![Waabi's $1B Funding & Uber Robotaxis: Complete Guide [2025]](https://tryrunable.com/blog/waabi-s-1b-funding-uber-robotaxis-complete-guide-2025/image-1-1769600430465.png)

Introduction: The Autonomous Vehicle Funding Landscape Shifts in 2025

The autonomous vehicle industry reached an inflection point when Waabi announced a historic

For context, the autonomous vehicle sector has matured significantly since the early days of self-driving hype. The industry landscape includes established players like Waymo (owned by Alphabet), Aurora Innovation (which acquired Uber's autonomous trucking division ATG in 2020), and Kodiak Robotics, along with emerging international competitors like Wayve, We Ride, and Momenta. Each company has pursued different technical architectures, business models, and go-to-market strategies. Waabi's approach stands apart because of its stated ability to tackle multiple verticals—autonomous trucking and robotaxis simultaneously—using a single, unified technological architecture.

What makes this announcement particularly noteworthy is the timing and the strategic partnership structure. Unlike previous funding rounds that often represented bets on a company's potential, the Uber commitment includes performance-based milestones, meaning Waabi must deliver tangible results to unlock the full $250 million. This structure reflects both Uber's confidence in the technology and a more mature, results-oriented approach to autonomous vehicle investments compared to the venture capital euphoria of the mid-2010s.

The announcement also carries symbolic weight because Waabi's founder and CEO Raquel Urtasun previously served as chief scientist of Uber's autonomous vehicle division before it was sold to Aurora Innovation in 2020. Her return to the Uber ecosystem with her own company demonstrates how industry consolidation and executive mobility have created a web of interconnected autonomous vehicle initiatives.

This comprehensive guide explores the technical foundations of Waabi's approach, the commercial implications of the Uber partnership, competitive dynamics with other autonomous vehicle companies, and what this funding milestone means for the broader autonomous vehicle industry. We'll examine the underlying technology, the business strategy, financial projections, regulatory considerations, and alternative approaches in the autonomous vehicle space.

Understanding Waabi's Core Technology: The AI-Powered Architecture

The Waabi World Simulator: Building Digital Twins at Scale

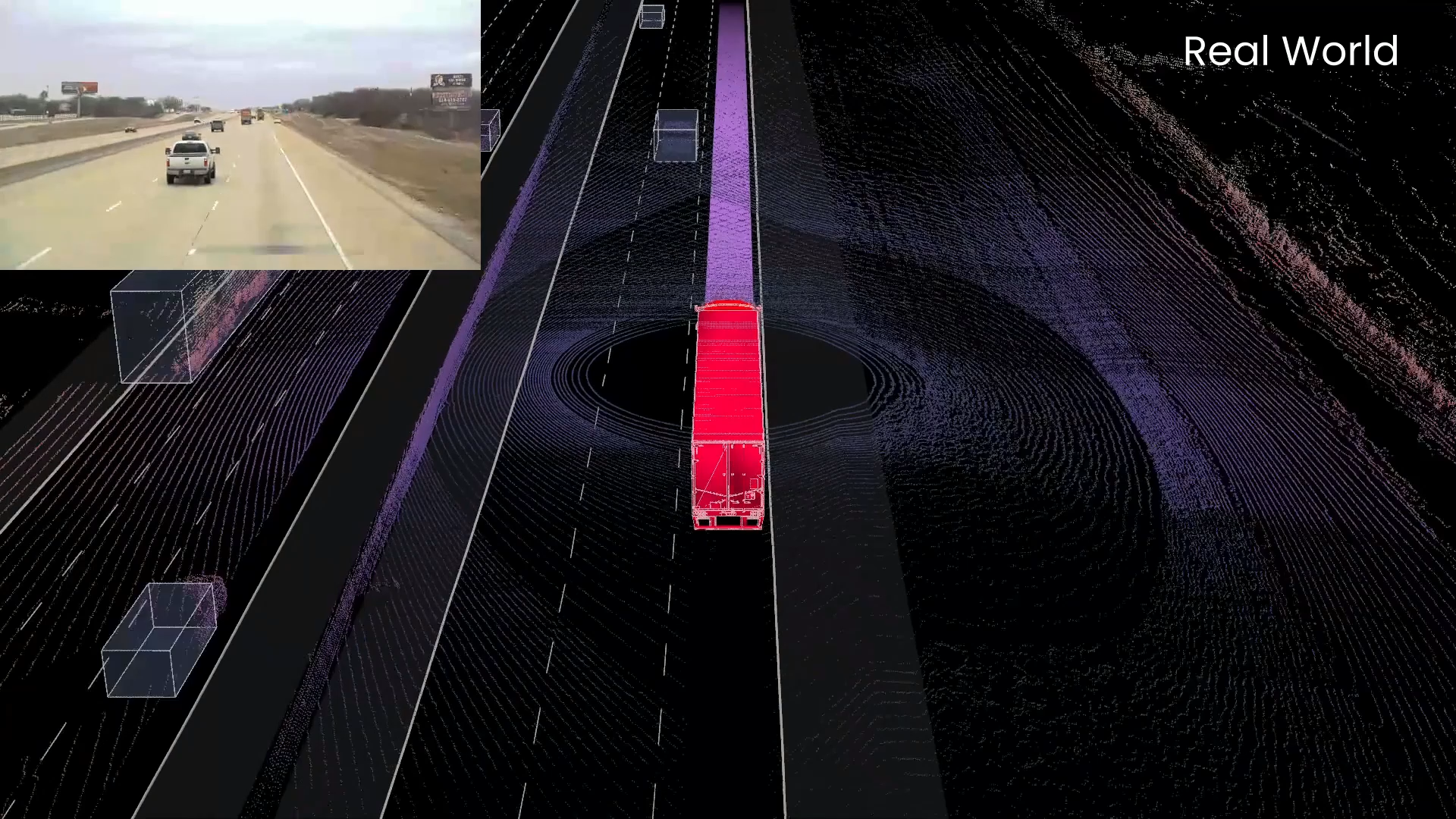

At the heart of Waabi's competitive advantage lies Waabi World, a closed-loop simulator that represents a fundamentally different approach to autonomous vehicle development compared to traditional methods. Rather than relying exclusively on real-world driving data collection (which has proven expensive and time-consuming for competitors), Waabi has built a synthetic environment that automatically constructs digital twins of the physical world from collected data.

The simulator operates on a principle that mirrors how human drivers learn: rather than requiring millions of miles of real-world driving to master various scenarios, the system manufactures and presents edge cases—unusual traffic situations, weather conditions, construction zones, and emergency scenarios—in a controlled environment. This approach substantially reduces the data collection burden. Competitors like Waymo have publicly reported testing millions of miles in the real world annually, with associated costs for vehicles, drivers, insurance, and infrastructure. Waabi's approach suggests a more capital-efficient pathway that could reduce the time-to-deployment significantly.

The closed-loop nature of Waabi World is crucial to understanding the competitive advantage. Traditional simulation in autonomous driving has struggled because it either oversimplifies real-world conditions or requires exhaustive manual scenario creation. Waabi's automated digital twin generation capability bridges this gap by using real-world data to inform synthetic scenario generation. The system performs real-time sensor simulation, meaning it can model how different sensor configurations (Li DAR, cameras, radar) would behave in various conditions, allowing Waabi to test different hardware combinations without physically building and testing each variant.

The self-teaching mechanism—enabling the Waabi Driver to "learn from its mistakes without human intervention"—suggests the company has implemented reinforcement learning techniques that automatically improve driver behavior based on simulation failures. This is conceptually different from supervised learning approaches where human experts must label correct behavior patterns. The efficiency gains from this methodology could represent orders of magnitude difference in development timelines and costs.

The Waabi Driver: Generalized AI Architecture Across Vehicle Types

Waabi's headline claim that their "Waabi Driver" can handle both autonomous trucking and robotaxis using the same underlying AI architecture challenges the traditional wisdom that each vehicle class requires purpose-built systems. This generalization capability, if validated, would represent a significant technical achievement because trucking and robotaxis face distinctly different operational requirements.

Autonomous trucks operate primarily on highways where road geometry is relatively predictable, but they must handle long-duration missions (10-20 hour driving days), interact with commercial logistics infrastructure, and manage heavy vehicle dynamics. Robotaxis operate in dense urban environments with complex intersection scenarios, pedestrian interactions, and frequent short trips in varied conditions.

Urtasun's claim that the underlying AI can "reason about its surroundings as a human would and choose the best maneuver" suggests the system employs sophisticated scene understanding and decision-making algorithms rather than simple rule-based approaches. This involves computer vision systems that can interpret scene elements (other vehicles, pedestrians, cyclists, traffic signals, lane markings), predict the likely behavior of other traffic participants, and select driving actions that maximize safety and efficiency.

The ability to generalize across vehicle form factors (trucks, cars, and potentially robotics as Urtasun hinted) implies the core reasoning engine operates at a level of abstraction above specific vehicle characteristics. Rather than tuning parameters for different turning radiuses or acceleration profiles, the system's decision-making applies to any vehicle that can be actuated. This architectural approach aligns with recent advances in transformer-based models and multi-modal learning in artificial intelligence, though Waabi hasn't publicly detailed their specific model architectures.

