![The Space Launch Industry in 2025: How Companies Are Competing With SpaceX [2025]](https://tryrunable.com/blog/the-space-launch-industry-in-2025-how-companies-are-competin/image-1-1770986322861.jpg)

The Space Launch Industry Faces a Historic Inflection Point

The commercial space industry is at a crossroads. For decades, launch was a niche market dominated by government contractors and a handful of established players. But in the last five years, everything changed. One company reshaped the entire economic model of spaceflight, forcing competitors to rethink strategy from the ground up.

That company is SpaceX. And it's not even close.

As of 2025, SpaceX accounts for approximately 50% of all orbital launches globally. Let that sink in. One company. Half the world's space launches. That statistic alone tells you everything you need to know about the competitive pressure facing the rest of the industry.

But here's what makes this moment interesting: SpaceX's dominance has paradoxically created the conditions for a wave of new competitors. Demand for launch services has exploded. Satellite operators need rides to orbit. Government agencies want redundancy and options. Companies are finally getting serious about building orbital infrastructure. The total addressable market for launch is bigger than it's ever been.

The problem? Everyone else is chasing a company that's already lapped the field.

This report examines the state of the global launch industry in early 2025. We'll look at the emerging players, the technical innovations driving competitiveness, the brutal economics of launch, and the hard questions every competitor must answer. Some will survive this period. Many won't. Understanding who has a realistic shot at challenging SpaceX's dominance requires looking past the marketing and into the actual engineering, funding, and strategic positioning.

Let's start with the uncomfortable truth: competing with SpaceX on price alone is a losing strategy. But that doesn't mean competition is futile. It means the path forward requires innovation, focus, and ruthless economics.

TL; DR

- SpaceX Controls 50% of Orbital Launches: One company dominates the market globally, creating unprecedented pricing pressure on competitors.

- Price Alone Won't Work: Rocket Lab and other players argue you can't win by undercutting SpaceX—you need differentiation.

- China Is Catching Up Fast: Successful ocean landings of booster hardware show rapid advancement in reusable rocket technology.

- Small Launch Players Are Consolidating: Orbex's collapse into insolvency shows the market can't sustain every startup.

- Reusability Is Table Stakes: Every serious competitor now requires a reusable booster architecture to compete long-term.

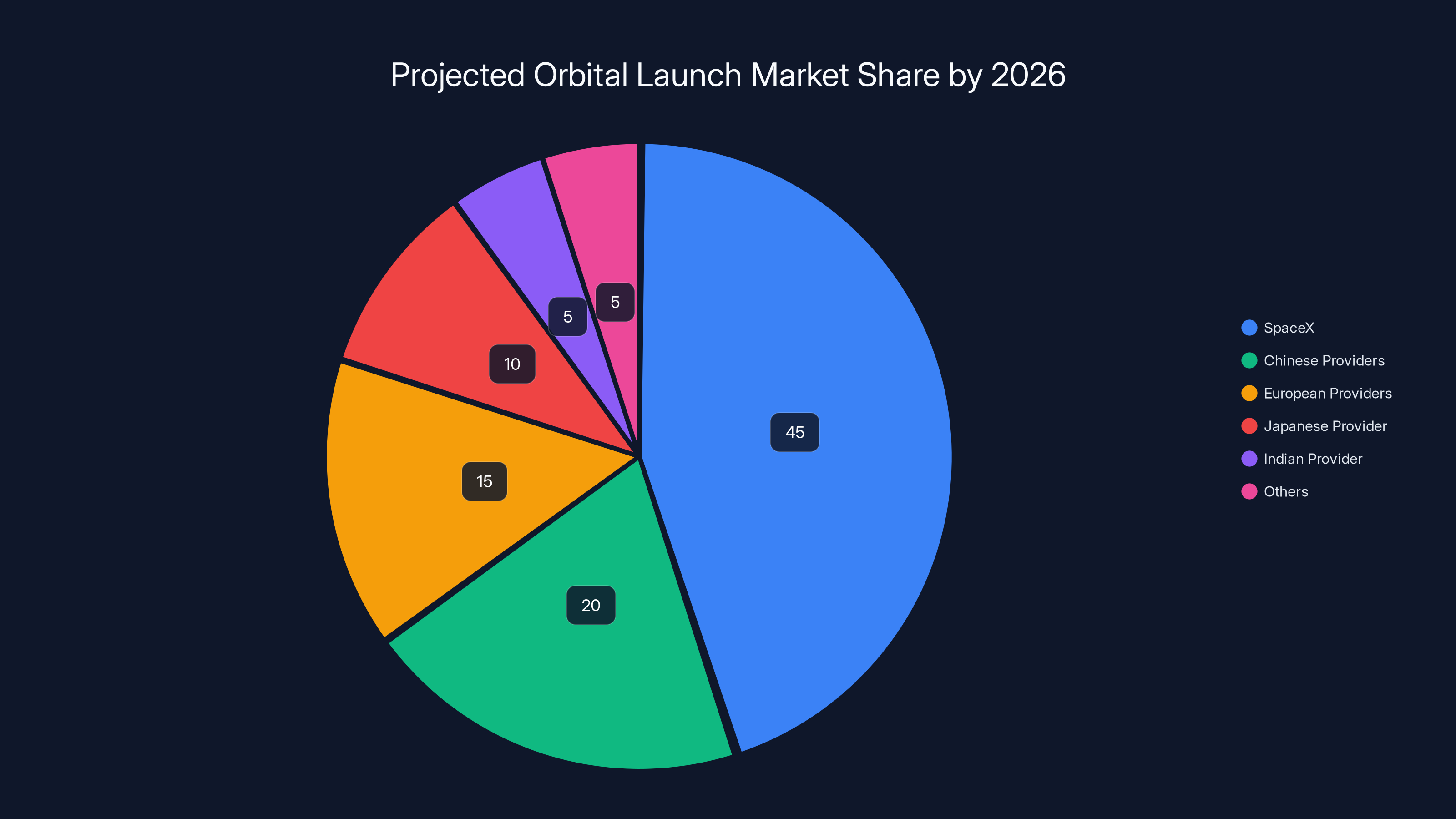

Estimated data shows SpaceX maintaining a dominant market share of 45% by 2026, with Chinese and European providers capturing significant portions of the market.

Why SpaceX Dominates: The Economics of Scale

To understand why SpaceX's position is so unassailable, you need to understand the fundamental economics of rocket launches.

