![Which Countries Are Building Sovereign Space Rockets [2025]](https://tryrunable.com/blog/which-countries-are-building-sovereign-space-rockets-2025/image-1-1771348059387.jpg)

Which Countries Are Building Sovereign Space Rockets [2025]

For decades, the space launch industry was a game played by superpowers. The United States, the Soviet Union, and later China controlled access to orbit. Everyone else either relied on these established players or watched from the sidelines.

That's changing fast.

Right now, a quiet revolution is happening. Dozens of countries are pouring billions into homegrown rocket programs. They're not doing it because they think they can beat Space X. They're doing it because they've realized something crucial: whoever controls your launch capability controls your national security.

The Trump administration's unpredictability, rising tensions with China, and strategic competition over satellite networks have accelerated this shift dramatically. When your government satellites depend on a foreign company's goodwill, you're vulnerable. When that company is run by someone the government has leverage over, you're even more exposed.

This isn't theoretical anymore. Germany just announced $41 billion in space spending over five years, with hundreds of millions earmarked specifically for domestic launch startups. Australia is building its first spaceport. Canada is funding its own rocket programs. Spain, Italy, France, and the UK are all betting serious money that they need independent access to space.

But here's what most people miss: talking about building rockets and actually building rockets are completely different things. Several countries have made big announcements. Far fewer have backed them up with real funding. Even fewer have hardware close to orbit.

Let's separate the serious players from the ones still dreaming.

TL; DR

- Germany leads Europe's push: Investing over $41 billion in space, with three well-funded startup rockets (Isar Aerospace, Rocket Factory Augsburg, Hy Impulse) racing toward their first orbital flights.

- Sovereign launch is now security policy: Nations see independent rocket access as essential to national defense, not just a nice-to-have capability.

- Private startups are doing the heavy lifting: Unlike the Space Race era, governments are funding commercial companies rather than building rockets themselves.

- Geopolitics is the real driver: Trump's relationship with Elon Musk and threats to NATO have pushed European allies to invest in independence from US launch providers.

- Most countries are still talking, not building: Only a handful have committed serious, sustained funding. Many announced programs remain underfunded or stalled.

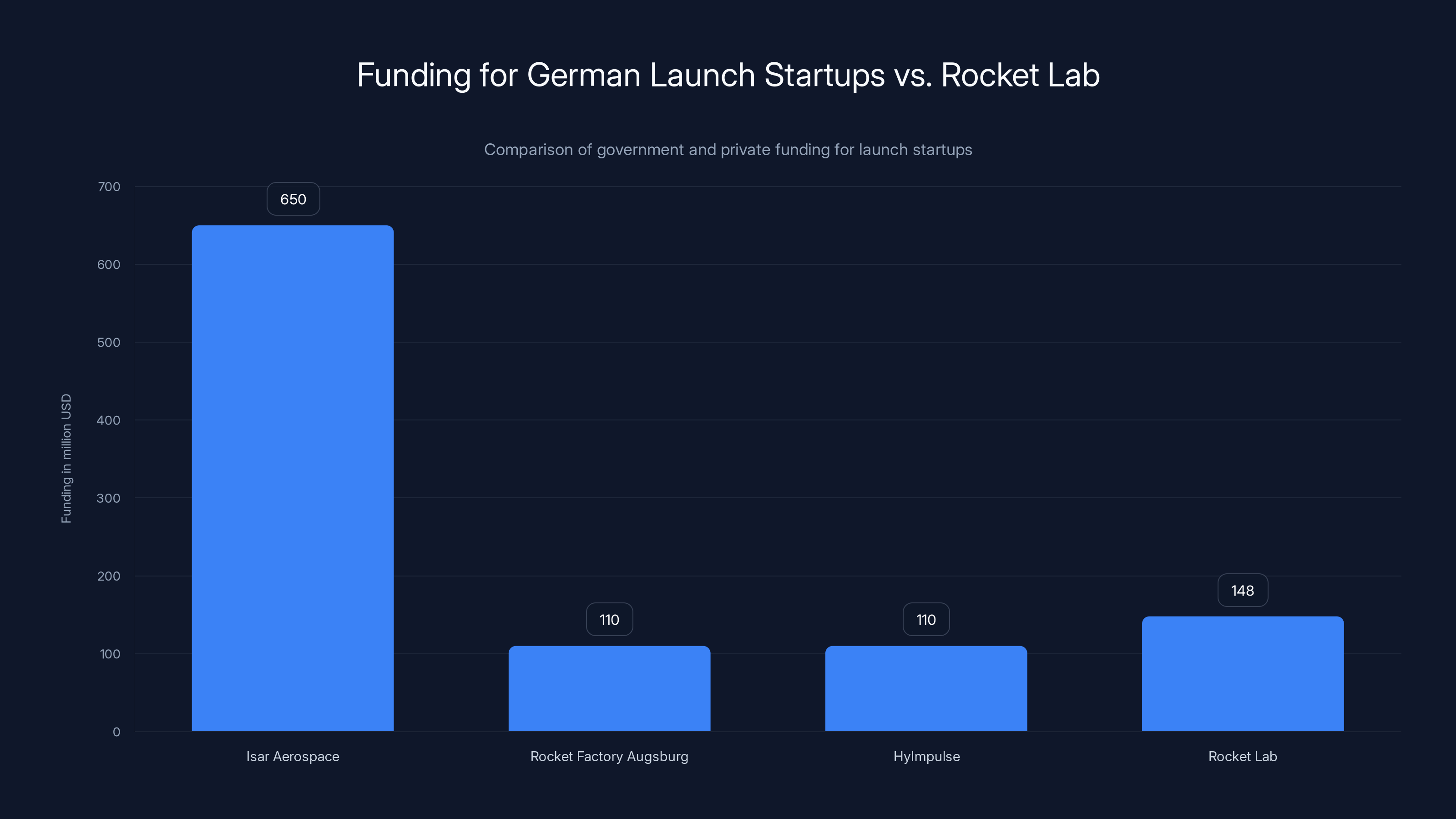

Isar Aerospace leads with $650 million in private funding, while Germany's government funding for startups like RFA and HyImpulse shows a strong commitment to launch independence.

Why Sovereign Launch Matters Now More Than Ever

For most of the space age, launch access wasn't really a concern for developed nations. You could pay the Americans, Russians, or Europeans for a ride. Prices were high, but capacity existed. If you needed satellites in orbit, you had options.

That ecosystem has fractured.

Space X's dominance has actually created new vulnerabilities for some countries. When one company controls roughly 70% of global launch capacity, and that company's CEO has direct influence with the sitting US president, smaller nations start getting nervous. What happens if they don't align with current US policy? What if relations sour? What if there's a sanctions regime, a trade war, or diplomatic tensions?

These aren't paranoid questions anymore. They're strategic planning.

Satellite networks themselves have become critical infrastructure in ways they weren't ten years ago. Modern militaries depend on satellite communications, reconnaissance, and navigation. Economic systems depend on satellite-based GPS and financial networks. Infrastructure increasingly depends on remote sensing and disaster response capabilities via satellites.