Learning from Fewer Examples: Data Efficiency as Competitive Advantage

Waabi's promise to "generalize and learn from fewer examples than traditional autonomous driving systems" directly addresses one of the most significant cost drivers in autonomous vehicle development. Waymo, for instance, has collected billions of miles of driving data and spent over a decade developing their autonomous driving technology. The associated costs—data collection infrastructure, annotation labor, computational resources for training, and deployment vehicles—have likely exceeded several billion dollars.

The efficiency claim rests on the quality of the synthetic data and simulation environment. If Waabi World can generate edge cases that more effectively train the decision-making system than equivalent real-world miles, the company could achieve comparable performance with substantially less data collection. This would translate to faster time-to-market and lower development costs, both critical advantages in a capital-intensive industry.

The mechanism underlying this efficiency likely involves two components: first, the simulator can generate data aligned with the learning algorithm's needs rather than presenting data in the natural distribution it occurs in the real world; second, the reinforcement learning approach allows the system to explore and learn from failure modes in simulation without risking safety in real-world testing. This represents an evolution of methodology from the early 2010s when autonomous vehicle companies primarily relied on carefully labeled real-world datasets.

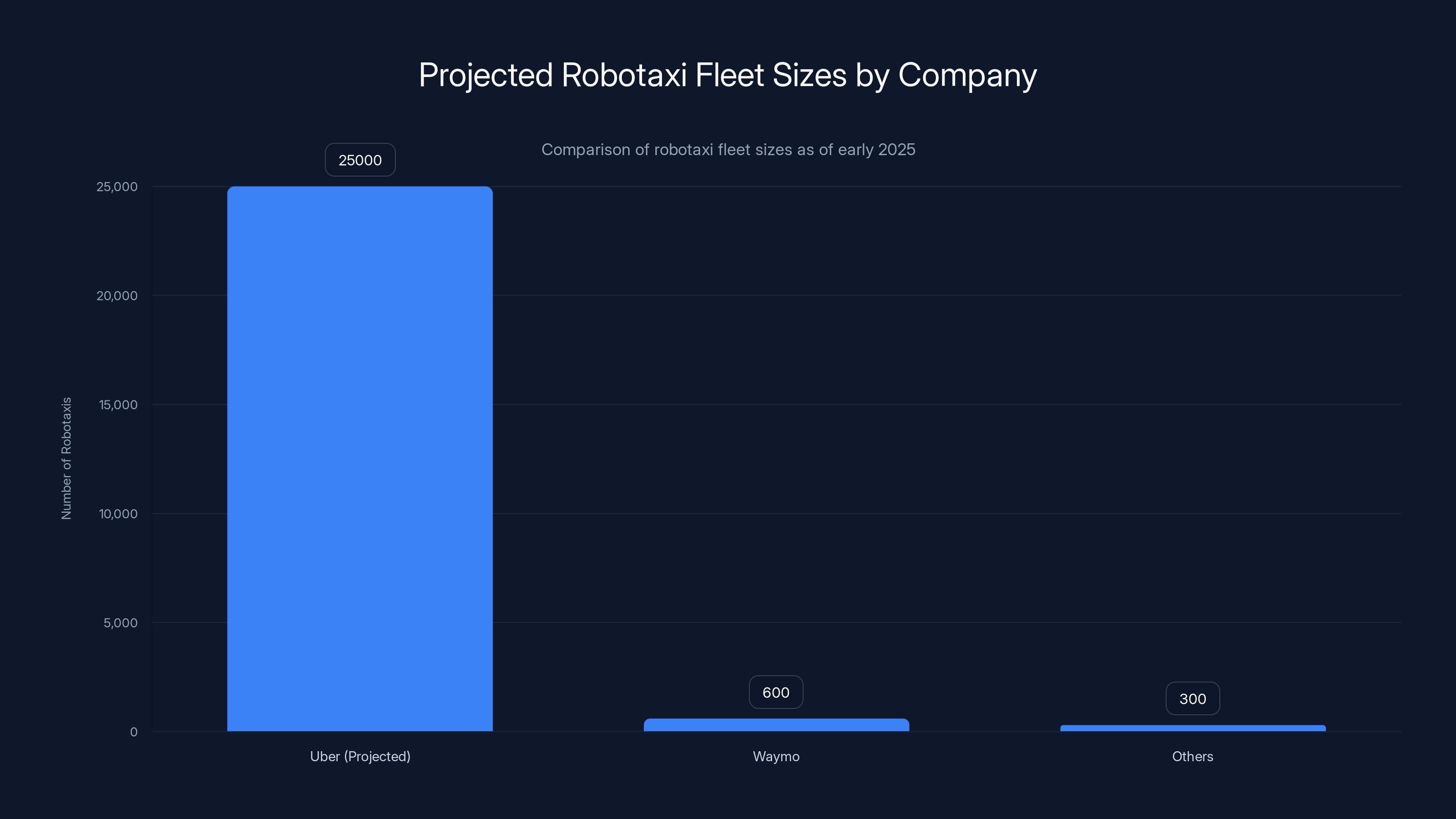

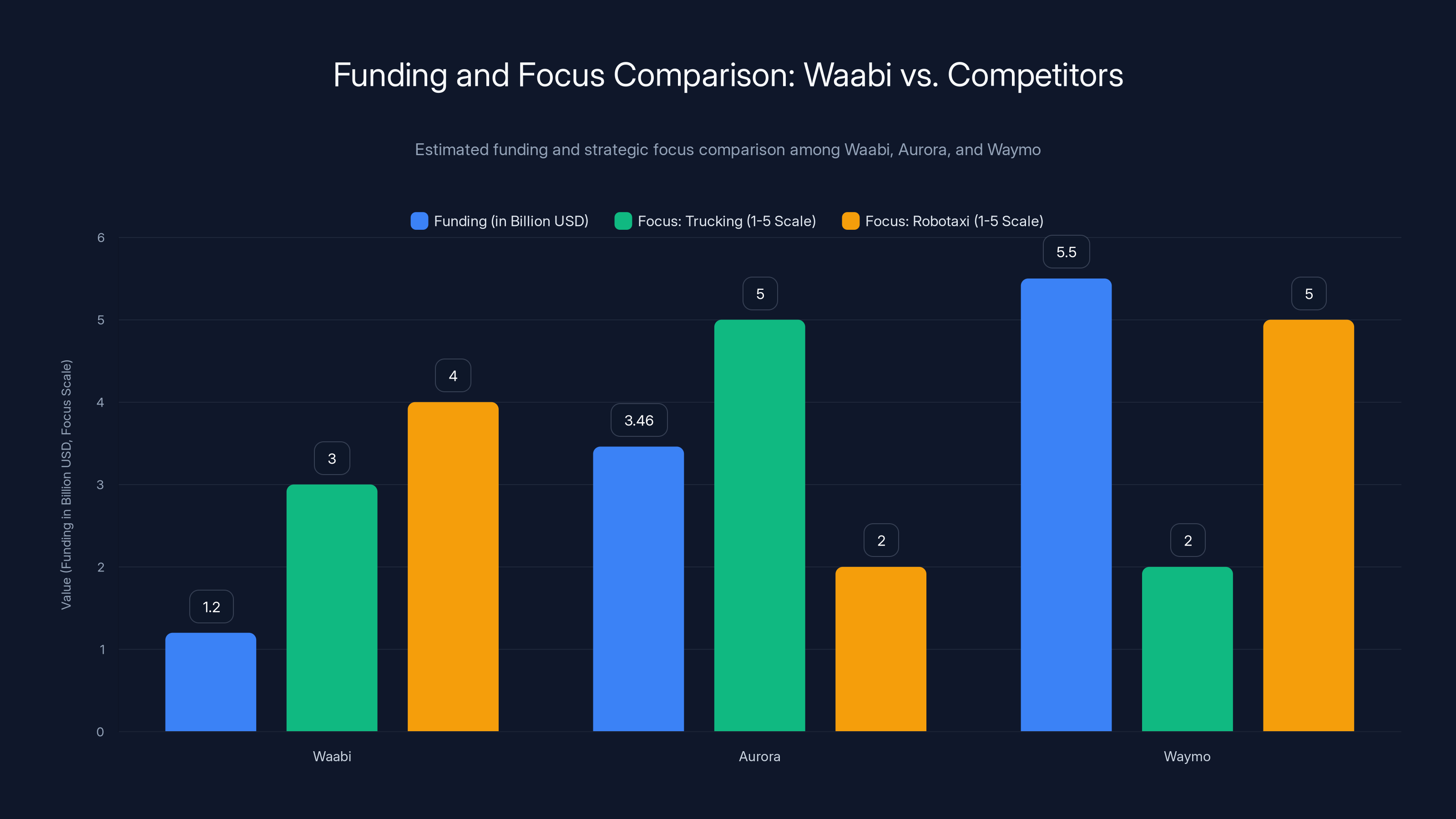

Uber's projected deployment of 25,000 robotaxis significantly surpasses current fleets, highlighting a strategic push into autonomous ride-hailing. Estimated data.

The Uber Partnership: Strategic Implications and Market Strategy

Deployment Timeline and Scale: The 25,000 Robotaxi Target

The commitment to deploy 25,000 or more robotaxis exclusively on Uber's platform represents the largest pre-announced autonomous robotaxi deployment order announced to date by any company. For context, Waymo operates approximately 500-700 robotaxis as of early 2025, while other companies operate smaller pilot fleets. A commitment to 25,000 vehicles, if fully deployed, would represent a 30-50x increase in the autonomous robotaxi fleet size.