A single orbital rocket launch—whether from SpaceX, Rocket Lab, or any other provider—requires moving roughly 50,000 to 140,000 pounds of payload to a specific altitude and velocity. The rocket must overcome Earth's gravity, atmospheric drag, and deliver the cargo with precision. This has always been expensive because rockets have historically been expendable. Build, launch once, throw away.

SpaceX changed that math by making rockets reusable. The Falcon 9 booster is designed to return to Earth, land itself, and fly again. This single innovation cuts the marginal cost of a launch dramatically. Instead of paying the full development and manufacturing cost in each flight, that cost is amortized across dozens or hundreds of launches.

The math is compelling. SpaceX's launch prices have dropped from roughly

This creates a vicious cycle for competitors. You need volume to amortize development costs. You need low prices to attract volume. But low prices require existing reusable infrastructure. You can't bootstrap your way into that position if SpaceX already dominates the market and can undercut any price you set.

Some executives in the industry acknowledge this brutal reality. Others are in denial.

SpaceX holds a dominant 50% share of the global orbital launch market in 2025, with Rocket Lab and European providers each capturing about 15%. Estimated data.

The Competitive Divide: Price Versus Differentiation

During industry discussions in early 2025, launch company executives revealed a fundamental split in strategy. The question: how do you compete with SpaceX?

One camp says you don't compete on price. Rocket Lab's leadership argues that trying to undercut SpaceX is economically suicidal. If SpaceX can launch at $1,500 per kilogram and still make money, then a startup trying to match that price while building infrastructure is heading toward bankruptcy. Brian Rogers, Rocket Lab's vice president of global launch services, put it bluntly: "If your idea is to go into the market competing with SpaceX on price, you're probably not in a good competitive position."

Instead, Rocket Lab's strategy is differentiation. They focus on the small-lift market—payloads too small or time-sensitive to wait for a SpaceX rideshare. They emphasize flexibility, fast turnaround, and the ability to hit specific orbital inclinations on demand. Their Electron rocket launches roughly once per week, not once per month or quarter. For customers with tight timelines, that matters more than absolute cost per kilogram.

But not everyone agrees. Devon Papandrew from Stoke Space articulated the opposing view at the same industry conference: "You absolutely have to have a plan to compete with SpaceX on price." The argument here is that you can't ignore the price leader in your market. Yes, SpaceX dominates now, but if you build a genuinely cheaper alternative—whether through novel engineering, different manufacturing approaches, or focusing on a specific launch profile—you create an opening.

Both strategies have merit. And both assume you can survive long enough to execute them.

The honest answer is probably somewhere in the middle. You need a defensible market segment—whether that's small payloads, high cadence, specific orbital inclinations, or targeted customer segments. And you need a credible path to reasonable margins within that segment. That might eventually mean competing on price, but not until you've established volume and operational maturity.

Orbex's Collapse: The Cost of Running Out of Money

Orbex was supposed to be a contender. Founded in 2016, the Scottish company attracted backing from European venture capitalists and government support from the UK space agency. The company's strategy was clean: build a small-lift orbital rocket for the European market, avoid the SpaceX price war by offering European-operated launch capacity and regulatory certainty.

In February 2025, Orbex filed for insolvency. The trigger was the collapse of a planned acquisition by The Exploration Company, another European space logistics startup. With that deal dead, Orbex couldn't secure additional funding.

Here's the brutal part: Orbex had been operating for nine years without producing a single flight-ready rocket. Nine years. For context, SpaceX built and launched the Falcon 1 in five years, from founding in 2002 to first launch in 2006. Rocket Lab reached orbit in nine years but was generating revenue before then through service contracts and investment from customers.

Orbex's problem wasn't the business model. It wasn't the location or the team. It was execution and runway. The company burned cash on development without reaching milestones that would generate revenue. This is a common pattern in aerospace: projects are expensive and slow. You need deep capital reserves or a path to revenue before your runway ends. Orbex had neither.

The company's assets and intellectual property may live on through Skyrora, another UK-based competitor. But Orbex itself is done. And it's unlikely to be the last casualty in the 2025 consolidation wave.

The lesson here isn't that the European market can't support a launcher. It's that development timelines in aerospace are longer than business plan assumptions. By the time a startup launcher reaches market, 8-10 years have often passed. During that time, the competitive landscape has changed, customer needs have evolved, and funding markets have shifted. You need either massive capital reserves or early revenue to survive that gap.