If another country controls whether your satellites reach orbit, that country has a veto over your national security and economic resilience.

This realization has cascaded through NATO and the G7 faster than any policy document could move it. When Germany's defense minister publicly stated that satellite networks are "an Achilles heel of modern societies" and that "whoever attacks them paralyzes entire nations," he was articulating something that intelligence agencies had already concluded privately. The public acknowledgment changed the political calculation.

Suddenly, spending billions on domestic rocket programs looked not like expensive vanity projects but like essential infrastructure investment. The same way you don't want to depend entirely on one power for energy, food, or military supply chains, you can't afford to depend entirely on one company for space access.

The geopolitical context has amplified this urgency dramatically. China is advancing its military space capabilities at a breakneck pace. Russia, despite sanctions, continues developing antisatellite weapons and space-based capabilities. The US under Trump has made it clear that European defense spending on "American" technologies can't be taken for granted.

When European leaders heard Trump suggest that NATO wasn't guaranteed to defend them if they didn't spend enough, and when they watched him impose tariffs and threaten invasions of allied territory, the message sank in: you can't outsource your security to Washington indefinitely. You need backup options.

For space access, that means building your own rockets.

Germany's Ambitious Bet on Launch Independence

Germany is probably the most serious about this right now. The numbers prove it.

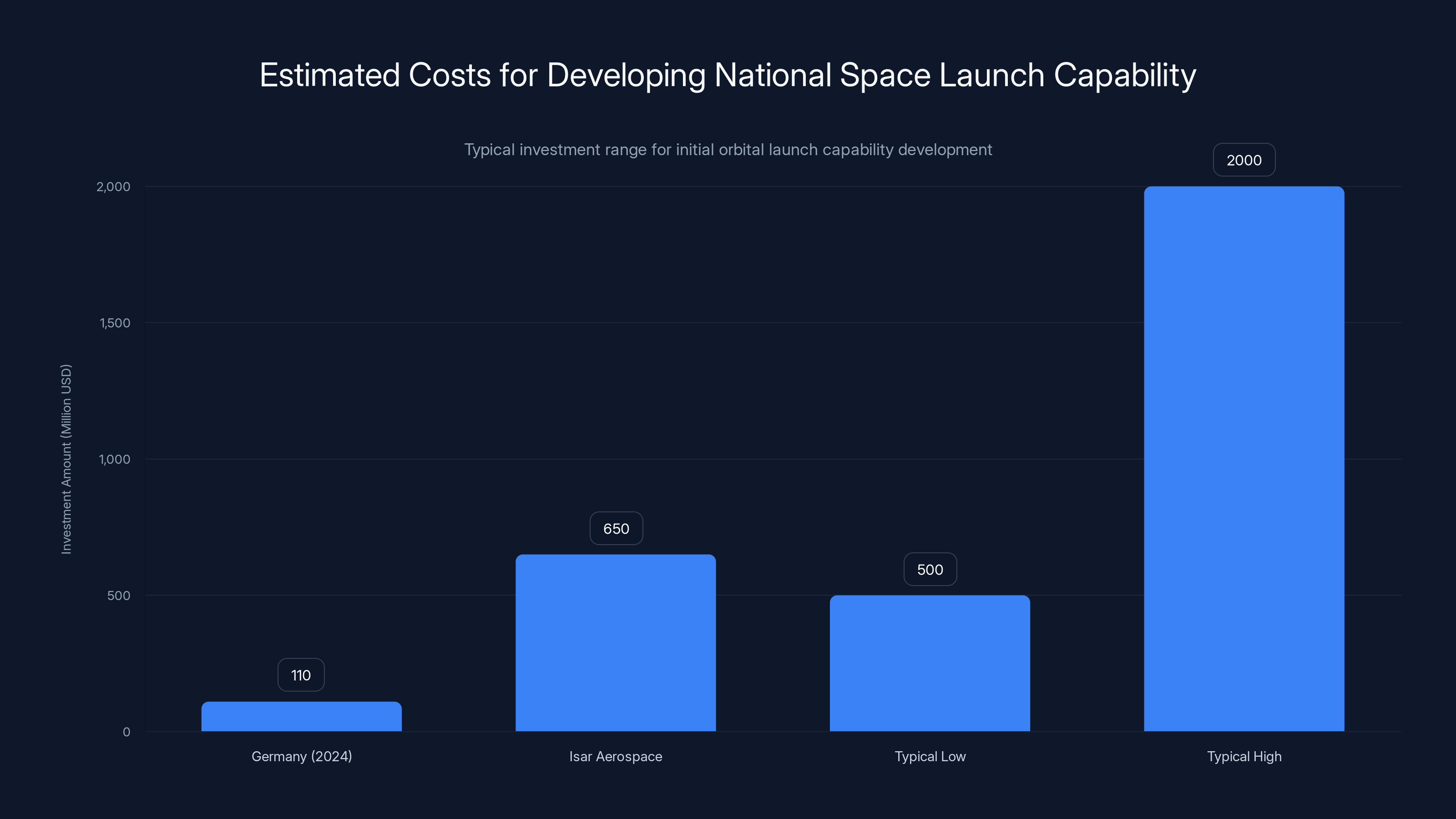

In 2024, the German federal government committed over

Context matters here. For comparison, Rocket Lab, the world's most successful commercial launch startup not founded by a billionaire, raised approximately $148 million in private funding before reaching orbit in 2018. Nearly all of it came from investors, not government. The fact that Germany is now putting comparable amounts directly into multiple startups shows how seriously they're taking this.

Isar Aerospace: Europe's Most Funded Launch Startup

Isar is the furthest along. The company has raised roughly $650 million in private funding, making it Europe's best-capitalized launch venture. They built the Spectrum rocket, a two-stage liquid-fueled vehicle designed to carry small payloads to low Earth orbit.

In 2025, Isar attempted its first orbital flight from a spaceport in northern Norway. The rocket lifted off cleanly but experienced an issue during the first stage flight. It didn't reach orbit, but the attempt itself was instructive. The vehicle performed many aspects of the flight profile correctly. Failure in rocket development isn't a dead end; it's a data point.

Isar is already preparing the second Spectrum rocket for another test flight. Industry observers expect this attempt could come within months. Success wouldn't mean the company is "done"—commercial rocket development requires multiple successful flights to prove reliability and attract customers. But reaching orbit for the first time is the critical inflection point. Once you do it once, you can do it again. That's when investors, governments, and satellite operators start taking you seriously.

The company's stated goal is to offer regular launch services by 2026 or 2027. That timeline might slip—timelines always slip in rocket development—but Isar's combination of technical progress, funding depth, and government backing makes them the likeliest German candidate to deliver sovereign launch capability.

Rocket Factory Augsburg: The Established Player

RFA has taken a different approach. Rather than building an entirely new vehicle, they're developing engine technology and competing in a slightly different launch category. Their focus is on methane-based propulsion, which offers advantages over traditional solid rockets in terms of cost and reusability.