Notably, the companies explicitly declined to provide a timeline for this deployment. This suggests either significant technical validation work remains before large-scale production, or regulatory and operational challenges require resolution before deployment can scale. The absence of timeline guarantees also protects both parties if technical or market conditions change. The milestone-based structure of Uber's funding ($250 million paid upon achievement of specified deployment and operational metrics) indicates these milestones likely include demonstration of safety performance, passenger volumes, and economic viability at intermediate deployment scales.

The exclusive deployment agreement on Uber's platform is strategically significant because it gives Uber platform leverage while guaranteeing Waabi a distribution channel. Uber operates in over 70 countries with hundreds of millions of active users, providing a ready market for robotaxi services. For Waabi, the exclusivity arrangement means they won't immediately pursue parallel robotaxi deployment with competing ride-hailing platforms, focusing instead on perfecting operations within the Uber ecosystem.

Manufacturing and Vehicle Integration Strategy

Waabi's commitment to develop purpose-built autonomous vehicles in partnership with Volvo (initially announced at Tech Crunch Disrupt 2024) represents a different strategic approach compared to competitors. Rather than retrofitting existing consumer vehicle platforms with autonomous systems, Waabi is designing vehicles from the ground up to incorporate autonomous driving capabilities. This allows optimization of sensor placement, redundancy architecture, and vehicle dynamics specifically for autonomous operation.

Urtasun emphasized that Waabi would "take a similar route to its autonomous trucking rollout by building its sensors and technology into the vehicle from the factory floor" and highlighted belief in "vertically integrating with a fully redundant platform from the OEM." This indicates the company is designing multiple system redundancy directly into the vehicles rather than relying on aftermarket integration. Full redundancy means critical systems (steering, braking, power, sensor suites) have backup implementations so that single component failures don't compromise safety.

This manufacturing strategy carries implications for cost structure and scalability. Purpose-built autonomous vehicles require significant engineering investment and retooling of manufacturing facilities, but they can achieve better performance and potentially lower per-unit costs at scale compared to retrofitted platforms. The choice of Volvo as a manufacturing partner suggests Waabi selected a company with existing heavy-vehicle manufacturing expertise and the capability to produce commercial quantities of vehicles.

Market Position Within Uber's Autonomous Vehicle Portfolio

Waabi joins an increasingly crowded group of autonomous vehicle technology providers supplying Uber's platform, which includes Waymo, Nuro, Avride, Wayve, We Ride, Momenta, and others. Uber has implemented a multi-vendor strategy rather than betting exclusively on a single autonomous technology provider. This approach provides Uber with negotiating leverage, allows comparison of different technical approaches, and reduces dependency risk on any single company's progress.

For Waabi, the implication is that while the exclusive robotaxi arrangement is significant, the company must still compete technically against other providers operating on Uber's platform. Performance metrics like safety rates, customer satisfaction, operational efficiency, and cost per trip will likely determine how aggressively Uber expands deployment of Waabi's vehicles versus alternatives.

The partnership also positions Waabi alongside Uber's new Uber AV Labs initiative, which will use Uber's vehicle fleet to collect data for autonomous vehicle technology partners. This creates a feedback loop where Waabi can access data generated from robotaxis deployed on Uber's platform, informing improvements to the Waabi Driver architecture. Other technology providers gain the same benefit, creating a shared data commons that benefits the entire ecosystem.

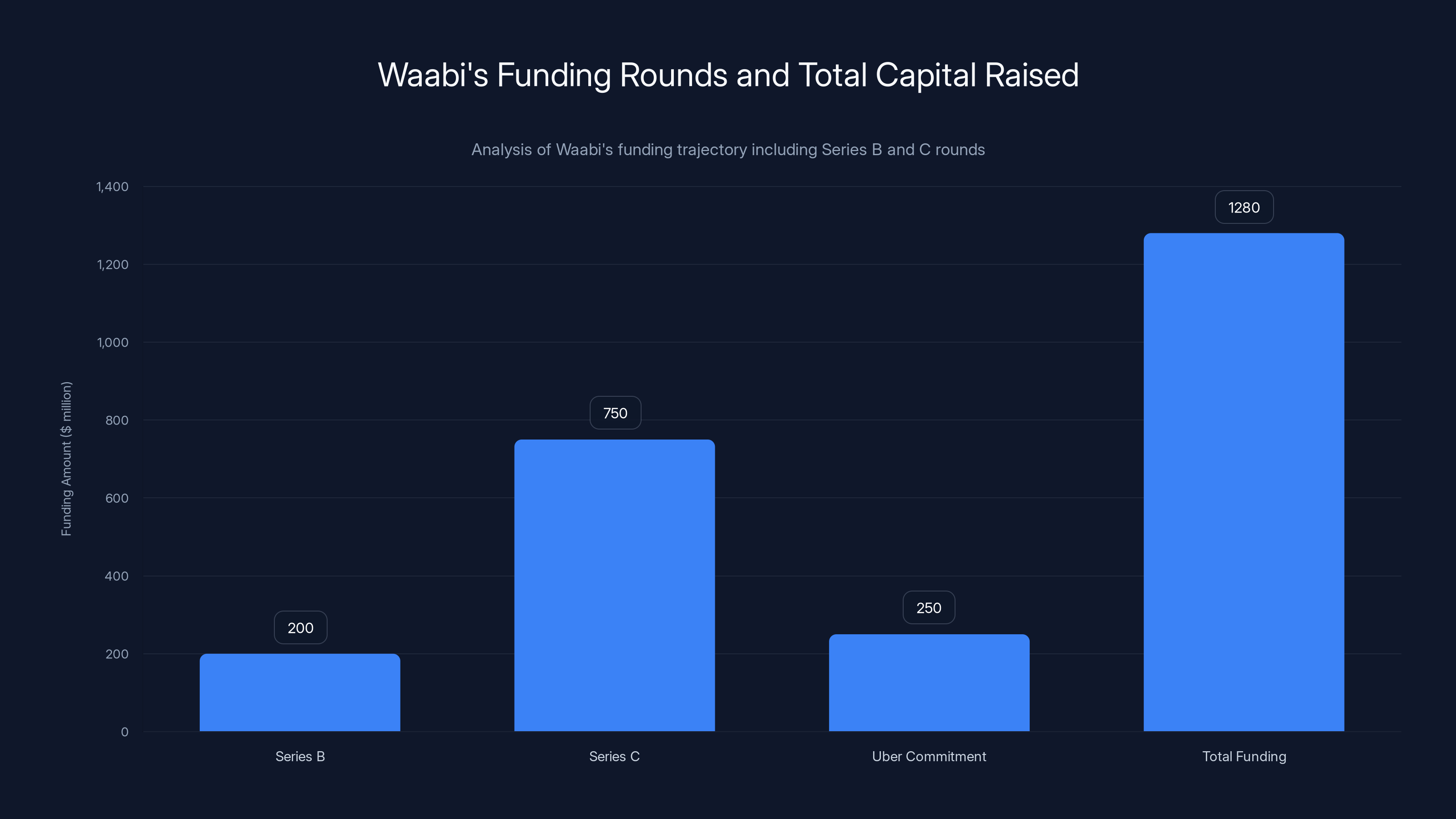

Waabi's funding trajectory shows significant acceleration with

Competitive Landscape: How Waabi Compares to Industry Leaders

Aurora Innovation: The Waymo ATG Acquisition and Trucking Focus

Aurora Innovation represents the most direct competitor in autonomous trucking, having acquired Waymo's autonomous trucking division (Uber ATG) in 2020 and subsequently acquired Uber Freight's autonomous vehicle operations. Aurora has raised approximately $3.46 billion in venture capital and has also secured public market funding through special purpose acquisition company (SPAC) merger, bringing total capital well beyond Waabi's current funding.

Aurora's technical approach emphasizes a modular architecture where autonomous driving capabilities (the Aurora Driver) can be integrated with different vehicle platforms and logistics partners. The company has focused intensely on trucking use cases and has demonstrated multi-mile public deployments in collaboration with partnerships including Cargo Metrics and major logistics companies. Aurora's advantage lies in the substantial capital available for development and deployment, along with the legacy knowledge transferred from Waymo's autonomous trucking program.

However, Aurora's laser focus on trucking means the company has not yet announced major robotaxi initiatives comparable to Waabi's Uber agreement. This represents either a strategic choice (focusing on higher-value trucking first) or a technical limitation (the Aurora Driver may not generalize as effectively to robotaxi use cases). Waabi's ability to pursue both verticals simultaneously with a single architecture potentially offers speed-to-market advantages if the technical claims are validated.

Waymo: The Entrenched Incumbent with Proven Robotaxi Operations

Waymo, owned by Alphabet, remains the autonomous vehicle industry leader by most metrics including operational robotaxi deployments, testing miles, and public perception. Waymo operates the most extensive robotaxi fleets in Phoenix, San Francisco, and Los Angeles, and has demonstrated ability to expand service areas while maintaining strong safety records. Waymo has also invested heavily in autonomous trucking through partnerships with companies like J. B. Hunt, though these have been more limited in scope than initial ambitions.

Waymo's advantages include access to Alphabet's computational resources (critical for AI development and simulation), a decade-plus head start in autonomous vehicle development, strong intellectual property portfolio, and established relationships with vehicle manufacturers, logistics companies, and ride-hailing platforms. Waymo is also not solely dependent on venture capital—Alphabet's balance sheet can fund development indefinitely if strategic priorities align.