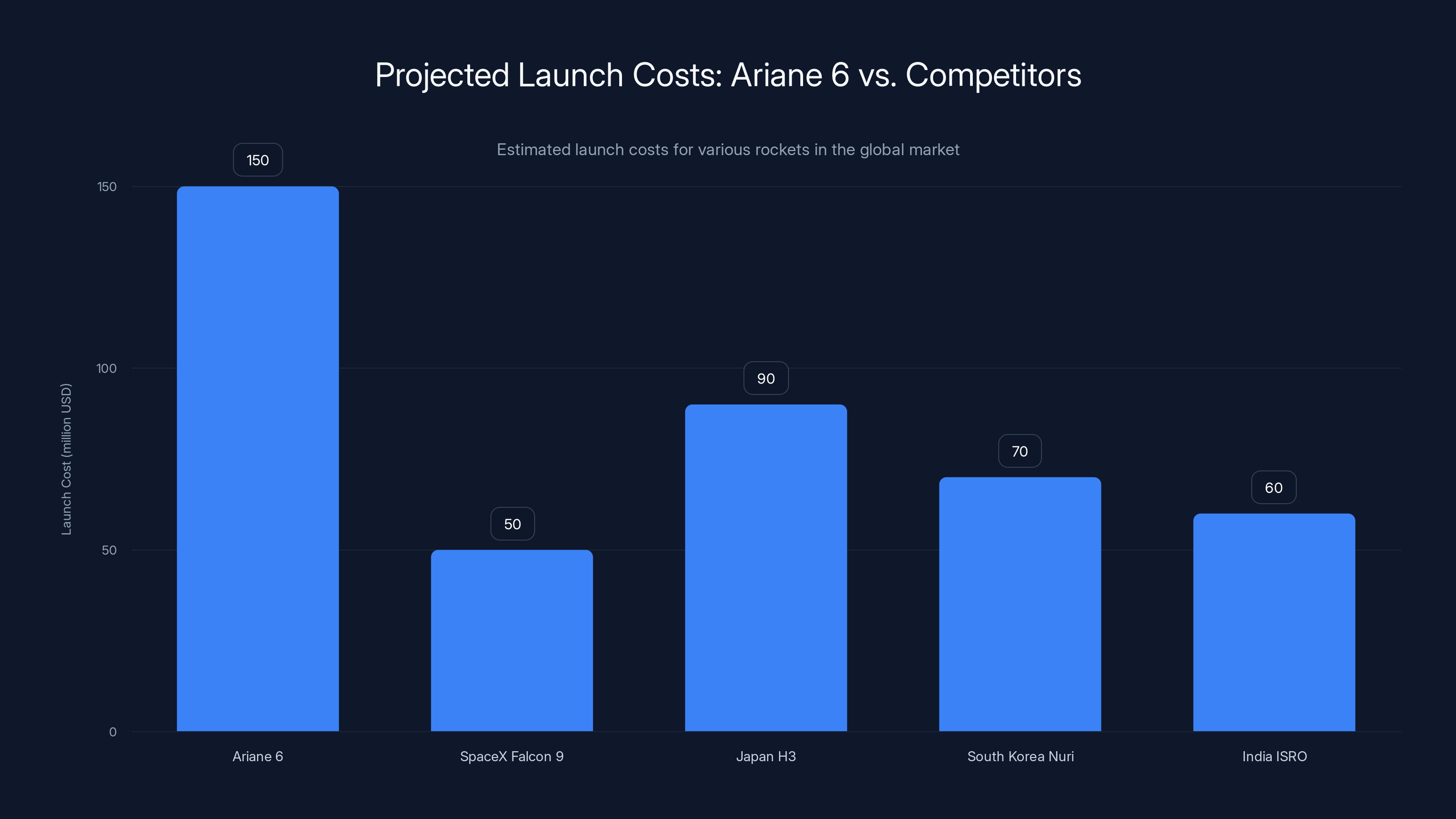

Estimated data shows Ariane 6's launch costs are significantly higher than its competitors, posing a challenge in a price-sensitive market.

Firefly's Block I Alpha: Racing Toward Operational Status

Contrast Orbex's trajectory with Firefly Aerospace's path. Firefly is pursuing medium-lift capability with its Alpha rocket. The company had setbacks—a catastrophic failure during a hot-fire test in Texas in 2024 destroyed the first stage. An earlier launch attempt in April 2025 ended in failure due to stage separation anomalies.

But Firefly is still flying. That's the key difference.

In February 2025, the company completed a successful 20-second static fire test of the Block I Alpha booster, clearing the way for a launch attempt no earlier than February 18 from Vandenberg Space Force Base in California. The mission, nicknamed "Stairway to Seven," is the final flight of the Block I Alpha variant. After this, the company will transition to Block II, which is designed to have stronger engines and higher performance.

Why does this matter? Because Firefly is learning in flight. Yes, they've failed. But they're gathering data, iterating, and moving forward. The company has successfully landed suborbital flights, demonstrating control and recovery. The recent static fire test validates engine and structural integrity. Each incremental step reduces technical risk.

More importantly, Firefly has access to capital and customer contracts. The company is backed by private investors and has government contracts that provide some revenue certainty. That cash flow allows them to continue development through failures that would bankrupt a company without outside support.

This is a crucial difference between sustainable space startups and those destined to collapse. You need either recurring revenue or very deep capital reserves. Preferably both.

Rocket Lab's Archimedes Engine Troubles: The Cost of Scaling

Rocket Lab is one of the few small-lift companies that has achieved scale and sustained revenue. The company launches the Electron rocket roughly once per week. Electron uses nine RP-1/LOX engines, each proven and reliable through hundreds of flights.

But Rocket Lab's future depends on a new rocket: Neutron. Neutron is much larger than Electron, designed to carry heavier payloads to orbit. The rocket will be powered by nine Archimedes engines, a new liquid methane/liquid oxygen powerplant with 165,000 pounds of thrust. Nine of these engines—765,000 pounds of thrust total—will boost Neutron to orbit.

Archimedes is a big deal because it represents a generational step forward in launch capability for Rocket Lab. But it's also a challenge. In the three months leading up to early 2025, Rocket Lab experienced two catastrophic test failures at its Mississippi test site. Both engines were blown up during testing—not gently shut down, but destroyed in anomalies.

This might sound bad. In the conventional aerospace world, it would be. But Rocket Lab's CEO Pete Beck provided important context: "We test to the limits, that's part of developing a successful rocket. We often put the engine into very off nominal states to find the limits and sometimes they let go, this is normal and how you ensure rockets don't fail in flight."

There's real wisdom here. Rocket Lab's philosophy is to break components during testing so they don't break in flight. Better to destroy an engine on a test stand than to have it fail during Neutron's first launch. The company has deliberately set out to find failure modes, understand them, and design around them.

However, if these failures continue or if Archimedes development slips beyond planned timelines, it could delay Neutron's operational debut. Rocket Lab has been targeting a first Neutron launch in late 2025. Delays would be costly and would give competitors breathing room.