The company is further behind Isar in terms of orbital attempts, but they bring different strengths. RFA has deeper ties to existing aerospace supply chains in Germany, which could accelerate manufacturing and certification once the rocket design is finalized.

Hy Impulse: The Long-Shot With Big Potential

Hy Impulse is pursuing what many consider a riskier approach: hybrid rocket engines that use solid fuel with liquid oxidizer. The technology offers potential advantages in simplicity and cost, but it's less proven than either liquid or solid-fuel systems.

They're further behind their competitors, but the technical approach could leapfrog conventional wisdom if executed well. German space policy is explicitly hedging bets across these three very different approaches. If one fails, the others continue. If one succeeds, Germany has options for future evolution.

What makes this remarkable is the coordination. Germany isn't just throwing money at startups and hoping. The government has explicitly stated its goal: "sufficient responsive launch transport capacity to ensure national and European strategic independence in all payload classes and transport scenarios."

This isn't ambiguous. Germany wants to launch small satellites, medium payloads, and eventually larger missions without depending on anyone else. They want to do it on German territory or friendly allied territory. And they're willing to fund multiple parallel efforts to make it happen.

That's serious industrial policy for space.

Developing a national space launch capability can cost from

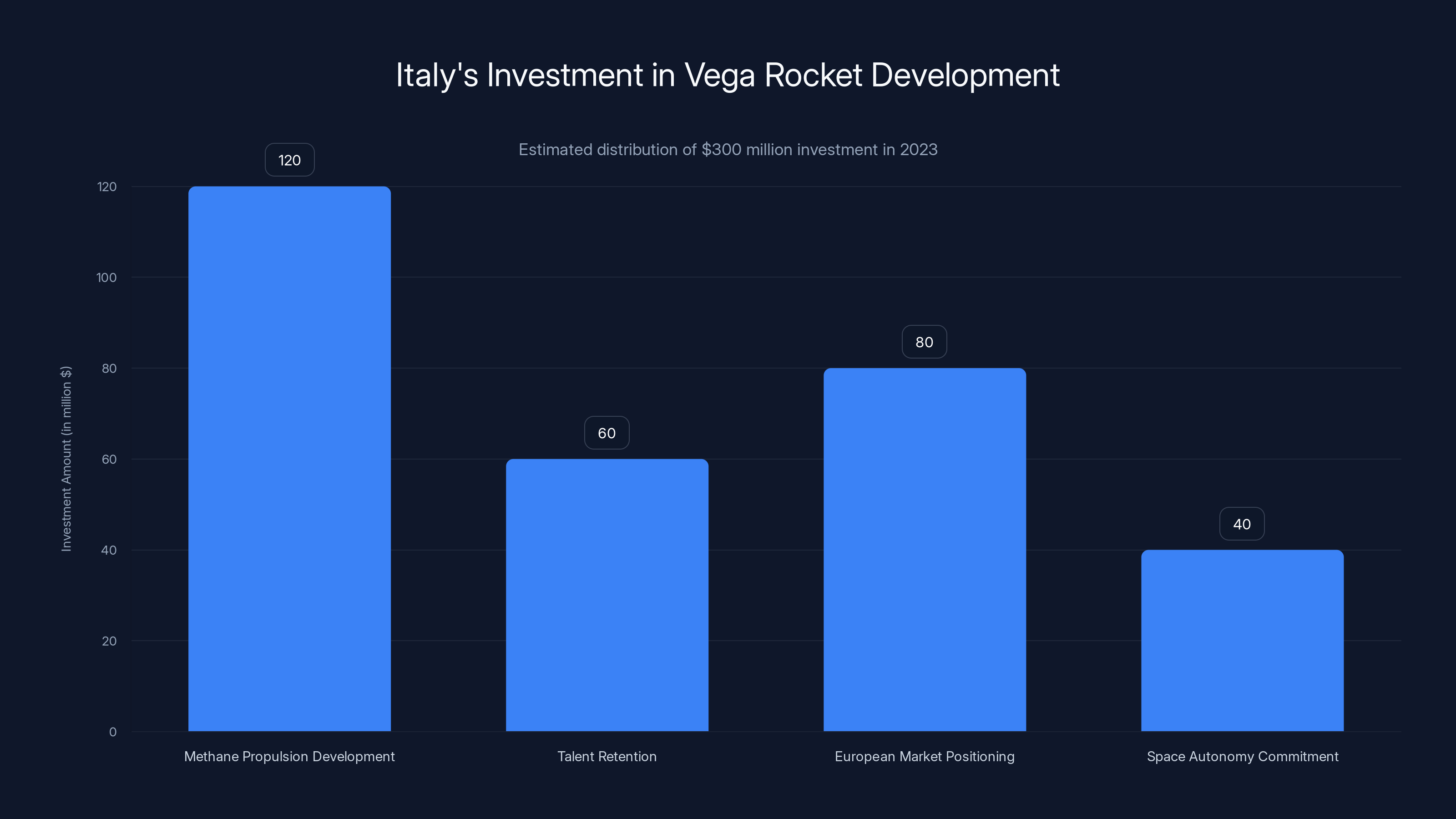

Italy and the Vega Rocket: Extending Existing Capability

Italy took a different strategic approach. Rather than starting from scratch, they're enhancing existing capability.

Italy already has the Vega rocket, built primarily with Italian and European components, operated by Avio. For years, Vega has been the European option for small satellite launches, offering a more economical alternative to the larger Ariane rocket for certain missions.

Vega isn't Italian-made in the sense that it's fully domestic. It's a European program with significant Italian participation and manufacturing. But from a strategic standpoint, Italy has meaningful control over it and a major industrial stake in its success.

In 2023, the Italian government committed over $300 million to support Avio's development of advanced versions of the Vega rocket, particularly versions with methane propulsion. This funding does several things simultaneously.

First, it keeps Italian industry at the cutting edge of space launch technology. The engineers, manufacturers, and supply chain involved in Vega development stay current and employed. That matters for retaining technical talent and industrial capacity.

Second, it positions Italy to benefit from the European space market. As other European countries seek independent launch capability, they'll need rockets. If Italy can offer them through Avio, that's both revenue and influence.

Third, it demonstrates commitment to European space autonomy without requiring Italy to independently develop a completely new vehicle. They're working within the existing European framework while investing in the next generation.

Ario's methane-powered Vega variants could become a workhorse for European missions in the next decade. Methane engines offer several advantages: they're cheaper to operate than current solid rocket motors, they can potentially be reused with proper design, and they scale well from small to large vehicles.

For a country like Italy, backing Avio and Vega is a pragmatic choice. They get the prestige and capability of sovereign launch without the astronomical cost of developing something entirely new.

France and the European Dimension

France occupies an interesting position. It has Ariane, the pan-European heavy-lift rocket, which France leads and manufactures in large part. Ariane 6 recently achieved successful orbital flights after years of delays, finally ending Europe's reliance on Space X for some critical missions.

For pan-European programs managed by the European Space Agency and European Union, Ariane 6's maturation is crucial. These institutional missions will use Ariane when possible. That keeps France's aerospace industry busy and Europe's space agency independent.