Waymo's disadvantage relative to Waabi may be organizational: as a subsidiary of a large technology corporation, Waymo potentially faces slower decision-making processes and less flexibility in partnerships. Waabi, as an independent company, can potentially move more quickly and commit exclusively to specific partners like Uber. Additionally, Waymo's established approach to autonomous driving (heavily data-driven, relying on extensive real-world testing) represents a different technical philosophy than Waabi's simulation-first methodology.

Kodiak Robotics: Truck-Focused Competitor with Limited Robotaxi Ambitions

Kodiak Robotics has raised approximately $448 million and maintains intense focus on autonomous trucking in the Western United States. Kodiak's approach emphasizes developing autonomous driving technology specifically optimized for highway trucking rather than attempting to generalize across multiple vehicle types. This specialized focus allows deep optimization for trucking-specific challenges like long-haul efficiency, complex highway interactions, and heavy vehicle dynamics.

Kodiak's limitation relative to Waabi is the lack of stated ambitions for other verticals like robotaxis, meaning the company's total addressable market is constrained to the trucking segment. While trucking represents a massive market (approximately 3.5 million professional truck drivers in the United States alone), the company cannot benefit from economies of scale across multiple vehicle types using shared technology infrastructure.

International Competitors: Wayve, We Ride, and Momenta

International companies like Wayve (United Kingdom, focused on end-to-end learning approaches), We Ride (China, expanding from robotaxis to autonomous trucking), and Momenta (China, pursuing autonomous trucking and robotaxis) represent emerging competition, particularly in international markets. These companies have pursued different technical approaches and benefit from operating in regulatory environments with potentially different approval timelines.

Wayve's end-to-end learning approach using transformer models trained on video data represents a fundamentally different architecture than traditional modular systems, though the company has faced questions about scalability and performance. We Ride and Momenta have focused on the massive Chinese market where regulatory pathways and user adoption patterns differ from Western markets.

Competitive Summary: Waabi's Distinctive Position

Waabi's distinctive advantages relative to these competitors center on: (1) claimed capital efficiency enabling faster development timelines and lower per-unit economics; (2) unified architecture enabling simultaneous pursuit of trucking and robotaxi markets; (3) exclusive Uber partnership providing distribution advantage in the robotaxi segment; and (4) Urtasun's proven track record and credibility in the autonomous vehicle industry.

The risks relative to competitors include: (1) Waabi's simulation-centric approach remains largely unproven at commercial scale compared to Waymo's real-world proven technology; (2) lower absolute capital compared to Waymo/Aurora potentially limiting resource availability for scaling; and (3) execution risk in simultaneously developing both trucking and robotaxi products when competitors have focused more narrowly.

Financial Analysis: Capital Structure and Valuation Implications

Series C Valuation and Funding Architecture

Waabi's

The Series C led by Khosla Ventures (known for backing deep technology companies with long development timelines) and G2 Venture Partners indicates confidence from sophisticated investors willing to make large bets on unproven but credible technology platforms. Co-leadership structure typically implies competitive tension between lead investors, suggesting strong demand for the round and potentially multiple investors bidding for allocation.

The Uber portion of funding differs structurally from the traditional Series C. Rather than purely venture capital seeking equity appreciation, Uber's $250 million in milestone-based capital functions more like strategic venture debt with success-based repayment. This means Waabi must achieve specific operational milestones (likely including safety certifications, autonomous deployment miles, passenger volumes, and economic metrics) to unlock the full capital commitment. This structure aligns investor incentives with operational outcomes, reducing the risk of capital deployment on unproven capabilities.

Total Capital Raised and Company Trajectory

Waabi's total funding to date now reaches approximately

For context, Waabi was founded in 2020, meaning the company has raised

Burn Rate and Runway Considerations

Autonomous vehicle companies operate at high burn rates because they require: (1) substantial engineering teams (100-500+ software and hardware engineers), (2) fleet operations including vehicle purchase, insurance, and maintenance, (3) data center and computational infrastructure for training and simulation, and (4) regulatory and commercial team costs. Industry estimates suggest autonomous vehicle company burn rates typically range from $50-150 million annually depending on development stage and deployment scope.

Waabi's

This financial runway matters because autonomous vehicle development involves "valley of death" risks where companies can run out of capital before technology demonstrates sufficient maturity for commercial deployment. Waabi's capitalization substantially reduces this risk, allowing the company to pursue long-term technical challenges without the pressure facing less well-funded competitors.

Return on Investment Potential and Valuation Models

The autonomous vehicle industry's potential returns drive the venture capital investment. If autonomous trucking reaches even partial market penetration, the addressable market exceeds

However, this value creation depends entirely on technical execution and commercial adoption actually occurring. If autonomous driving technology proves fundamentally harder to scale than current assumptions (as some skeptics argue), or if regulatory obstacles prevent widespread deployment, the investment returns would be minimal. The Uber partnership reduces this uncertainty by providing commercial deployment commitment, but doesn't eliminate technological execution risk.

Aurora leads in funding with $3.46 billion, focusing heavily on trucking, while Waymo excels in robotaxi operations. Waabi balances both sectors with moderate funding. Estimated data for funding and focus.

Technical Validation and Deployment Timeline

Current Deployment Status in Autonomous Trucking

Waabi has operated pilot programs in Texas with human drivers in the front seat for safety oversight, allowing collection of real-world performance data while maintaining safety guarantees. The company previously announced intentions to deploy fully driverless trucks on public highways by the end of 2024, but this timeline slipped, with Urtasun indicating deployment now expected "sometime in the next few quarters." This multi-quarter timeline suggests 2-3 quarters (six to nine months) from the funding announcement.

The delay reflects typical challenges in autonomous vehicle deployment: regulatory approval processes, validation requirements, and the inherent complexity of transitioning from piloted to fully autonomous operation. While the slip is notable, single-quarter delays in autonomous vehicle timelines are common and don't necessarily indicate fundamental technical issues.

Validation Requirements for Autonomous Trucking

Fully driverless truck deployment requires multiple validation checkpoints: (1) Safety case development demonstrating that autonomous trucks achieve safety levels equal to or exceeding human drivers; (2) Regulatory approval from transportation authorities in deployment states/regions; (3) Insurance validation with liability frameworks for autonomous vehicles; and (4) Customer acceptance from shipping companies and logistics partners willing to contract for autonomous trucking services.

Waabi's approach of developing purpose-built trucks with Volvo enables tight integration of autonomous systems, potentially simplifying validation compared to retrofitted vehicles. The vehicles can be engineered from inception to meet autonomous operation requirements rather than adapting consumer vehicles to autonomous duty.

Robotaxi Deployment Challenges and Timelines

Robotaxi deployment in urban environments faces distinct challenges compared to highway trucking. Urban robotaxis must navigate complex intersections, manage frequent pedestrian interactions, handle unpredictable traffic situations, and provide positive customer experiences in shared vehicles. The transition from pilot programs (limited geography, controlled conditions) to city-wide deployment requires substantially more operational infrastructure.

Uber's 25,000 robotaxi target implies deployment across multiple metropolitan areas and potentially multiple countries within Uber's global network. Even deploying in the 5-10 largest metropolitan areas would represent unprecedented scale in autonomous vehicle operations. The lack of timeline for such deployment reflects the substantial operational unknowns: What customer take-up rates would occur? How would autonomous vehicle failures affect service quality? How would labor markets adjust to large-scale displacement of ride-hailing drivers?