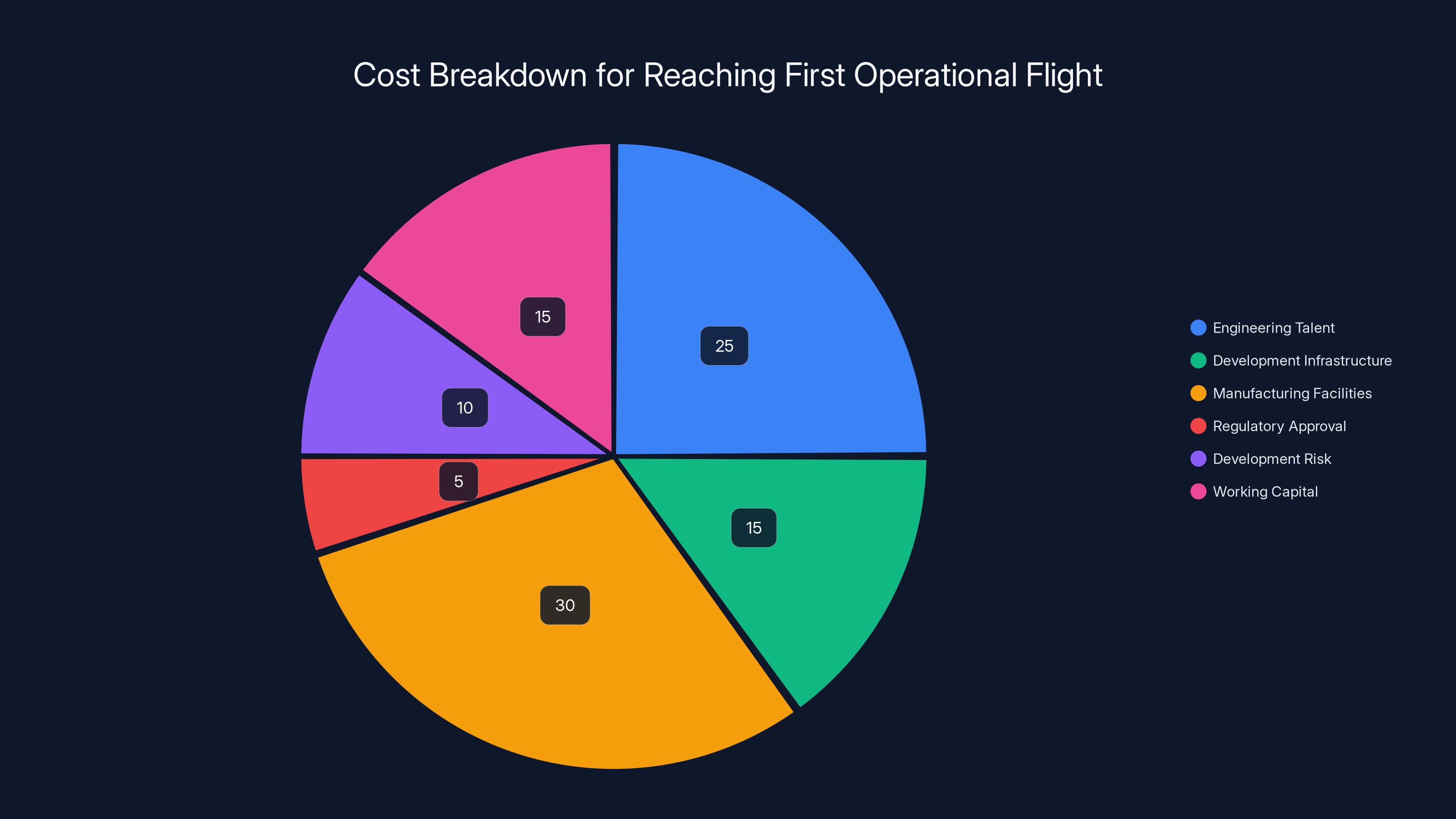

Engineering talent and manufacturing facilities are the largest cost components, making up over half of the total expenses for reaching the first operational flight. Estimated data.

Russia's Proton: A Dinosaur's Last Flight

In a small but symbolically significant event, Russia launched a Proton rocket in early 2025 after a nearly three-year hiatus. The Proton, first launched in 1965, is one of the oldest continuously developed rocket designs in the world. As of this flight, it had logged 430 launch attempts, with 48 total or partial failures—a reliability rate of roughly 89%.

That reliability rate was decent for its time. It's not acceptable in 2025.

The recent flight carried the Elektro-L No. 5 meteorological satellite from Baikonur Cosmodrome. The launch was delayed from late 2025 to February 2025 when engineers discovered a problem with the Block DM-03 upper stage during preflight checks. That issue was resolved, and the mission succeeded.

But this launch represents the end of an era. Russia has committed to phasing out the Proton by the end of the decade, replacing it with the Angara rocket family. Angara is modern, more reliable, and—crucially—more politically aligned with Russia's goal of space independence following Western sanctions.

The Proton's retirement is less about the rocket's technical capability and more about geopolitics and economics. A rocket designed in 1960 requires constant maintenance and upgrades. Spares are increasingly difficult to procure. The customer base has shrunk as Western companies no longer launch on Russian rockets and other nations develop domestic capabilities.

For the global launch industry, Proton's retirement reduces competition slightly. But that reduction is more than offset by the emergence of new Chinese launch providers and continued investments in European, Japanese, and American systems. The era of Russian launch dominance is over.

China's Reusable Rocket Progress: Closing the Gap

The most significant technical development in early 2025 came not from the West but from China. A subscale test vehicle for the Long March 10 rocket successfully launched and then executed what was described as a "picture-perfect ocean landing."

Let's unpack what that means.

China has been investing heavily in reusable launch technology. The Long March 10 is part of that effort—a next-generation heavy-lift rocket designed with reusability in mind. The subscale demonstrator is smaller than the full-size vehicle, used to validate the reentry and landing systems before committing to full-scale tests.

The ocean landing is particularly notable. Landing on water is actually harder in some ways than landing on solid ground. Water provides zero structural support—if your guidance is off by even a few feet, you miss the landing zone entirely. The booster must decelerate to near-vertical orientation, deploy landing legs, and touch down with minimal horizontal velocity. Do it right and you recover the booster with minimal damage. Do it wrong and you lose everything.

China's success on this test suggests their reentry guidance, propulsive landing, and recovery systems are maturing. That's a big deal because it means China is probably 2-3 years away from operational reusable Long March flights.

Why does this matter globally? Because a Chinese competitor capable of matching SpaceX's reusability economics would disrupt pricing assumptions everywhere. U.S. launch companies have been banking on the assumption that they have at least 5-7 years before serious reusable competition emerges. If China compresses that timeline, pricing pressure could become acute much sooner.

Moreover, China's state-backed advantage is significant. The country's space program doesn't operate under the same profit margin requirements as private Western companies. Chinese rockets can be priced to capture market share and strategic influence, not necessarily to maximize margins. That's a difficult competitive dynamic for Western companies to counter.