But France is also investing in smaller domestic startups as insurance against future Ariane issues and to ensure France has independent options for French national satellites.

The logic is sound: Ariane 6 is expensive for small satellite launches. If a French military or civilian satellite needs to reach orbit urgently and Ariane isn't available, having a smaller, cheaper French or French-backed option provides flexibility. France is funding companies like Axiom Space and others who might eventually provide that capability.

France also benefits politically from European unity on space. If France positions itself as the leader protecting European space interests against American and Chinese dominance, that enhances France's diplomatic influence within Europe. Space is increasingly part of the national power calculation.

The United Kingdom's Rebirth as a Launch Nation

The UK presents a fascinating case of history repeating itself.

Britain was actually an early space power. The UK developed the Black Arrow satellite launch vehicle in the 1960s and 1970s, becoming only the sixth country to independently launch a satellite. Then, in 1971, the government canceled the program to save money. Britain walked away from launch capability and never looked back.

For fifty years, the UK depended on other nations for space access. They were satisfied with that arrangement. The European framework worked well enough.

Now they're trying to get it back.

The UK government has committed funding to several promising small-satellite launch startups. Axiom Space, based in the UK, is developing engines and launch vehicles. The government is supporting infrastructure development, including plans for spaceports at existing RAF bases and new facilities.

What's interesting about the UK approach is that they're being realistic about their place in the market. Britain isn't trying to out-compete Space X or build massive heavy-lift rockets. They're focusing on small-payload launch, which is actually where the market has moved. Hundreds of small satellites need to reach orbit every year. That's where the commercial opportunity is.

The UK also benefits from its relationship with the European space framework while maintaining independence. It's leveraging both institutional space infrastructure developed in Europe and developing new sovereign capabilities.

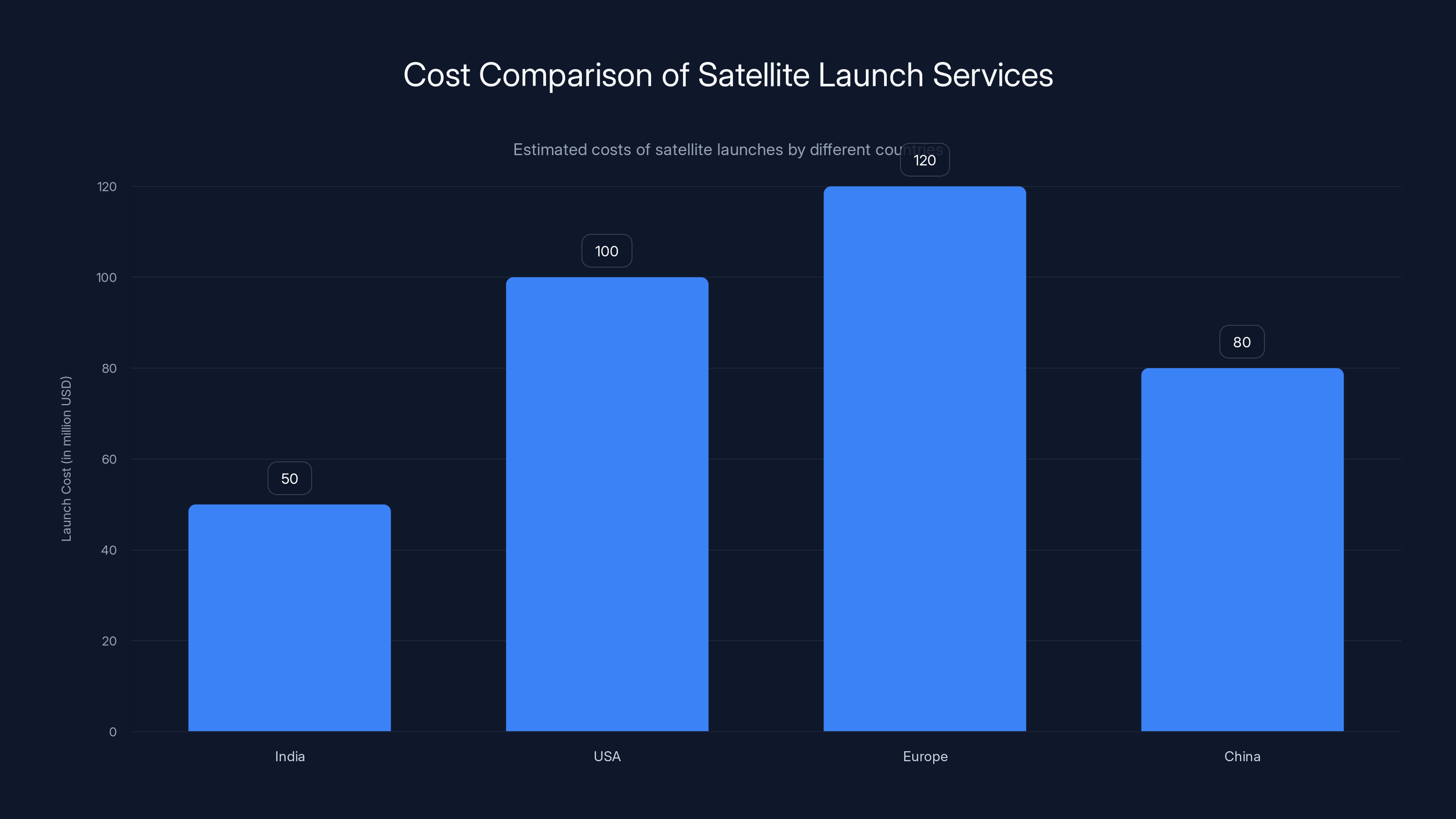

Estimated data shows Italy's strategic $300 million investment in Vega rocket development, focusing on methane propulsion and market positioning.

Spain's Emerging Launch Ambitions

Spain has been less visible in the sovereign launch push, but they're investing nonetheless.

The Spanish government has committed funding to domestic space companies and is supporting PLD Space, a startup working on small launch vehicles. Spain is also positioning itself as a location for spaceport infrastructure, understanding that actual launch facilities are as important as the rockets themselves.

Spain's approach is less prominent than Germany's but still substantive. They're spreading risk across several initiatives rather than betting everything on one champion company. This hedge strategy makes sense for a mid-tier space power.

Like other European nations, Spain sees the geopolitical logic clearly. If European nations need sovereign launch capability and are willing to fund it, Spain wants to participate in the market and benefit from the industrial development.

Canada's Measured Approach

Canada is in a unique position. It's tightly integrated with the US military-industrial complex through NATO and NORAD, yet it sees the same independence imperative everyone else does.

Canada has a strong aerospace industry centered around satellite and spacecraft manufacture. They've produced some of the world's best robotic systems and satellites. But they've never had indigenous rocket launch capability.

The Canadian government is now funding domestic launch startups and has committed to developing spaceport infrastructure. They're taking a measured but serious approach.

What's distinct about Canada is that they have room to cooperate closely with the US while building independent capability. Unlike European nations that may feel they need to distance themselves from American control, Canada can work with the US on many space activities while still developing sovereign options for national security satellites.