Business Model and Economics Analysis

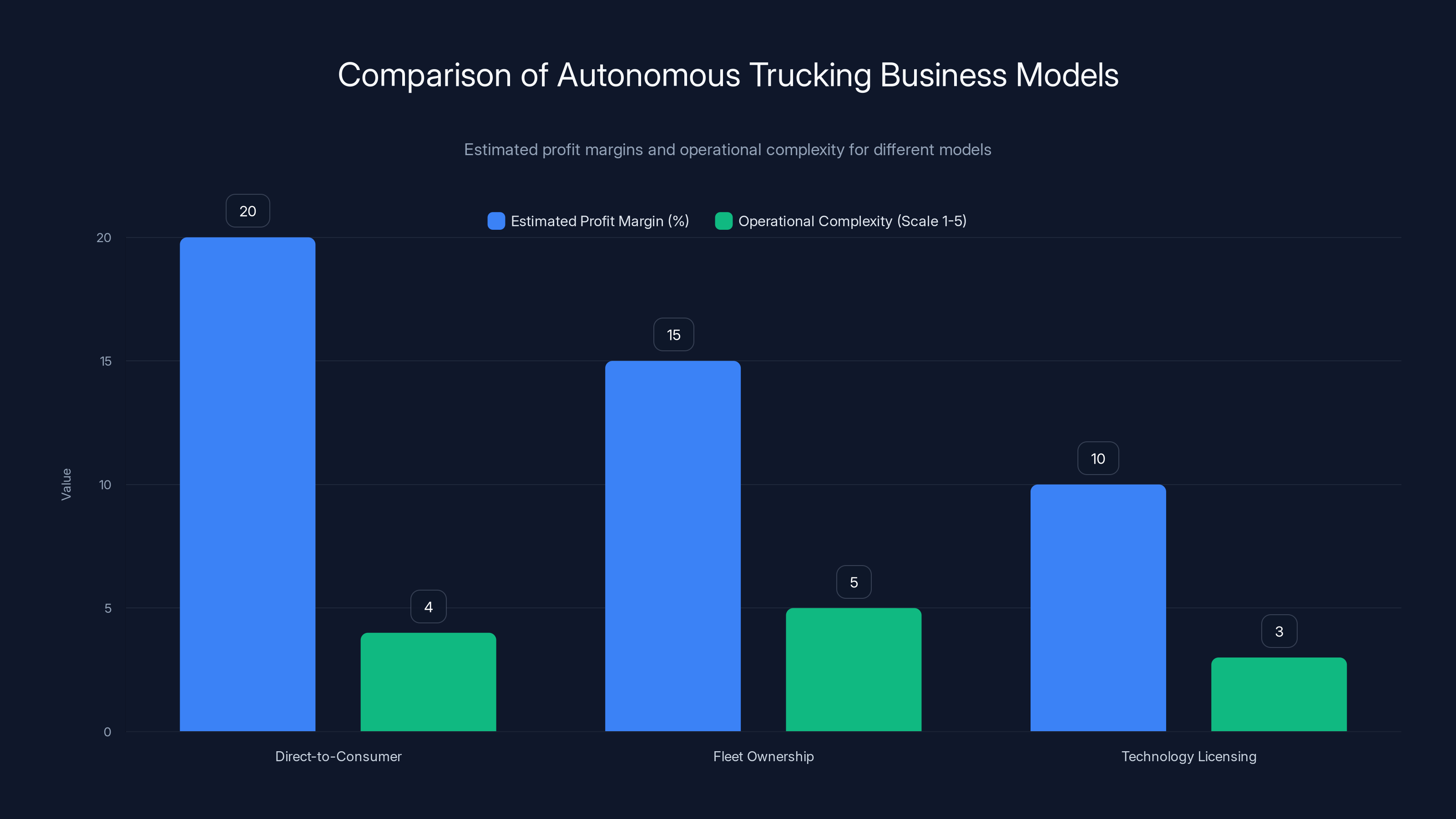

Autonomous Trucking Business Model: Direct-to-Consumer Sales

Waabi's announced approach to autonomous trucking involves selling "purpose-built autonomous trucks" directly to shippers and logistics companies. This direct-to-consumer model contrasts with alternatives like: (1) fleet ownership and operations models where Waabi owns and operates truck fleets; or (2) technology licensing where third parties integrate Waabi's autonomous systems into their own vehicles and operations.

The direct-to-consumer approach enables higher gross margins because Waabi captures vehicle sale margins (potentially 15-25% of vehicle cost) in addition to technology licensing fees. However, the model requires Waabi to establish manufacturing relationships, manage supply chains, and support customer deployments—all complex business functions beyond pure technology development. The announced Volvo partnership likely handles vehicle manufacturing, with Waabi integrating autonomous systems and potentially handling customer sales and support.

Financial models for autonomous trucking typically project the autonomous truck purchase price at a premium of 20-40% above conventional trucks (approximately

Robotaxi Business Model: Revenue Sharing with Uber

Waabi's robotaxi business model appears to involve revenue sharing with Uber, though specific terms haven't been publicly disclosed. Comparable robotaxi arrangements (such as Waymo's partnership with Uber) typically involve Uber retaining 70-80% of fare revenue with the technology provider (Waabi) retaining 20-30% as compensation for providing the autonomous driving technology.

This structure aligns incentives: Waabi profits when robotaxis operate successfully and generate high utilization, while Uber captures the consumer-facing platform value and customer relationship. Uber handles fleet management, customer service, and platform operations, while Waabi provides the core autonomous technology.

Revenue generation at scale is straightforward: if 25,000 autonomous vehicles achieve average daily utilization of 8-10 hours across 300 operating days annually, the fleet generates approximately 60-75 million vehicle hours annually. At average fares of

Cost Structure and Path to Profitability

Autonomous vehicle operations costs break into: (1) Vehicle capital costs (depreciation and interest on fleet investment); (2) Operations costs (maintenance, insurance, charging/fuel, parking, cleaning); (3) Technology development (continued R&D maintaining competitive advantage); and (4) Commercial operations (customer support, fleet management, regulatory compliance).

Waymo's publicly disclosed robotaxi operations data suggests per-mile operating costs (excluding vehicle capital) of approximately

Assuming similar economics for Waabi, full deployment of 25,000 vehicles generating 2.4-3 billion miles annually could achieve profitability if Waabi's technology cost per mile is sufficiently low. At a 25% margin assumption (capturing value from lower operating costs versus human drivers), full deployment could generate $150-250 million in annual profit, justifying the current valuation and providing substantial returns to early investors.

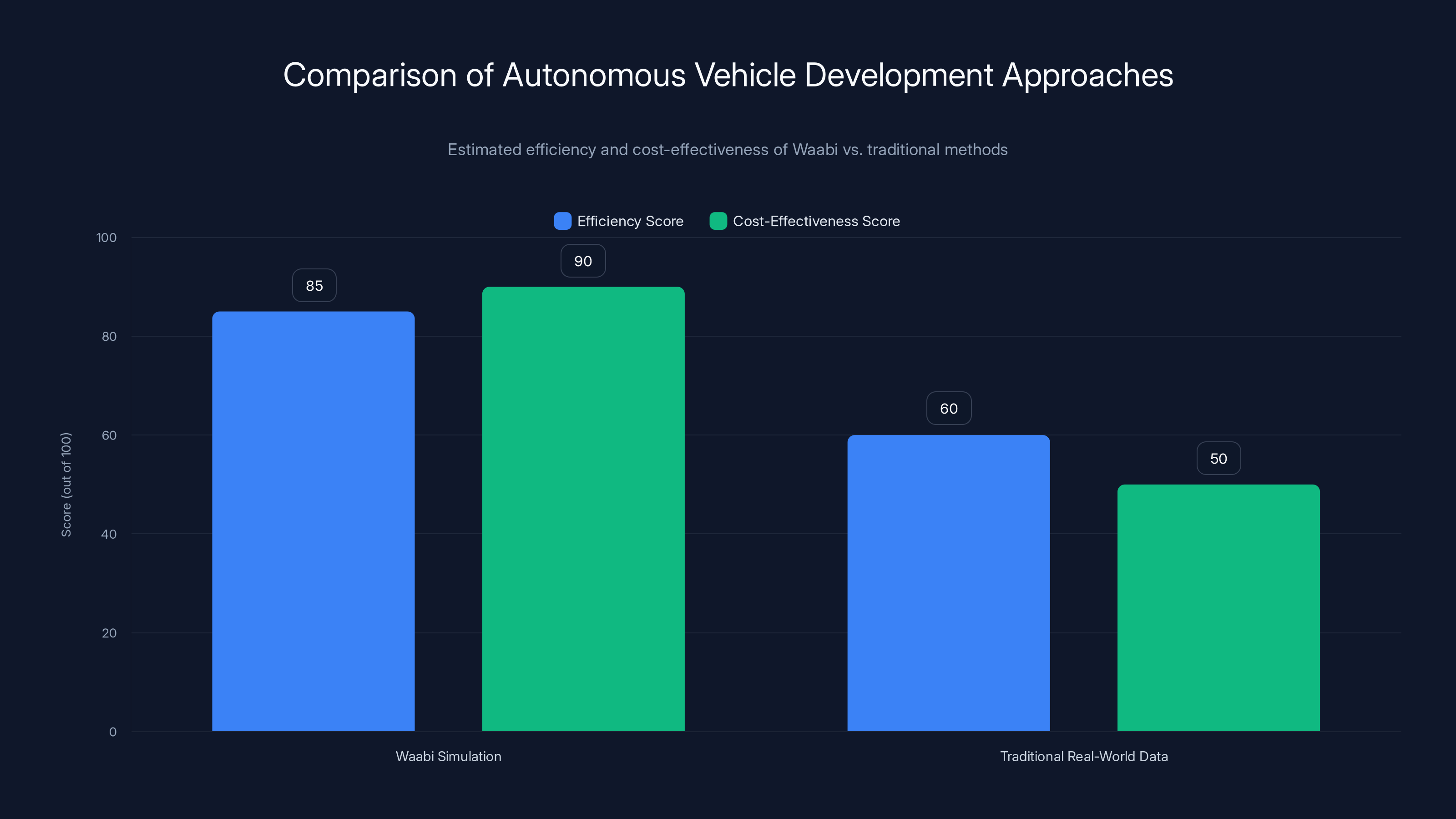

Waabi's simulation-driven approach is estimated to be more efficient and cost-effective compared to traditional real-world data collection methods, potentially accelerating development timelines. (Estimated data)

Regulatory Environment and Deployment Challenges

Autonomous Vehicle Regulatory Framework

Autonomous vehicle deployment operates within a complex regulatory environment that has evolved substantially since autonomous driving concepts emerged. Key regulatory dimensions include: (1) Vehicle safety standards established by the National Highway Traffic Safety Administration (NHTSA) in the United States, and comparable agencies in other countries; (2) Operational permits and state-level approval requirements for testing and commercial deployment; (3) Insurance and liability frameworks determining fault and financial responsibility; and (4) Data privacy and cybersecurity standards governing collection and use of vehicle and passenger data.