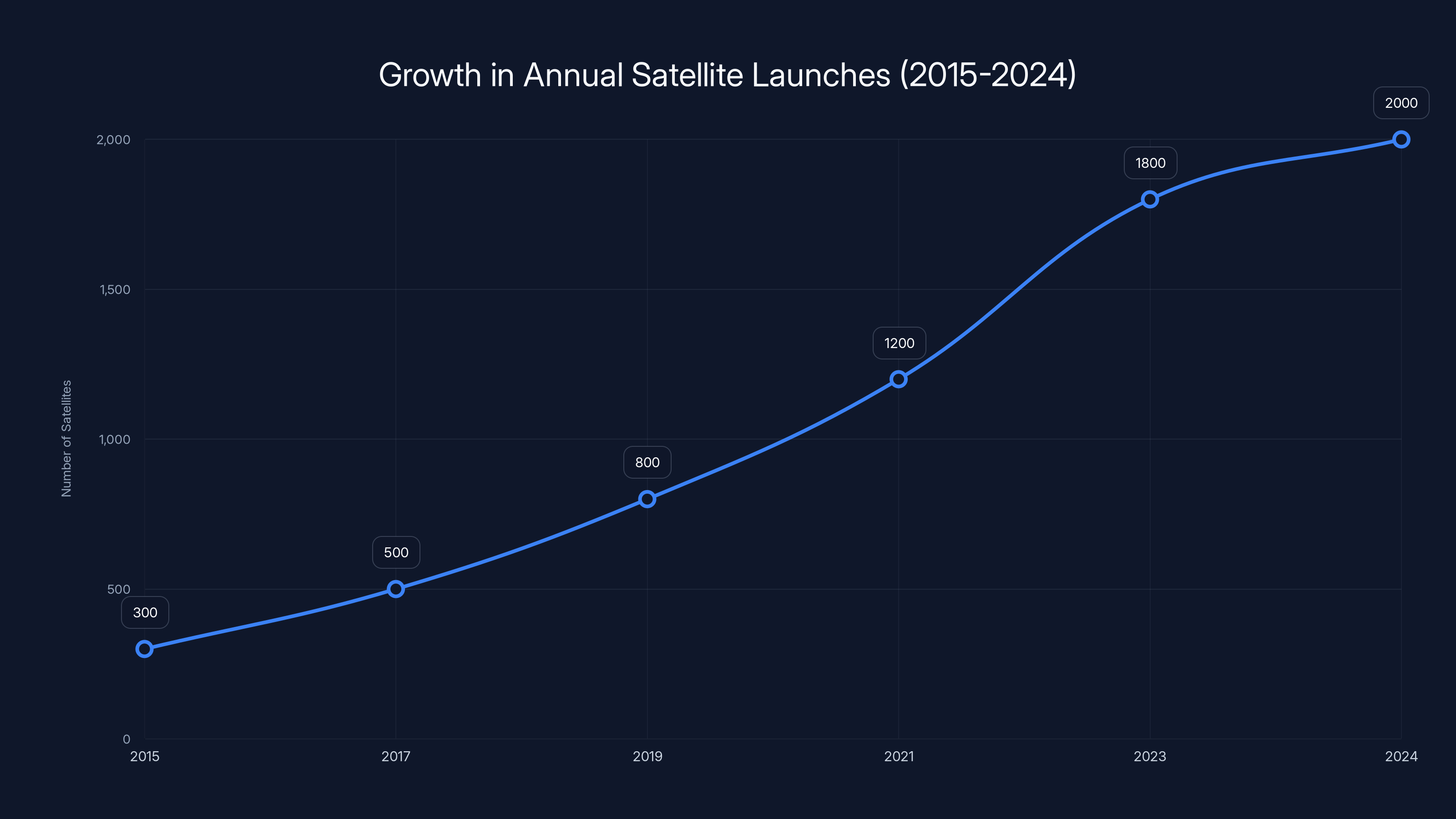

The number of satellites launched annually has increased from 300 in 2015 to over 2,000 in 2024, driven by mega-constellations and high demand. Estimated data.

The Labor Question: SpaceX's Regulatory Exemption

In a less publicized but potentially significant development, the National Labor Relations Board abandoned a complaint against SpaceX regarding labor practices. The labor board initially had jurisdiction under standard employment law, but ultimately determined that SpaceX should instead be regulated under the Railway Labor Act—the statute governing labor relations at railroad and airline companies.

This is a significant win for SpaceX and a setback for labor organizers. The Railway Labor Act's dispute resolution processes are slower and more cumbersome than standard NLRB procedures. For a company accused of unfair labor practices, that's advantageous.

Why does this matter to the broader launch industry? Because labor costs are a significant component of rocket manufacturing and operations. If SpaceX can maintain more flexible labor arrangements than competitors, that's a cost advantage. Other companies are subject to tighter NLRB scrutiny, union organizing campaigns, and standard employment dispute procedures. None of that applies to SpaceX under the Railway Labor Act framework.

It's a small regulatory advantage, but in an industry where margins are tight, small advantages compound.

The Economics of Entry: Why Most Startups Fail

Let's talk about the business model for a moment, because it explains why Orbex failed and why many other competitors will too.

Building a commercial orbital rocket requires:

-

Engineering Talent: Hundreds of highly skilled aerospace engineers, each costing

300K annually with benefits. A 100-person engineering team costs $20-30 million per year just in salaries. -

Development Infrastructure: Test facilities, launch sites, or agreements to use existing sites. Test stands for engines, propellant handling systems, and assembly facilities. Capital requirements: $50-200 million.

-

Manufacturing Facilities: The actual production line where rockets are built. Not a factory that makes 100 rockets per year, but something that can scale production from 5 per year to 50 per year. Capital requirements: $100-500 million depending on automation level.

-

Regulatory Approval: Licensing launches, ensuring compliance with export controls, meeting safety requirements. This isn't just a cost; it's a timeline. Plan for 2-5 years minimum to get your first launch license.

-

Development Risk: Your first launch will probably fail. Maybe your second too. Budget for 2-4 development flights before you achieve your stated performance. That's 2-4 launch attempts that don't generate revenue but do consume capital.

-

Working Capital: Once you can launch, you need capital to build rockets you'll deliver months later. That's months of payroll and material costs before you see revenue.

Total cost to reach first operational flight:

That's just to reach the point where you can reliably launch your baseline vehicle. Then you need capital for reusability, improvements, and scaling. Most venture capital companies can raise $200-500 million for a space startup. That's enough for early-stage development but insufficient for full development through first operational flight.

This is why space startups need either:

- Government backing (military or space agency contracts that fund development and guarantee customers)

- Anchor customers (national space agencies or large satellite operators who commit to a certain number of launches, providing revenue predictability)

- Massive private capital (not typical for VC firms, but possible with strategic investors)

- Sequential development (start with small vehicles, use revenue to fund larger vehicles)

Rocket Lab took the sequential approach. They started with Electron, a small-lift vehicle that could be built cheaply. The tiny satellites market had enormous demand and willingness to pay premium prices for fast turnaround. Electron's first successful launch was in 2017—just three years after the company pivoted to this strategy. Revenue from frequent Electron launches now funds Neutron development.

Orbex tried to go directly to a medium-lift vehicle without the established revenue stream. That's a much harder path.