Canada's space strategy explicitly mentions the importance of "assured access to space," which is diplomatic language for "we can't depend entirely on others." The funding levels are more modest than Germany's, but the direction is clear.

Australia's Southern Hemisphere Advantage

Australia is undertaking an unusual effort: building a completely new spaceport capability from scratch.

The Australian government has funded the development of two spaceport complexes. The geographic location is valuable. A spaceport at lower latitudes offers advantages for reaching certain orbits. Australia's position makes it useful for accessing polar and high-inclination orbits that are critical for Earth observation and some military satellite missions.

Australia is also backing domestic launch startups. They're thinking strategically about what role Australian launch capability can play in regional space markets. Southeast Asian nations need satellite access. An Australian launch provider could service that market.

The Australian approach is interesting because it's less about complete independence from allies and more about positioning Australia as a regional space hub. They want to be the country where satellites from their region launch, which gives them economic and diplomatic benefit.

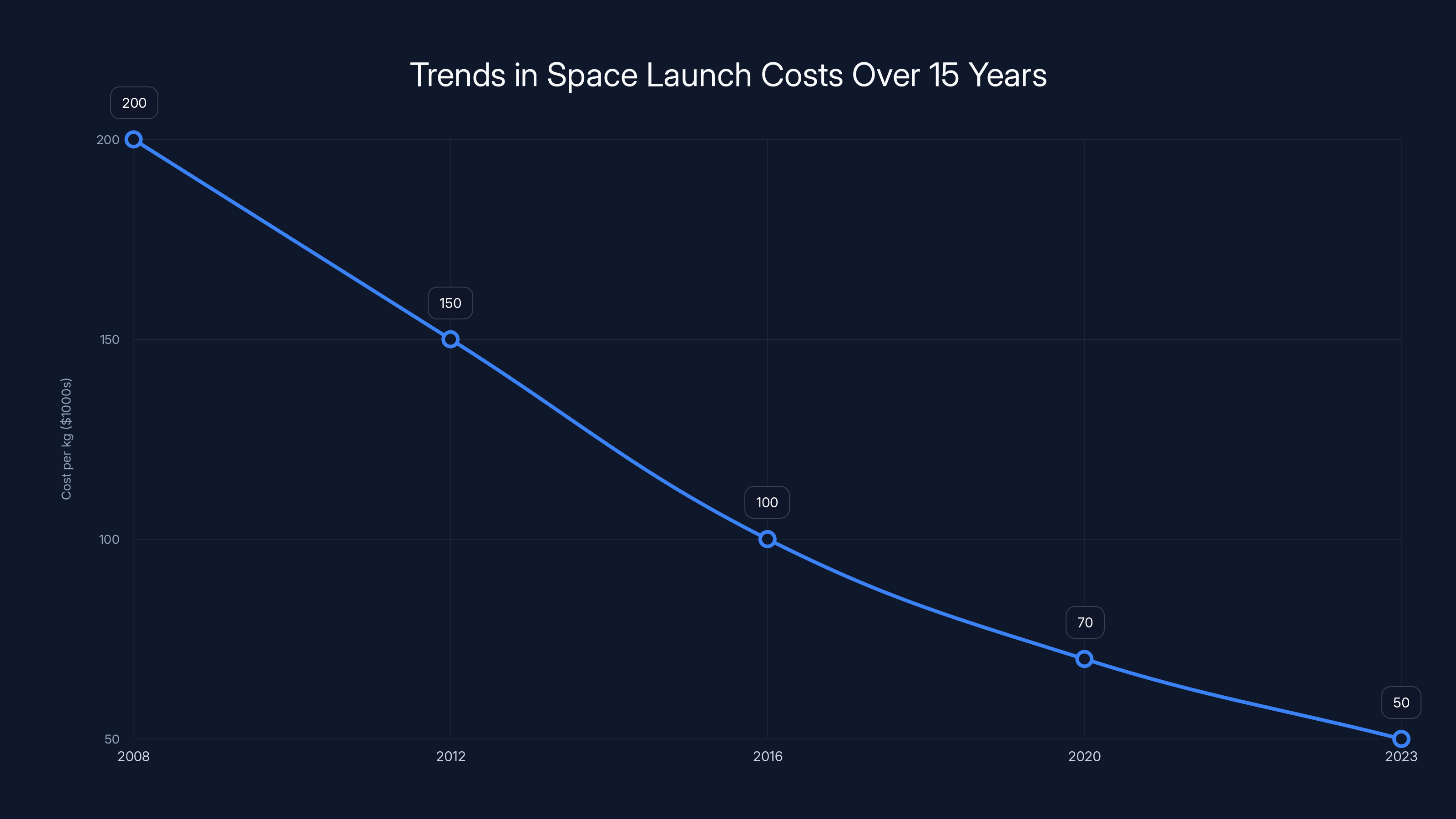

The introduction of reusable rockets and small launch vehicles has significantly reduced space launch costs over the past 15 years. (Estimated data)

Japan and Established Capability Evolution

Japan already has independent launch capability through its H-IIA and H-III rockets, built by Mitsubishi Heavy Industries. They've successfully launched satellites for decades.

What's changed is Japan's investment in next-generation capability. The H-3 rocket represents a major advance in cost efficiency. Japan is also funding commercial startup ventures and positioning itself as a provider in Asia-Pacific markets.

Japan's situation differs from European nations pursuing first sovereign launch. Japan is enhancing and modernizing existing capability while also ensuring competition and innovation through startup funding. This is evolution, not revolution.

The geopolitical context still matters. Japan faces Chinese military pressure and wants assured access to space for defense purposes. Investing in domestic launch capacity, especially more cost-effective versions, is part of Japan's long-term defense posture.

India's Accelerating Space Program

India already demonstrated independent launch capability decades ago. They've successfully launched satellites and deep space probes using indigenous rockets. The Indian Space Research Organisation (ISRO) runs one of the world's most capable space programs.

What's happening now is acceleration and commercialization. India is privatizing certain aspects of space launch and encouraging commercial startups to develop launch vehicles. Skyroot Aerospace, backed by private funding, is developing the Vikram small-launch rocket.

India is also becoming competitive on cost. Indian launch services are significantly cheaper than Western alternatives for comparable capability, which makes India a serious player in the global commercial launch market.

From a geopolitical perspective, India's space independence is important to their strategic autonomy in Asia. As China advances militarily, India sees space capabilities as essential to national defense. Continuing to develop and improve launch capability fits squarely into India's broader strategic vision.

Middle Eastern and Asian Aspirations

Several countries in the Middle East and Asia have ambitions but limited demonstrated capability.

Saudi Arabia has discussed building domestic launch capability as part of its Vision 2030 modernization agenda. The Emirates have invested in space infrastructure and satellite manufacturing. These efforts are real, but they're typically relying on partnerships with established space powers rather than developing entirely indigenous systems.