Unlike traditional vehicles where manufacturers prove compliance with fixed safety standards, autonomous vehicle approval operates under more flexible frameworks. NHTSA issues guidance rather than mandatory regulations in many areas, creating ambiguity but also flexibility for new technologies. This regulatory flexibility has enabled Waymo, Cruise (though now shuttered), and others to deploy robotaxis, but also creates uncertainty about future requirements.

State-Level Deployment Variations

Autonomous vehicle deployment regulations vary substantially by state and country. Some jurisdictions (Arizona, California, parts of Texas) have relatively permissive frameworks allowing extensive autonomous vehicle testing and deployment. Others maintain stricter approval processes or explicitly prohibit full autonomy. This fragmentation creates operational complexity for companies pursuing nationwide deployment.

Waabi's focus on Texas for initial trucking pilots exploits this state's relatively favorable regulatory environment. Expansion to other trucking corridors (I-95 on the East Coast, I-70 through the Midwest) would require navigation of different state regulatory frameworks, potentially slowing geographic expansion.

Insurance and Liability Considerations

The insurance and liability framework for autonomous vehicles remains incompletely developed. Traditional vehicle insurance policies cover driver negligence, but autonomous vehicles raise novel questions: If an autonomous vehicle causes an accident, is the manufacturer liable? The fleet owner? The software provider? Current frameworks assume human drivers bear primary responsibility, an assumption invalid for fully autonomous vehicles.

Progress toward resolving these questions varies geographically. Some states have implemented autonomous vehicle liability frameworks; others rely on existing insurance law adapted to autonomous contexts. This regulatory uncertainty, while declining, still represents a deployment risk for companies like Waabi expanding operations across jurisdictions.

Data Privacy and Cybersecurity Standards

Autonomous vehicles collect extensive data including vehicle telemetry, sensor data, passenger behavior, and location information. Regulatory frameworks governing collection, storage, and use of this data increasingly impose strict requirements. The European Union's GDPR framework, for instance, creates substantial compliance requirements for companies operating in European markets.

Cybersecurity represents an additional regulatory concern. Autonomous vehicles represent potential targets for hackers who could compromise safety systems or access sensitive data. Regulatory frameworks increasingly mandate cybersecurity standards and breach reporting requirements, imposing compliance costs on companies operating autonomous vehicles.

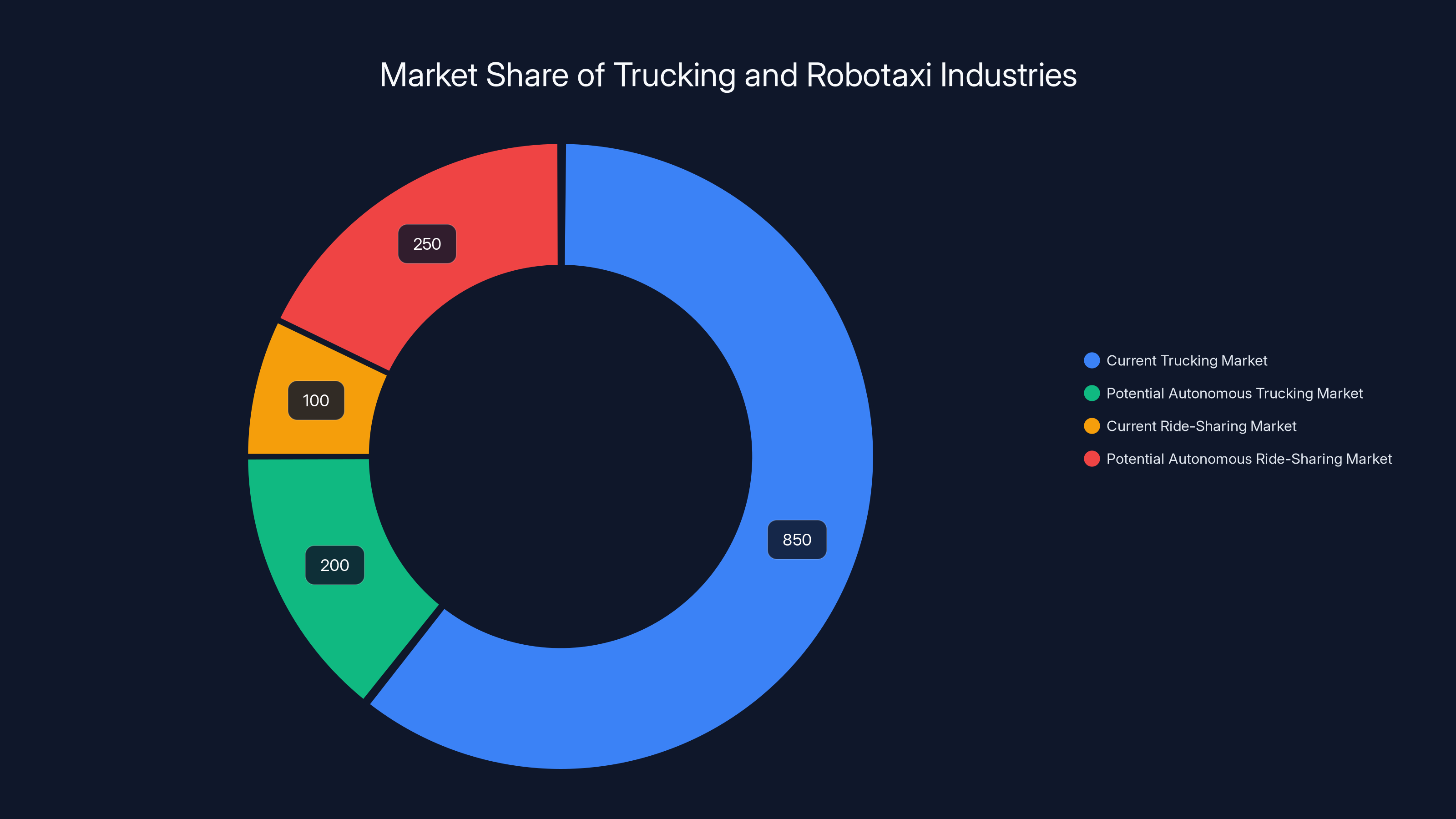

Market Size and Total Addressable Market Analysis

Trucking Market Opportunity

The long-haul trucking market represents the more immediate and addressable opportunity. The United States trucking industry generates approximately

Key market drivers for autonomous trucking include: (1) driver shortage (trucking industry faces chronic driver shortages, creating pressure to automate); (2) labor cost escalation (truck driver wages increasing faster than inflation, making automation economics attractive); (3) fuel efficiency gains (autonomous vehicles can optimize routing and driving patterns for efficiency); and (4) safety improvement (autonomous vehicles potentially achieving better safety records than human drivers).

International markets provide additional opportunities. The European trucking market is similarly sized, and international logistics companies increasingly pursue autonomous trucking capabilities. Waabi's potential expansion beyond the U. S. could access these larger markets over time.

Robotaxi Market Opportunity

The robotaxi market opportunity is substantially larger than trucking but more speculative and longer-term. The global ride-sharing market generates approximately

Key market dynamics for robotaxis include: (1) consumer acceptance (riders must trust autonomous vehicles, currently uncertain); (2) regulatory approval (local approval processes required for each geographic market); (3) capital efficiency (ability to operate profitably at lower margins than human driver-operated services); and (4) network effects (larger robotaxi fleets provide better service coverage and frequency, attracting more riders).

Waabi's Uber partnership provides significant advantage in the robotaxi market by leveraging Uber's existing user base, brand recognition, and operational infrastructure. This distribution advantage could accelerate market capture relative to autonomous vehicle companies lacking ride-hailing partnerships.

Market Penetration Scenarios and Timeline Assumptions

Projecting autonomous vehicle market penetration remains highly uncertain, with analyst forecasts varying widely depending on assumptions. Conservative scenarios assume autonomous trucking reaches 30-40% market penetration by 2035-2040, with robotaxis reaching 20-30% penetration in major metropolitan areas over similar timeframes. Optimistic scenarios assume faster adoption with 50%+ penetration by 2035 for trucking and 40-50% for robotaxis in developed markets.

Waabi's penetration will depend on relative competitive performance, execution on promised capabilities, and capital available for scaling operations. The $1 billion funding provides substantial resources, but competitors like Waymo and Aurora also have significant capital and head starts, meaning Waabi must execute better or faster to capture disproportionate market share.

The direct-to-consumer model offers higher profit margins (estimated 20%) but involves significant operational complexity. Fleet ownership has the highest complexity, while technology licensing is simpler but less profitable.

Technical Risks and Execution Challenges

The Simulator Validation Problem

Waabi's simulation-centric approach introduces a fundamental technical risk: reality gap—the potential that behaviors learned in simulation don't transfer effectively to real-world conditions. Historically, researchers have struggled with reality gaps in robotics and autonomous systems, requiring extensive real-world fine-tuning even after successful simulation performance.

Waabi's Waabi World simulator aims to reduce this gap by building digital twins from real-world data and performing real-time sensor simulation. However, the completeness of this simulation remains unvalidated at full commercial scale. Edge cases—unusual situations the simulator hasn't encountered—could surface in real-world operations, requiring retraining and potentially causing safety incidents.

Addressing this risk requires extensive validation: Waabi must demonstrate that simulation-trained driving systems achieve safety parity with real-world tested systems. The comparison against Waymo's extensively real-world-validated technology provides a natural benchmark—if Waabi's performance matches Waymo's despite different development approaches, the simulation methodology gains credibility.