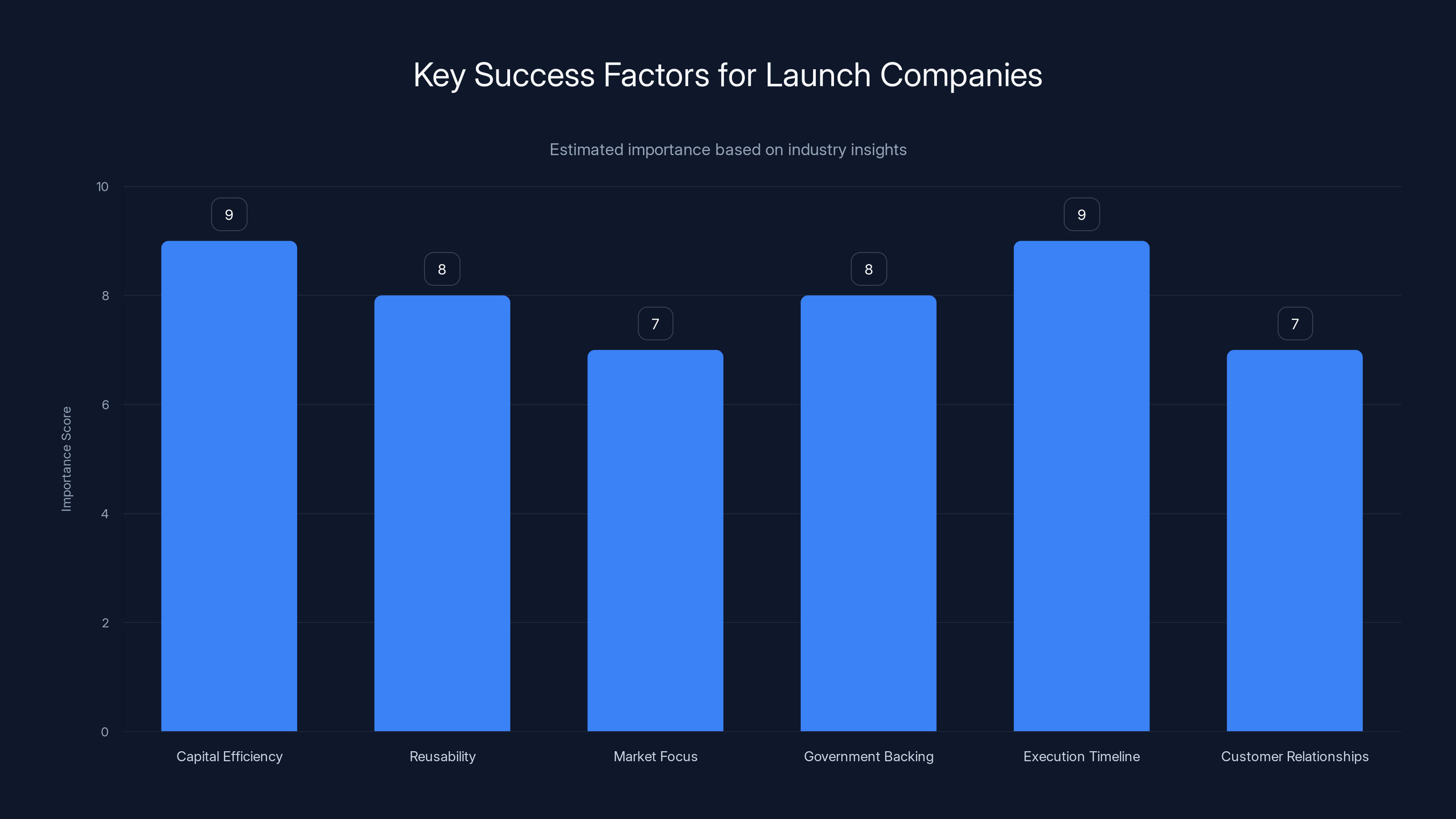

Capital efficiency and execution timeline are critical for launch company success, while customer relationships and market focus also play significant roles. Estimated data based on industry insights.

Customer Demand: The Untapped Satellite Constellation Market

The reason all these companies are fighting to build rockets is simple: customers desperately need launch capacity.

The satellite industry is in the middle of a transformation. Companies like SpaceX (Starlink), Amazon (Project Kuiper), and others are building mega-constellations—thousands of satellites in low Earth orbit providing broadband coverage globally. These constellations require constant replenishment. A typical Starlink satellite has a design life of 5-7 years. To maintain a constellation of 5,000 active satellites, you need to launch roughly 1,000 new satellites per year, every year, indefinitely.

Beyond Starlink, there are Earth observation constellations, communication satellites, Internet of Things networks, and government payloads. The total number of satellites launched per year has grown from roughly 300 in 2015 to over 2,000 in 2024. That number is still climbing.

Demand for launch is, by most estimates, supply-constrained. There aren't enough rockets to launch all the satellites that customers want to launch. SpaceX, despite flying half the world's orbital launches, still has a backlog. Rocket Lab is booked solid months in advance.

In normal markets, limited supply with strong demand means prices go up. Launch services have done exactly that. Commercial launch prices have increased 20-30% in 2024-2025 as demand has outstripped supply. This is unusual for a technology market where prices typically fall over time. But it confirms that launch supply is the limiting factor, not demand.

So here's the opportunity: every additional operational launch provider adds to total capacity and eventually brings prices down. That creates an opening for new entrants. But the bar to become "operational" is high. You need to fly dozens of times to prove reliability and begin competing on economics.

For perspective: Rocket Lab has achieved about 40 successful Electron launches. Firefly is still in the single digits. Relativity Space, Axiom Space, and other potential competitors haven't launched operationally yet. Meanwhile, SpaceX has hundreds of successful launches and reflight experience.

The International Dimension: Europe's Struggles and Asia's Momentum

Europe has long been a leader in space launch. The Ariane 5 rocket, developed by the European Space Agency, was for many years the world's most reliable heavy-lift vehicle. But Ariane 5 is being retired, and its successor, Ariane 6, is expensive and still in development.

Ariane 6 is designed to carry commercial and government payloads to orbit. It's a capable vehicle. But it's also expensive to develop (estimated costs exceed

This puts European launch companies in a difficult position. Government customers prefer national suppliers for political and strategic reasons, but those suppliers price at levels that private operators can undercut by 50-75%. That dynamic is forcing consolidation and rethinking.

Meanwhile, Asia is developing rapidly. Japan's H3 rocket is in development and scheduled for operational flights in 2025-2026. South Korea's Nuri rocket successfully reached orbit in 2022 and is planning commercial operations. India's ISRO is developing commercial launch capability alongside its government missions.

China, as discussed, is progressing rapidly toward operational reusable capability. That could be transformative if it succeeds.

The global launch industry is becoming multipolar. No single country dominates anymore. That competition is good for customers because it increases supply and drives innovation. But it's brutal for individual companies trying to compete.

How to Win: The Realistic Paths Forward

Given all of this, what's the realistic path to success for launch competitors?

It's not price competition alone. It's also not technological superiority in isolation. It's a combination of factors:

1. Market Segment Focus

You can't try to be everything. Rocket Lab focused on small-lift and fast cadence. That's a defensible position because SpaceX's Falcon 9 is overkill for small payloads and can't match Electron's launch frequency.

