facilities (fabs) takes 4-5 years from groundbreaking to production and costs $15-20 billion each. Memory manufacturers are investing in new capacity, but the lag between deciding to build and actually producing chips at scale means relief won't arrive until 2027-2028. Additionally, specialized equipment and technical expertise needed to manufacture memory chips are difficult to source quickly, creating bottlenecks even with investment.

How much will laptop prices actually increase by March 2025?

Lenovo and other manufacturers are warning of price increases in the 8-15% range, with higher percentages for gaming and premium laptops where memory costs represent a larger portion of the bill of materials. Budget laptops might see 5-8% increases, while gaming rigs could increase 15-20%. The actual increases will vary by model, configuration, and brand, but expect widespread price increases across all tiers.

Should I buy a laptop now or wait for prices to drop?

If you need a laptop and have the budget, buying before mid-February makes sense to avoid March price increases. If you can wait, waiting until late March or April might reveal whether prices stabilize or see modest discounts as retailers manage inventory. Don't wait hoping for major price drops—based on supply forecasts, meaningful price relief won't arrive until 2027 or later. Buy based on your timeline and needs, not on speculation about future prices.

What are manufacturers doing to mitigate the crisis?

Manufacturers like Lenovo are diversifying suppliers to reduce reliance on any single source, negotiating longer-term contracts to secure allocation even at higher prices, adjusting product configurations to shift demand toward lower-memory models, and implementing strategic pricing to maintain margins. Some are discontinuing low-margin models entirely. These strategies help manufacturers manage the crisis but don't eliminate the underlying cost increases that get passed to consumers.

How does AI drive memory demand and make the shortage worse?

AI model training and inference require enormous amounts of memory, particularly in data centers. When every major tech company started building AI infrastructure simultaneously, memory demand from data centers exploded. Data centers are less price-sensitive than consumer markets and willing to pay premium prices for allocation, so they absorb memory supplies meant for consumer laptops. Additionally, AI integration in consumer operating systems and applications creates demand for more memory in everyday devices, further straining already-tight supplies.

Will memory prices ever return to 2024 levels?

Historically, memory prices don't return to pre-shortage levels. The 2016-2017 NAND shortage saw prices stabilize 20-30% higher than pre-shortage levels after normalizing. The current crisis is likely to follow the same pattern, with prices settling at a new higher baseline around 2028-2029. Budget for 15-25% permanent price increases above 2024 levels as the new normal rather than expecting full recovery.

Are there alternative devices I should consider instead of laptops during the shortage?

Tablets, Chromebooks, and cloud-based computing are alternatives worth considering if budget is tight. Tablets with keyboard accessories work for light productivity. Chromebooks have minimal memory requirements and cost less. Cloud-based development and computing options eliminate local hardware costs but require reliable internet and have latency considerations. These alternatives have tradeoffs, but for price-sensitive buyers, they might be viable workarounds during the memory shortage.

How does this crisis affect gaming laptops specifically?

Gaming laptops typically use 32GB of RAM as standard (compared to 16GB for mainstream machines), so they're disproportionately affected by memory price increases. A gaming laptop's memory cost increase of

What regions are most affected by RAM price increases?

All regions face price increases, but the magnitude varies. Markets where major manufacturers are headquartered (North America, parts of Europe) see smaller increases due to manufacturer leverage. Emerging markets see more severe increases because local retailers have less negotiating power with suppliers. Global manufacturers like Lenovo experience the full impact but can shift costs across regions strategically, meaning some markets absorb more price pressure than others.

When should we realistically expect memory prices to stabilize?

Realistic expectations point to elevated prices throughout 2025, modest relief in late 2025 or early 2026 as new fab capacity comes partially online, and meaningful normalization by 2027-2028. Full supply-demand rebalancing probably doesn't occur until 2028-2029. Until then, memory remains scarce and expensive. Consumer expectations should shift from "prices will drop" to "prices will stay elevated for 3-4 more years."

Key Takeaways

- Lenovo officially warned of unavoidable RAM price increases in March 2025, signaling the company has exhausted mitigation options

- Global DRAM shortage is structural, not temporary: driven by sustained AI infrastructure demand, limited manufacturing capacity, and 4-5 year fab construction timelines

- Expected price increases range from 8-15% for mainstream laptops and up to 20% for gaming rigs, with budget models facing spec downgrades instead of price cuts

- Memory shortage won't fully resolve until 2027-2028 when new manufacturing facilities reach production capacity; elevated prices likely become permanent baseline

- AI data centers consume memory allocations at premium prices, diverting supply from consumer laptop manufacturers and forcing them to choose between margin compression or cost pass-through

Related Articles

- Steam Deck OLED Out of Stock: The RAM Crisis Explained [2025]

- RAM Shortage Crisis 2026: How Memory Scarcity Could Bankrupt Companies [2025]

- Steam Deck Out of Stock: RAM Shortage Impact [2025]

- Instagram on Trial: Meta's Addiction Battle and Tech's RAM Crisis [2025]

- RAM Shortage 2026: Why Your Devices Will Cost More [2025]

- Mac Mini Shortages Explained: Why AI Demand is Reshaping Apple's Supply [2025]