Generalization Across Vehicle Types: Validation Required

The claim that a single AI architecture can handle autonomous trucking and robotaxis, with hints toward robotics applications, remains unproven. While conceptually plausible (both tasks involve perception, prediction, and decision-making), the real-world validation requires demonstrating comparable performance across these distinct domains. No company has yet clearly demonstrated this generalization capability at commercial scale.

Risks include: (1) the architecture works well for trucking but requires substantial modification for robotaxis (suggesting the generalization claim is overstated); (2) safety and regulatory requirements differ by domain, preventing true architectural generalization; or (3) the system achieves acceptable performance in both domains but at lower levels than domain-specialized competitors, limiting competitive advantage.

Distributed Teams and Engineering Complexity

Autonomous vehicle development involves complex engineering requiring coordination across: hardware engineers (sensor systems, vehicle integration), software engineers (computer vision, prediction, planning, control), machine learning engineers (model training, reinforcement learning), and systems engineers (safety validation, software architecture). Coordinating these specialties across a growing organization presents substantial management complexity.

Waabi's founding team brings credibility (Urtasun's academic and industry background) but the company must attract and retain top-tier talent to execute against well-resourced competitors. Engineering talent in autonomous vehicles remains scarce and highly competitive, creating retention risks as company valuations increase (making employee equity less valuable) and competitive opportunities emerge.

Strategic Implications and Industry Trends

The Multi-Vendor Approach to Autonomous Vehicles

Uber's strategy of working with multiple autonomous vehicle providers (Waabi, Waymo, Nuro, Avride, Wayve, We Ride, Momenta) reflects a shift from previous assumptions that a single autonomous vehicle solution would dominate. This multi-vendor approach has precedent in other technology domains—cloud computing with AWS, Azure, and Google Cloud; smartphone operating systems with i OS and Android—where platform companies host multiple technology providers rather than betting on a single solution.

For Waabi, the multi-vendor environment creates both opportunity and risk. Opportunity: the company can succeed by differentiating on specific dimensions (cost, safety, customer experience) rather than capturing 100% of Uber's robotaxi fleet. Risk: Uber could easily shift away from Waabi to competing providers if superior alternatives emerge, or if Waabi fails to meet operational targets.

Capital Efficiency as Competitive Moat

Waabi's emphasis on capital efficiency—developing autonomous systems with fewer engineers, data centers, and collected miles compared to competitors—could establish a meaningful competitive advantage. If Waabi achieves comparable technology performance to Waymo while consuming only 40-50% of the capital and time, the company gains a sustainable advantage that's hard to overcome through incremental improvements by competitors.

Capital efficiency advantages become increasingly important if autonomous vehicle investment cycles extend further (if technology development takes 15-20 years rather than 10-12 years). In extended timelines, more capital-efficient companies can reach market with fresher technology and maintain funding advantages. Conversely, if technology reaches commercial maturity in 5-10 years, the capital efficiency advantage becomes less significant.

Consolidation and Strategic Acquisitions

The autonomous vehicle industry has already experienced significant consolidation: Uber sold ATG to Aurora; Cruise faced layoffs and reduced focus; multiple smaller companies shut down. Future industry consolidation likely continues, with well-capitalized companies acquiring technology and talent from struggling competitors. Waabi's strong funding position and exclusive Uber partnership reduce acquisition risk (Waabi is unlikely acquisition target given Uber's strategic commitment), but also means the company faces continued pressure to execute and maintain performance advantages.

The current U.S. trucking market is valued at

Comparisons to Alternative Autonomous Vehicle Approaches

End-to-End Learning vs. Modular Architectures

Autonomous vehicle architectures diverge fundamentally on whether to use end-to-end learning (feeding raw sensor data into neural networks that learn to output driving commands) or modular architectures (separate perception, prediction, and planning modules assembled together). Wayve pursues end-to-end approaches using transformer models trained on video data. Waymo and Aurora employ modular architectures with distinct components for each driving task.

Waabi's architecture appears modular based on descriptions of perception, prediction, and decision-making components, though the company hasn't published detailed technical specifications. Modular approaches offer interpretability (easier to understand why systems make decisions) and testability (individual components can be validated), advantages important for safety-critical autonomous driving. End-to-end approaches potentially offer better performance through unified optimization but sacrifice interpretability and create challenges in failure analysis.

Human-in-the-Loop Development vs. Purely Autonomous Development

Some autonomous vehicle companies maintain human operators in vehicles during testing and early deployment to intervene if systems fail. Waymo explicitly emphasized this approach in early deployments, with safety drivers ready to take control. Waabi's piloted trucking deployments similarly employ human drivers in the front seat for safety oversight.

This human-in-the-loop approach provides safety guarantees during development but slows deployment because human operators must be employed and trained. Eventually, full autonomy requires removing humans, but the intermediate phase allows extensive real-world validation. Waabi's timeline for transitioning from piloted to fully driverless reflects this approach.

Simulation-First vs. Real-World Data Collection First

Waabi's simulation-first approach contrasts with competitors like Waymo that prioritized extensive real-world data collection. Simulation-first offers potential advantages in development speed and capital efficiency, but requires exceptional quality in the simulator to avoid reality gaps. Real-world data collection provides ground truth but incurs substantial ongoing costs.

The optimal approach likely blends both: simulation for initial development and edge case exploration, real-world data for validation and continuous improvement. Waabi's integration of real-world data into Waabi World digital twins suggests recognition that simulation alone proves insufficient.

Investment and Market Outlook

Venture Capital Interest in Autonomous Vehicles

Autonomous vehicle funding has cycled through booms and busts as technological capability versus expectations periodically misaligned. The current funding cycle, demonstrated by Waabi's $1 billion raise, suggests renewed venture capital confidence following years of skepticism about overhyped autonomous vehicle capabilities. This confidence partly reflects: (1) concrete deployments by Waymo demonstrating technology maturity; (2) regulatory pathways clarifying for autonomous operations; and (3) economic incentives (labor shortages, efficiency potential) driving continued investment.

Waabi's successful fundraising, combined with continued interest from Uber and other platform companies, suggests venture capital views autonomous vehicles as a justified long-term investment opportunity despite previous disappointments. The $1 billion raise signals investor confidence in both Waabi specifically and autonomous vehicle market timing more broadly.

Exit Strategies and Return Timelines

Venture capital autonomous vehicle investments operate on unusually long timelines compared to typical software startups. Rather than expecting exits in 5-7 years, investors anticipate 10-15+ year development and commercialization phases. This extended timeline affects investor expectations and capital structures—later-stage investors like Khosla Ventures often accept longer returns in exchange for better valuation and downside protection.

Waabi's potential exit paths include: (1) IPO (going public through direct listing or SPAC merger, following Aurora's path); (2) Strategic acquisition by an automotive manufacturer, logistics company, or ride-hailing platform seeking to internalize autonomous vehicle capabilities; or (3) Sustained private operations with venture investors achieving returns through internal cash generation and buybacks. The Uber partnership might itself lead to eventual acquisition of Waabi by Uber if the partnership proves sufficiently valuable.

Future Outlook and Evolution Possibilities

Expansion Beyond Trucking and Robotaxis

Urtasun has hinted that robotics represents the next vertical beyond autonomous vehicles. If Waabi's architecture truly generalizes across vehicle form factors, the application to robotics (autonomous forklifts, warehouse robots, delivery robots) represents substantial additional markets. These specialized robotics applications often operate in constrained environments (warehouses, delivery zones, industrial sites) where approval and deployment timelines could be faster than open-road autonomous vehicles.

The total addressable market for autonomous robotics in warehousing, logistics, and delivery potentially rivals or exceeds autonomous vehicle markets. Success in these areas would validate the generalization claim and create multiple revenue streams using shared technology infrastructure.

International Expansion and Regulatory Navigation

Waabi's initial focus on the United States reflects the large trucking and ride-sharing markets and relatively favorable regulatory environment. However, international markets like Europe, China, and Japan represent additional opportunities. Each region operates under different regulations, presents different customer behaviors, and involves different competitive landscapes.

Expansion to European markets potentially involves dealing with stricter GDPR requirements and more cautious regulatory approval processes. Expansion to Asian markets potentially involves competing against entrenched local competitors and different labor market dynamics. Waabi's strategy for international expansion, still unarticulated, will significantly affect long-term market reach and profitability.

Technology Evolution and Computational Requirements

The computational requirements for autonomous vehicles continue evolving as algorithms advance and training data accumulates. Future iterations of Waabi's technology may require substantially different computational architectures (leveraging specialized AI accelerators, edge computing, or quantum computing if applicable). Maintaining technological currency while managing the installed base of deployed vehicles (which require backwards-compatible updates) presents ongoing technical challenges.

The energy consumption of training large autonomous driving models remains substantial—Waabi's claim of not needing "a gazillion latest chips" or "massive data centers" may prove optimistic if the technology requires scaling to handle increasing complexity. This creates a potential competitive vulnerability if competitors with greater computational resources develop notably superior performance through brute-force scaling.

Summary and Key Takeaways

Waabi's $1 billion funding round and exclusive Uber robotaxi partnership represent significant milestones in the autonomous vehicle industry's evolution toward commercial deployment at scale. The company's technical approach emphasizing capital efficiency, simulation-driven development, and generalization across vehicle types offers a distinct alternative to competitors' heavily real-world-focused methodologies.