Other companies might focus on:

- High-inclination launches that SpaceX can't easily serve

- Dedicated rides to specific orbital altitudes

- National security launches (where security concerns justify premium pricing)

- Hypersonic technology demonstration and research payloads

2. Integration and Services

Launch is just the beginning. Real value is in the entire chain: mission integration, orbital mechanics, tracking, data retrieval. Companies that bundle these services can command premium pricing and create stickiness with customers.

3. Rapid Iteration

SpaceX succeeded partly because of culture. The company embraces failure as a learning mechanism. It tests hardware, iterates quickly, and moves forward. Companies that can match that tempo and still maintain safety standards will advance faster than traditional aerospace contractors.

4. Reusability and Affordability

You need a credible path to reusable boosters. Not immediately, maybe not in your first-generation vehicle. But in your roadmap, you must have reusability. That's the only way to reach SpaceX-competitive economics.

5. Customer Relationships

Large satellite operators will diversify suppliers for reliability. If you can become one of their top two or three launch providers, you've secured a revenue base that funds further development. That's how you escape the venture capital trap.

6. Geographic Advantage

If you're based in a country with strategic reasons to support national launch capability (like Europe or Japan), that's a moat. Government customers will pay a premium for a domestic supplier. Use that premium to develop competitive capability.

Technology Trends: What's Changing the Game

Beyond economics and strategy, several technologies are advancing rapidly and could reshape competition:

Additive Manufacturing

Rocket engines are traditionally fabricated from precision-machined aluminum or steel billets. That's expensive and wasteful. Companies like Relativity Space are experimenting with 3D-printed rockets using metal additive manufacturing. If they can achieve flight-proven hardware with dramatically lower manufacturing costs, that's a game-changer.

The advantage isn't just lower cost per unit. It's flexibility. A 3D printer can switch from producing one rocket design to another without retooling. That enables customization and small-batch production economics that traditional manufacturing can't match.

Methane Engines

Historically, rockets used either RP-1 (refined kerosene) or hydrogen. Rocket Lab's new Archimedes engine uses methane. Why? Methane is easier to manufacture, can be produced sustainably (from renewable sources), and simplifies supply chains. It's also denser than hydrogen, allowing for smaller fuel tanks. Companies worldwide are now developing methane engines. That convergence suggests methane will become a standard fuel, potentially commoditizing engine suppliers.

AI and Autonomy

Rocket landing sequences are complex. SpaceX's Falcon 9 booster uses closed-loop guidance, accelerometers, and thrusters to execute a precise landing. As sensors become cheaper and computing more capable, companies can implement more sophisticated guidance systems. Some advanced systems might eventually become fully autonomous, landing in weather conditions where human-piloted approaches would fail.

Launch Infrastructure

Historically, launch sites were huge complexes with massive launch towers and infrastructure. SpaceX is demonstrating that you can launch with smaller facilities. Relativity Space is designing launches from small concrete pads. If launch infrastructure costs drop from

Regulatory Hurdles: The Hidden Barrier

Here's what most people overlook: regulation is often a bigger barrier to entry than technology.

In the United States, you need launch licenses from the FAA. These aren't rubber-stamp approvals. They involve environmental assessments, coordination with the Department of Defense, export control review, and insurance requirements. A single license can take 2-5 years to obtain.

International coordination is worse. If your rocket will overfly other countries during launch or reentry, you need their permission. That's diplomatically complex and time-consuming.

Environmental compliance has become more stringent. Launch vehicles produce significant exhaust products that enter the atmosphere. Regulators increasingly care about sonic booms, water pollution from launch facilities, and atmospheric composition impacts. Companies have to plan and pay for environmental impact assessments.

Export controls are another barrier. Space technology is considered defense-sensitive in most countries. If your rocket has any government involvement or government funding, it can't be exported. This limits market access for some competitors and complicates international partnerships.

Rocket Lab navigated most of these issues years ago, which gives them a regulatory moat. New competitors have to repeat the process. The FAA is more experienced now and arguably more thorough. That's good for safety and bad for schedule.

Europe has less stringent export controls than the U.S., which could be an advantage for European launch companies. But European environmental regulations are stricter, which partially offset that advantage.

China operates under a completely different regulatory regime—essentially, government agencies coordinate internally without public transparency. That can accelerate timelines, but it also means less external visibility into technical readiness.

Supply Chain Vulnerabilities: A Lesson From 2022-2023

One factor that helped SpaceX during the pandemic was vertical integration. When supply chains broke down, SpaceX had in-house capability to produce many critical components. Competitors who outsourced more suffered longer delays.

That lesson is sinking in now. Companies are bringing more manufacturing in-house or establishing exclusive supplier relationships with guaranteed capacity. Rocket Lab manufactures most of its own hardware. Rocket Lab recently acquired one of its suppliers to ensure access to a critical component.

But vertical integration has trade-offs. It requires capital investment, specialized expertise, and ongoing operational complexity. Smaller companies that outsource benefit from supplier specialization and lower fixed costs. The optimal balance is probably company-specific and mission-dependent.

For competitive purposes, the reality is this: if your suppliers can't deliver, you can't launch. Building redundancy and backup suppliers is essential but expensive. Companies with deep capital reserves can afford to do this. Startups often can't.

The Path to 2026 and Beyond: Predictions and Scenarios

Looking ahead, several scenarios seem probable:

Scenario 1: SpaceX Maintains Dominance

In this scenario, SpaceX's cost advantage and operational maturity remain unassailable through 2026 and beyond. Other companies achieve operational status but operate in niche markets where SpaceX doesn't compete aggressively. Total orbital launch market grows, but SpaceX's market share stays above 40-50%. This is the most likely scenario based on current trends.

Scenario 2: Chinese Reusability Accelerates Disruption

China achieves operational reusable Long March flights in 2026-2027, offering pricing 20-30% below SpaceX but with lower reliability. This doesn't overthrow SpaceX but does force Western launch companies into deeper niches or consolidation. Some competitors may not survive.

Scenario 3: Regulatory Advantage Shifts

The U.S. government, concerned about launch market consolidation, accelerates licensing and support for alternative launch providers. European and Japanese rockets receive military contracts and government guaranteed purchase agreements. That undercuts pure price competition and allows non-SpaceX providers to compete on a more level playing field.

Scenario 4: Consolidation and Rollup

Small launch companies merge to achieve scale. By 2026-2027, the launch market might look like: SpaceX, Rocket Lab, two European providers, one Japanese provider, one Indian provider, and one or two Chinese providers. Everyone else is acquired or shut down.