These countries are pursuing space capability as part of broader modernization and economic diversification. They're positioning themselves as space hubs and technology centers. Whether they develop actual independent launch capability remains to be seen, but they're definitely trying to enhance their role in the space economy.

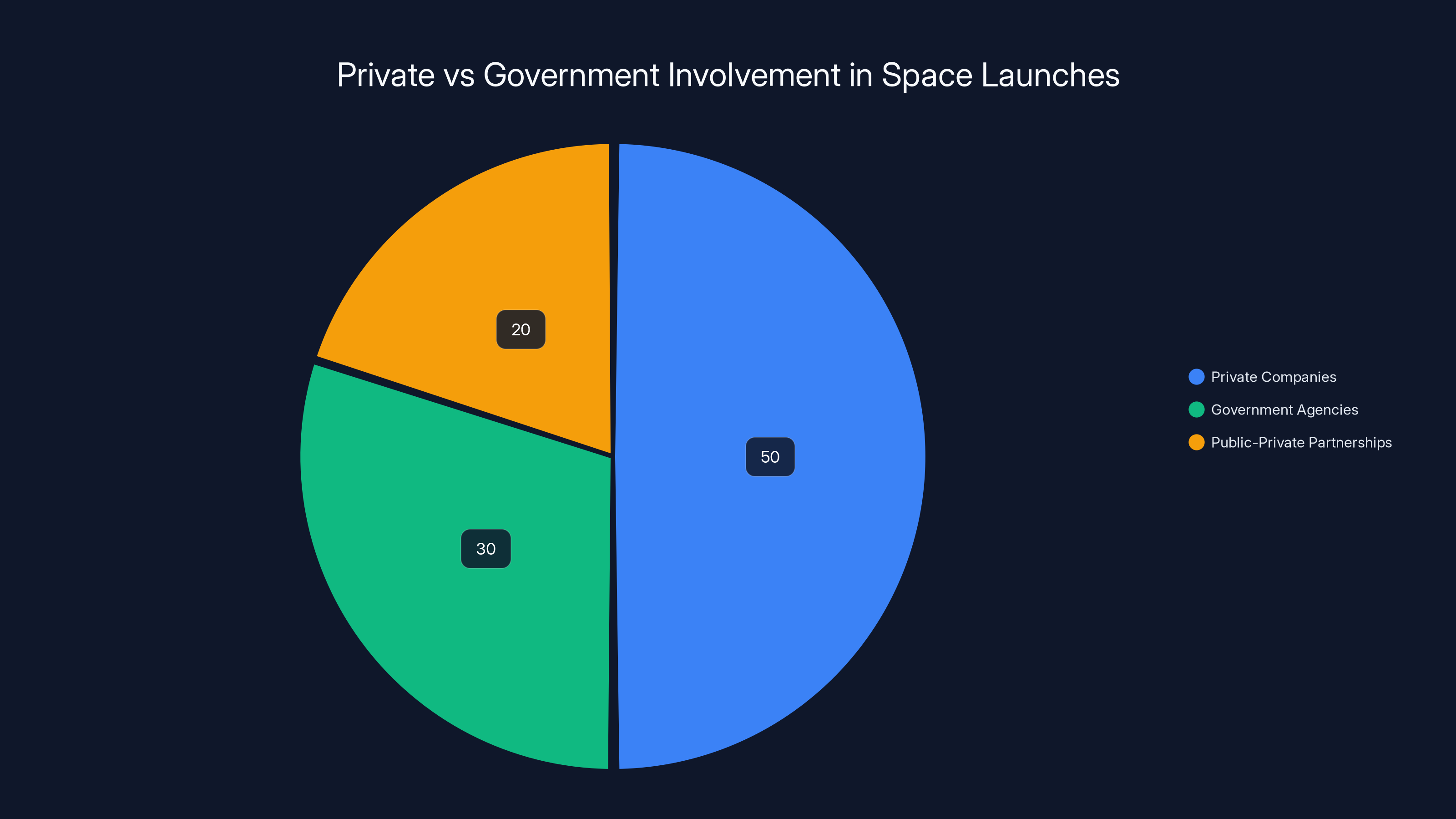

Private companies now play a crucial role in space launches, accounting for an estimated 50% of the involvement, highlighting a shift from traditional government-led initiatives. Estimated data.

The Challenge of Actually Reaching Orbit

Here's what separates the serious efforts from the wishful thinking: actual hardware approaching operational status.

Germany has rockets undergoing test flights. That's real progress. Isar's Spectrum vehicle has launched, though it didn't reach orbit on the first attempt. The fact that they flew at all puts them in an extremely small group.

Italy has an operational rocket already in service with Vega. They're enhancing it, but they have proven capacity.

Many other nations have announced programs, committed funding, or backed startups. Some of these will fail. Rocket development is extraordinarily difficult and capital-intensive. The startup mortality rate is high. Most companies that try to build rockets fail.

What's different now is that enough nations are spreading their bets across multiple companies and substantial funding that even with a high failure rate, some will succeed. Germany funding three separate companies is a smart hedge. If all three fail, Germany failed. If even one succeeds, Germany has achieved its objective.

For investors and engineers, this is golden. The space launch industry, which was essentially closed to new entrants for decades, now has more funding and more serious government backing than at any time since the 1970s. That's attracting world-class talent and supporting innovation.

The Role of European Cooperation

One pattern worth noting: most European countries are pursuing sovereign capability while also participating in European institutional programs like ESA and Ariane.

This isn't contradictory. It's strategic layering. Nations want European capability for shared missions, but they also want national options for national security satellites. They want to be customers for commercial European launch services, but they also want to own the capability themselves.

This approach provides resilience. If one system fails, others exist. If one is unavailable due to politics or logistics, alternatives are available. That redundancy is the whole point.

Europe is learning from its experience with American launch dependency. For years, European nations were comfortable using Space X for critical missions while waiting for Ariane 6. Now they're asking: what if that wasn't an option? What if US policy changed? What if geopolitical relations soured?

The answer is: you need backup options. That realization is driving the entire European push toward distributed launch capability.

Economics and Market Dynamics

The economics of space launch have shifted dramatically in the last fifteen years, and that's enabling this diversification.

Space X proved that rockets could be reused and that launch costs could drop dramatically from historical levels. That changed the fundamental equation. Launch isn't necessarily a one-time, incredibly expensive infrastructure program anymore. It can be an ongoing service.

That makes it more feasible for mid-tier nations to develop independent launch capability. They don't need to build a single enormous program. They can support multiple smaller companies, accept some will fail, and end up with reliable service.

Small launch vehicles are also genuinely useful now. Historically, if you had a satellite, you needed a big rocket. Now, small satellites are valuable. Remote sensing data, communication relay, internet service (like Starlink), and scientific instruments all fly on small spacecraft that don't need massive launch vehicles.

This opens a market niche that didn't exist at a viable scale before. Companies like Rocket Lab have proved that small-launch is a real business. That success has inspired dozens of competitors, including the German startups, British ventures, and others.

Commercial launch companies also reduce the burden on governments. Instead of governments building and operating rockets themselves, they can fund private companies. The companies take the entrepreneurial risk. Governments get a rocket without maintaining a massive in-house infrastructure.