The exclusive Uber robotaxi partnership provides substantial strategic advantage by guaranteeing distribution through the world's largest ride-hailing platform, though success requires continued technical validation and operational execution. The 25,000 robotaxi deployment target, if achieved, would represent unprecedented scale in autonomous vehicle operations and validate core technology assumptions.

Waabi's competitive position relative to Waymo, Aurora, and international competitors depends ultimately on execution: demonstrating that simulation-trained autonomous systems achieve safety and operational performance comparable to real-world validated alternatives; proving that unified architectures can handle multiple vehicle types without sacrificing performance in any; and navigating complex regulatory and operational challenges as deployment scales from pilots to city-wide operations.

The funding success indicates investor confidence in both Waabi and autonomous vehicle market timing broadly. However, autonomous vehicles remain a high-risk, long-duration investment where technology achievements don't guarantee commercial success. Regulatory approval, customer adoption, competitive responses, and unexpected technical challenges all remain potential obstacles to realizing projected returns.

For the autonomous vehicle industry, Waabi's progress represents validation of alternative development approaches (simulation-first, capital-efficient) that could ultimately prove superior to earlier companies' methodologies. If Waabi succeeds, the company's approach becomes the template for future autonomous vehicle development. If the company struggles, execution challenges rather than methodology failures likely explain the shortfall.

FAQ

What is Waabi and what does the company do?

Waabi is an autonomous vehicle technology company founded by Raquel Urtasun that develops artificial intelligence systems for self-driving trucks and robotaxis. The company uses a closed-loop simulator called Waabi World to train its autonomous driving system, which can handle both highway trucking and urban robotaxi operations using the same underlying AI architecture. Waabi aims to make autonomous vehicle development more capital-efficient than competitors through simulation-driven training rather than relying exclusively on real-world data collection.

How does Waabi's simulation technology work?

Waabi World is a closed-loop simulator that automatically builds digital twins of the real world from collected data, performs real-time sensor simulation to model how different sensors behave in various conditions, and manufactures challenging scenarios to stress-test the Waabi Driver AI system. The simulator enables the Waabi Driver to learn from mistakes without human intervention, allowing the system to develop driving capabilities more efficiently than traditional approaches relying primarily on real-world miles. The technology trains the autonomous driving system to reason about surroundings as humans would and select optimal driving maneuvers.

What is the significance of the Uber partnership?

Uber has committed approximately

How does Waabi's approach differ from competitors like Waymo and Aurora?

Waabi emphasizes capital-efficient development using simulation-driven training, whereas Waymo has focused on extensive real-world data collection and testing over 15+ years, and Aurora (which acquired Uber's autonomous trucking division) emphasizes a modular technology architecture. Waabi claims to generalize across multiple vehicle types using a single AI architecture, while most competitors have specialized in either trucking or robotaxis separately. Waabi's approach potentially allows faster development and lower capital requirements, but the simulation-first methodology remains less proven at commercial scale compared to Waymo's extensively tested real-world systems.

When will Waabi deploy fully autonomous vehicles?

Waabi previously announced plans to deploy fully driverless trucks on public highways by the end of 2024, but this timeline slipped and Urtasun now indicates deployment expected "sometime in the next few quarters" (suggesting 2-3 quarters from the funding announcement). The company is currently operating piloted truck deployments in Texas with human drivers for safety oversight. For robotaxis, no specific timeline has been announced for the Uber deployment, though the 25,000 vehicle target suggests a multi-year rollout period rather than immediate deployment.

What is Waabi's business model and how will the company generate revenue?

Waabi employs two business models: in autonomous trucking, the company sells purpose-built trucks directly to shippers and logistics companies through manufacturing partnerships with companies like Volvo; in robotaxis, Waabi provides autonomous driving technology to Uber and likely shares in fare revenue generated from successful robotaxi operations. The autonomous trucking model generates revenue from vehicle sales and ongoing service fees, while the robotaxi model involves profit-sharing on passenger trips, likely structured so Uber retains 70-80% of fare revenue and Waabi receives 20-30% as compensation for technology and ongoing support.

How much total funding has Waabi raised?

Waabi has raised approximately

What are the main technical risks for Waabi's approach?

Key technical risks include: the potential reality gap where simulation-trained driving behavior doesn't transfer effectively to real-world conditions (a challenge with robotics and autonomous systems historically); unvalidated claims that a single AI architecture can handle both trucking and robotaxis equally well; potential discovery that simulation quality proves insufficient for edge cases encountered in real-world operations; and continued evolution of computational requirements potentially negating capital efficiency advantages if substantially more computation becomes necessary for advanced capabilities.

How does Waabi's funding compare to competitors?

Waabi's

What is the addressable market opportunity for Waabi's technology?

Waabi operates in two major markets: autonomous trucking (approximately

What regulatory challenges does Waabi face for deployment?

Waabi must navigate multiple regulatory frameworks including: National Highway Traffic Safety Administration (NHTSA) safety standards and guidance; state-level permitting and approval processes that vary by jurisdiction; insurance and liability frameworks that remain incompletely developed for fully autonomous vehicles; and data privacy standards like the European Union's GDPR if expanding to international markets. The fragmented regulatory environment creates complexity but also allows focus on more permissive jurisdictions for initial deployment before expanding to stricter regulatory environments as the technology matures and gains validation.

Alternative Solutions and Competitors to Waabi

While Waabi represents an innovative approach to autonomous vehicle development, several alternative solutions and competing approaches merit consideration depending on specific use cases and priorities. For teams and organizations evaluating autonomous vehicle technology partnerships or investments, understanding these alternatives provides important context for decision-making.

Waymo: The Proven Robotaxi Leader

Waymo remains the most established autonomous vehicle company with proven robotaxi operations in Phoenix, San Francisco, and Los Angeles, and autonomous trucking partnerships with logistics companies. Waymo's advantages include proven real-world operational experience, extensive intellectual property, access to Alphabet's computational resources, and regulatory approval in multiple jurisdictions. For organizations prioritizing proven technology maturity and established operational frameworks, Waymo represents the conservative choice with the lowest execution risk.

Aurora Innovation: Capital-Rich Trucking Specialist

Aurora Innovation, which acquired Uber's autonomous trucking division, represents the most heavily capitalized trucking-focused autonomous vehicle company with $3.46 billion in funding. Aurora's approach emphasizes modular architecture and partnerships with logistics companies and vehicle manufacturers. For organizations seeking specialized autonomous trucking solutions with proven capital availability and industry partnerships, Aurora provides an alternative with substantial resources and established relationships.

International Alternatives: Wayve, We Ride, and Momenta

International companies like Wayve (UK-based, pursuing end-to-end learning approaches), We Ride (China, expanding to trucking), and Momenta (China, pursuing both robotaxis and trucking) offer geographic and technical alternatives. These companies often operate with different capital structures, technical approaches, and regulatory pathways compared to U. S.-based companies. For organizations with international operations or specific geographic focuses, these alternatives provide localized solutions aligned with regional market dynamics.

Runable: AI-Powered Automation for Content and Workflows

For organizations seeking AI-powered automation capabilities beyond autonomous vehicles specifically, platforms like Runable offer broader automation solutions applicable to business processes, content generation, and workflow automation. Runable provides AI agents for document generation, slide creation, report automation, and workflow automation at a cost-effective price point ($9/month), making it suitable for teams prioritizing productivity automation across multiple domains rather than autonomous vehicle technology specifically. While not a direct autonomous vehicle alternative, Runable represents a different approach to AI-powered automation that teams evaluating technology investments might consider for complementary business applications.

Key Takeaways

- Waabi's 750M venture + $250M from Uber) demonstrates renewed investor confidence in capital-efficient autonomous vehicle development

- Exclusive Uber robotaxi partnership commits to deploying 25,000+ vehicles, providing major distribution advantage but requiring successful execution

- Simulation-first development approach using Waabi World digital twins offers capital efficiency advantages over real-world-focused competitors like Waymo

- Claimed generalization across trucking and robotaxis using unified AI architecture differentiates Waabi but remains unproven at commercial scale

- Competitive landscape includes well-funded rivals like Aurora ($3.46B), established leader Waymo, and international competitors, making execution critical

- Total addressable market exceeds $300+ billion across trucking and robotaxi segments if autonomous vehicles achieve regulatory approval and consumer adoption

- Technical risks include reality gap between simulation and real-world performance, unvalidated multi-vertical claims, and continued computational requirement evolution

- Financial projections suggest potential for $10-60B in revenue if Waabi captures 10-20% of addressable markets, justifying venture valuations

- Regulatory challenges vary by jurisdiction and require navigation of complex safety, liability, and privacy frameworks for deployment at scale

- Investment success depends on validating simulation methodology, delivering announced capabilities on timelines, and competing effectively against resourced rivals

Related Articles

- Waabi Uber Robotaxi Deal: $1B Funding & 25,000 Vehicles Explained

- Robotaxis Disrupting Ride-Hail Markets in 2025: Price War and Speed [2025]

- Elon Musk's Davos Predictions: Why They Keep Missing [2025]

- Waymo's Miami Robotaxi Launch: What It Means for Autonomous Vehicles [2025]

- Tesla's Dojo Supercomputer Restart: What Musk's AI Vision Really Means [2025]

- Hyundai's Autonomous Robotaxi: Las Vegas Launch & Future of Self-Driving