Which scenario actually occurs will depend on technical execution, capital markets, geopolitical developments, and customer demand growth.

Lessons for Investors and Entrepreneurs

If you're considering investing in or founding a launch company, here's what the evidence suggests:

-

Scale matters but capital efficiency matters more. Rocket Lab has created more value with less capital than competitors with bigger budgets. That's because they focused ruthlessly on first operational flight and revenue generation.

-

Reusability is not optional. Any launch company without a clear path to reusable flight is probably not viable long-term. Single-use vehicles can't compete economically with reusable ones.

-

Market segment focus beats broad portfolio. Companies trying to serve both small and heavy-lift markets dilute resources. Pick a segment where you can achieve first-mover advantage or unique capability.

-

Government backing accelerates everything. Companies with military contracts, space agency partnerships, or government funding move faster. That's partly capital, partly regulatory, partly strategic alignment.

-

Execution timeline beats technology perfection. The company that reaches orbit first, even with a less perfect vehicle, beats the company trying to achieve 99% optimization in design. Flight testing teaches lessons that ground testing can't.

-

Customer relationships are your moat. Once a large satellite operator commits to your launch provider, switching costs are high. That customer base funds your next vehicle development.

FAQ

What is the current state of the global launch industry?

As of 2025, SpaceX dominates with roughly 50% of global orbital launches. Other players like Rocket Lab, Firefly, European providers, and emerging competitors are fighting for market share in a supply-constrained market where demand for launch capacity exceeds available supply. The industry is rapidly consolidating, with some players like Orbex failing while others like Rocket Lab scale successfully.

Why can't other companies simply match SpaceX's pricing?

SpaceX's low prices are enabled by reusable booster technology and accumulated operational experience across hundreds of flights. Competitors attempting to match those prices while still building their reusable infrastructure would operate at a loss. Most launch executives acknowledge you need differentiation beyond price—whether that's market segment focus, launch cadence, or specific customer service capabilities—to compete sustainably.

How quickly is China advancing in reusable rocket technology?

China has demonstrated successful ocean booster landings and continues to improve reusability techniques with each test. Based on current progress, Chinese reusable Long March rockets could be operationally available as early as 2026-2027, potentially offering prices 20-30% below SpaceX but with lower reliability initially. This timeline is significantly faster than Western estimates from 2022-2023.

What happened to Orbex and what does it tell us about the industry?

Orbex, a Scottish launch startup, filed for insolvency in February 2025 after nine years of development without producing a flight-ready vehicle. The company burned through capital on development without reaching revenue-generating milestones. The lesson: launch companies need either very deep capital reserves, government backing, or early revenue-generating capability to survive the long development cycle. Pure venture capital is typically insufficient.

How do launch companies generate revenue before their first operational flight?

Successful launch companies like Rocket Lab achieve early revenue through suborbital test flights, research contracts with universities or companies, government contracts for technology development, and strategic investments. Firefly benefits from military contracts that provide revenue certainty during development. SpaceX leveraged government contracts and demonstrated reusability milestones to secure additional funding. Companies relying solely on venture capital without alternative revenue sources often run out of money before reaching operational status.

What role does geographic location play in launch company competitiveness?

Geographic location provides strategic advantages through government support and customer loyalty. European launch companies benefit from ESA backing and preference from European satellite operators for "European" launch capacity, allowing higher pricing than pure market competition would support. Japan, India, and South Korea have similar advantages. However, this geographic protection only works for government and regulated customers. Commercial customers are increasingly price-sensitive and geographically agnostic, favoring SpaceX and other low-cost providers.

Conclusion: The Industry at an Inflection Point

The global launch industry in 2025 is caught between competing forces. On one side, SpaceX has achieved an unprecedented dominance that seems unassailable. The company controls half of all launches, continues improving Falcon 9 and developing Starship, and maintains cost advantages that competitors struggle to match.

On the other side, demand for launch capacity remains supply-constrained. That creates genuine opportunities for competitors willing to focus ruthlessly on specific market segments and execute efficiently. Rocket Lab proves that you can build a sustainable, profitable launch business without directly competing against SpaceX on price or total tonnage.

Orbex's collapse shows that the bar is high. You need either exceptional capital reserves or a path to early revenue. You can't develop a rocket in the background for a decade and hope the market will still exist when you finish. The world changes too fast.

China's progress on reusable booster landings is the wild card. If China successfully transitions to operational reusable launches, the competitive dynamics shift dramatically. Pricing pressure increases. Some marginal players won't survive. But total market size also increases as lower prices drive new customer demand.

For entrepreneurs and investors, the message is clear: you need a defensible strategy. That might be a specific market segment, geographic advantage, specific customer relationships, or a technically differentiated vehicle. But you need something beyond "we're building a rocket that's kind of like SpaceX's."

For customers, the message is equally clear: supply constraints are easing. Don't accept that SpaceX pricing is permanent. Shop alternatives. Multiple providers are achieving operational status. Negotiate accordingly.

The space industry is becoming competitive in ways it hasn't been before. That's good for customers and the overall ecosystem. For individual companies trying to compete, it's brutally challenging. But for space technology overall, competition drives innovation, reduces costs, and expands what's possible from Earth orbit.

In the next few years, we'll see which companies execute well and which ones run out of time or capital. That outcome will shape the industry for decades.

Key Takeaways

- SpaceX's 50% global launch market share is built on reusable booster technology and operational maturity across 350+ successful flights

- Competing on price alone is economically unsustainable; successful competitors differentiate through market segment focus, operational cadence, or customer integration

- Orbex's insolvency after 9 years of development demonstrates the capital and timeline challenges facing launch startups without government backing or early revenue

- China's successful booster ocean landings suggest operational reusable Long March flights within 2-3 years, potentially disrupting Western launch market assumptions

- The launch industry requires either massive capital reserves (2B to first operational flight), government contracts, or established revenue streams to survive development cycles

Related Articles

- Rocket Lab's Archimedes Engine Explosions: Why Blowing Up Is Part of the Plan [2025]

- China's Moon Mission Breakthrough: New Lunar Spacecraft and Reusable Rocket [2026]

- SpaceX's Moon Base Strategy: Why Mars Takes a Backseat in 2025 [2025]

- SpaceX Starship Upper Stage Malfunction: Launch Recovery Timeline [2025]

- Why NASA Finally Allows Astronauts to Bring iPhones to Space [2025]

- Blue Origin Pauses Space Tourism to Focus on Moon Missions [2025]