India offers significantly cheaper satellite launch services compared to Western countries, enhancing its competitiveness in the global market. (Estimated data)

National Security Calculus

Underneath all of this is a fundamental shift in how nations think about security.

Traditional military security involved armies, navies, and air forces. Space was important but peripheral. Now, space is central. Military operations depend on satellite communications and positioning. Economic systems depend on GPS and financial networks reliant on satellite infrastructure. Civilian infrastructure depends on weather satellites and early warning systems.

If another nation controls your access to space, they have leverage over all of these critical systems. That's an unacceptable position for any self-respecting government.

The Trump administration's unpredictability has accelerated this realization dramatically. When European leaders genuinely worried about whether the US would defend them, they also started worrying about whether the US would help them reach space. That worry translates into political willingness to fund alternatives.

China's military modernization in space also matters. China has developed antisatellite weapons, space-based surveillance systems, and military launch capability. The prospect of competition or conflict with China in space makes nations want their own capabilities.

For India, competition with Pakistan and China justifies space investment. For European nations, it's more about strategic independence from both the US and China. For everyone, the message is the same: you need the capability to reach space on your own terms.

The Private Sector's Crucial Role

What's interesting about the current wave of sovereign launch development is how much it depends on private companies rather than government-run space agencies.

Historically, space launch was a government function. NASA, Soviet space program, ESA—all government organizations building and operating rockets. Now, governments are funding private startups.

This model has major advantages. Private companies can move faster, iterate quicker, and take risks that government bureaucracies can't. They can hire talented engineers from around the world without political complications. They can fail and try something different without major political consequences.

Governments provide capital and demand, but they let entrepreneurs run the operation. That's proven wildly effective in the US market with Space X and Rocket Lab. Now it's being applied in Europe, Asia, and elsewhere.

The risk, from a national perspective, is that you're betting on companies that might not survive or might be acquired by foreign entities. But governments are hedging this by funding multiple companies and maintaining some technical capacity in-house through their space agencies.

Timelines and Realistic Expectations

When should these new sovereign launch capabilities be operational?

Germany's official targets suggest 2026 or 2027 for initial operational capability from Isar or another competitor. Those timelines are likely optimistic. Rocket development almost always slips. The history of space launch is filled with delays.

But even if timelines slip to 2028 or 2029, that's still imminent from a geopolitical perspective. These capabilities are coming within the decade. By 2030, expect multiple new nations to have independent launch capability, or at least reliable access through commercial providers they partially control.

Once a few nations pull it off, others will accelerate their own programs. There's a threshold effect. When it becomes clear that sovereign launch is achievable for developed nations with adequate funding, it becomes politically difficult to not pursue it.

The Future of Space Launch

What does this trend mean for the global space economy and international relations?

First, Space X's dominance will likely moderate. Not disappear, but moderate. Space X will continue as the leading global launch provider for customers choosing purely on commercial terms. But the market for "captive" customers—governments launching national security satellites—will become distributed.

Second, launch services will become more expensive on average. Space X benefits from economies of scale and Elon Musk's willingness to operate at lower margins. National champions and smaller competitors will have higher costs. That's fine for government missions, which have less price sensitivity. But it means the era of extremely cheap commercial launch might not expand as fast as some predicted.

Third, international cooperation on space will likely decrease in some areas while increasing in others. Shared scientific missions might see more cooperation. National security missions will see less, as each nation tries to develop independent capability. You'll see both trends simultaneously.

Fourth, the space launch industry will become more fragmented globally. Rather than one or two providers dominating, there will be a tier of established providers (Space X, Ariane, Russian rockets where available) and an emerging tier of national champions and regional providers. That fragmentation has downsides for efficiency but upsides for resilience.

Finally, space is becoming explicitly militarized in strategic planning. Nations aren't pursuing launch capability purely for science or commerce. They're pursuing it because they see space as a domain where military competition will occur. That mindset shapes all the decisions around funding, partnerships, and technology choices.

Conclusion

The space launch industry is undergoing the most significant transformation in its history. For decades, it was a superpower domain. Then it was dominated by Space X. Now it's becoming globalized, with dozens of nations investing in their own capability.

This shift didn't happen because nations suddenly got interested in space exploration. It happened because space became essential to national security and economic resilience. When your military can't function without satellites, when your economy depends on GPS, when another nation can deny you space access, you have to own the capability yourself.

Germany is the model here. They've analyzed the problem, committed serious funding, and backed multiple companies racing toward the goal. They're accepting failure as a possibility but betting that at least one will succeed. That's a rational approach to high-risk, high-reward technology development.

Other nations are following similar paths. Some will succeed faster than others. Some will ultimately decide the cost isn't worth the benefit and step back. But the overall trajectory is clear: space launch is becoming distributed. The era of depending on one or two providers is ending.

That has profound implications for international relations, military strategy, and the commercial space economy. We're in the early stages of a transition that will reshape how the world thinks about space access for the next fifty years.

The rockets being built in German factories and northern Norwegian test ranges represent more than engineering achievements. They represent nations asserting control over their own futures in an era where space access is national security. That's the real story behind the push for sovereign launch capability.

FAQ

Why do countries need independent space launch capability?

Independent launch capability provides national security assurance by eliminating reliance on foreign providers for critical satellite missions. Military and government satellites require sovereign access to space to prevent adversaries or allies from weaponizing dependency. Additionally, as satellite networks become essential infrastructure for communications, navigation, and early warning systems, nations want control over their own access rather than trusting it to another country's private company or government.

How much does it cost to develop a national space launch capability?

Developing an initial orbital launch capability typically requires

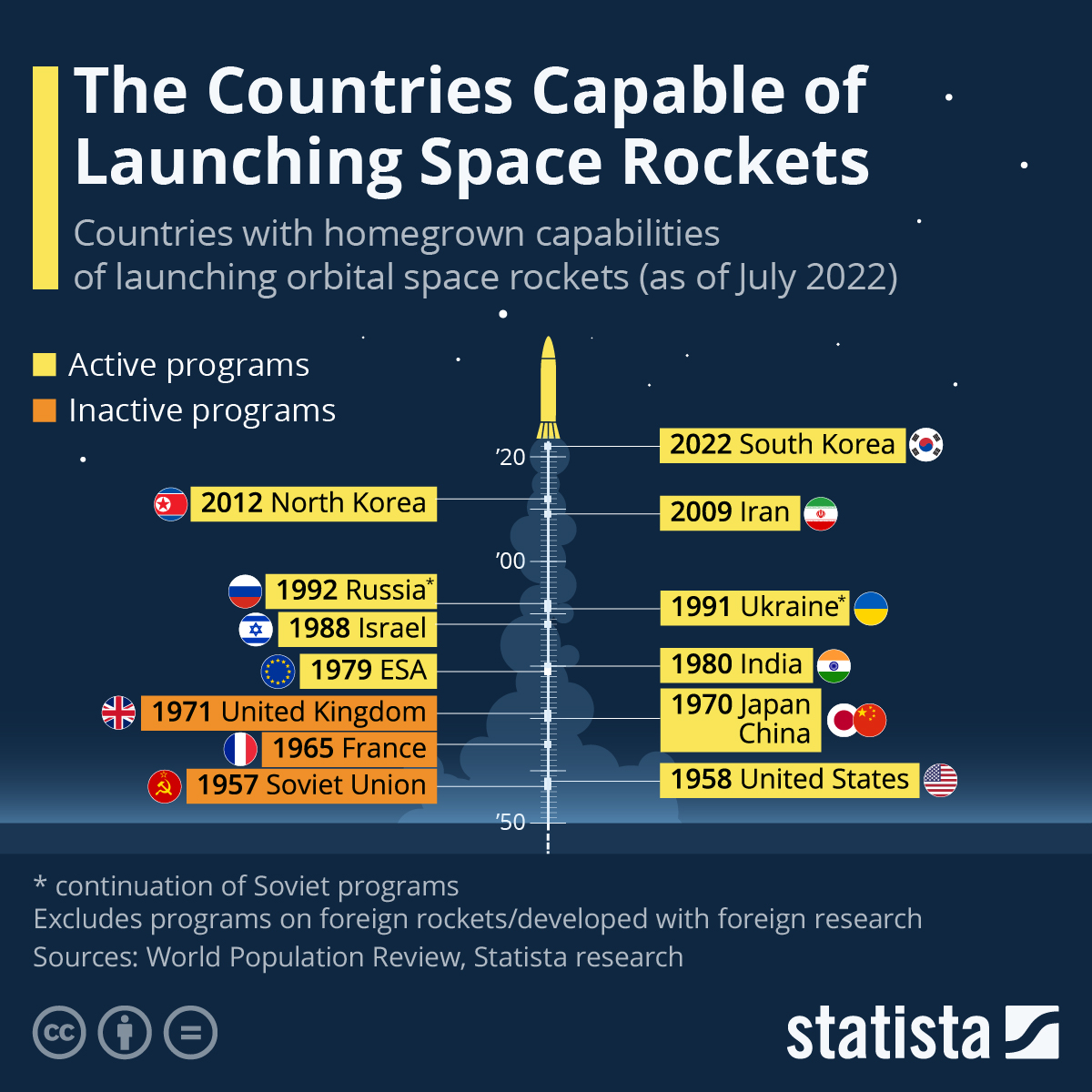

Which countries have already achieved sovereign space launch capability?

Twelve nations have successfully launched satellites into orbit using their own rockets: the United States, Russia, China, France, Japan, India, the United Kingdom, Israel, Iran, North Korea, South Korea, and New Zealand. However, the UK no longer maintains active launch capability, though they're attempting to restore it. Most other developed nations historically relied on these established providers or multinational programs like Ariane.

How does geopolitics influence space launch development?

Geopolitical tensions directly drive launch capability development. European nations accelerated their programs after the Trump administration questioned NATO commitments and threatened tariffs on allies. China's military space development prompted India and regional powers to pursue independence. Space X's leadership position under Elon Musk, who has significant government influence, created political motivation for other nations to reduce dependency. These strategic calculations override pure economics—nations will fund expensive redundant capability rather than accept strategic vulnerability.

What's the difference between national space agencies and commercial launch startups?

National space agencies traditionally designed, built, and operated rockets as government organizations, moving slowly through bureaucratic processes. Commercial startups operate more like businesses, moving faster and taking more risks. Modern governments fund commercial startups rather than building rockets themselves, outsourcing entrepreneurial risk while maintaining control through purchasing agreements. Private companies like Isar Aerospace bring innovation and cost efficiency that traditional government programs struggle to achieve.

How long before new nations achieve orbital spaceflight capability?

Germany's most advanced startups, particularly Isar Aerospace, could achieve their first orbital flights in 2025 or 2026, though timelines typically slip in rocket development. Most other programs are two to five years behind. Realistic timelines suggest multiple new nations will have independent or semi-independent launch capability by 2030. Some programs may accelerate if early successes prove the concept viable. Others may abandon efforts if technical or financial obstacles prove insurmountable.

Are these national launch programs economically viable as commercial businesses?

Most national champion rockets will struggle to compete with Space X on price for commercial customers seeking pure cost efficiency. However, they're not primarily designed for commercial competition. They're designed to launch government satellites and provide sovereignty. The commercial market provides revenue and efficiency incentives, but the core business case is national security. A startup might launch government satellites at high margin and commercial satellites at low margin, subsidizing the national security mission through commercial revenue.

How does the Ariane rocket fit into European sovereign capability?

Ariane 6, the current version, represents European capability developed collectively by multiple nations and managed by ESA. While not any single nation's "sovereign" system, it serves the purpose of not depending on American or Chinese launch providers. Individual nations are developing smaller systems for their own national security missions, while supporting Ariane for shared European institutional missions. This layered approach provides both collective European independence and national-level backup options.

Actionable Insights and Key Takeaways

For policymakers, the key insight is that space launch is no longer a luxury. Nations without reliable access to their own satellites face strategic vulnerability. The investment required is substantial but manageable, and the window to develop capability is narrowing as technology becomes more complex.

For investors, multiple pathways exist to profit from this trend. Funding ventures in nations pursuing launch independence could yield returns if companies succeed. Supply chain companies selling components to launch startups have lower-risk revenue opportunities. Established aerospace companies can position themselves as prime contractors and technology partners.

For engineers and technologists, this represents an extraordinary opportunity. Space launch has been relatively closed for decades. Now, dozens of ambitious projects are hiring and building. The talent available in the space industry is world-class, and the problems are genuinely difficult and interesting.

The push for sovereign space launch capability represents a historic reordering of how nations think about space access. Understanding this shift—and who's serious about pursuing it—is essential for anyone tracking geopolitics, economics, or technology.

Key Takeaways

- Germany leads Europe with $41 billion in space spending and three well-funded launch startups (Isar, RFA, HyImpulse) approaching first orbital flights in 2025-2026

- Geopolitical tension with Trump administration and uncertainty about SpaceX dependency motivated NATO allies to pursue sovereign launch capability

- Only 12 nations have achieved independent spaceflight capability; new powers are emerging but success requires sustained government funding and technical expertise

- Small-launch vehicles create viable market niche that makes independent capability economically feasible for developed nations, unlike previous heavy-lift era

- European nations are layering sovereign national launch capability with collective European Ariane program, providing strategic redundancy

Related Articles

- Ariane 6 Rocket: Europe's Heavy-Lift Success & Space Launch Evolution

- ULA's Vulcan Rocket Booster Problem: What Went Wrong [2025]

- Rocket Lab's Archimedes Engine Explosions: Why Blowing Up Is Part of the Plan [2025]

- SpaceX Common Carrier Status: Labor Law Exemption Explained [2025]

- NLRB Drops SpaceX Case: What It Means for Worker Rights [2025]

- Artemis II Wet Dress Rehearsal: NASA's Final Test Before Moon Launch [2025]