![Xflow Lands $16.6M From Stripe and PayPal to Fix Cross-Border B2B Payments [2025]](https://tryrunable.com/blog/xflow-lands-16-6m-from-stripe-and-paypal-to-fix-cross-border/image-1-1771913157730.jpg)

How Xflow is Disrupting Cross-Border B2B Payments with Stripe and PayPal's Backing

The cross-border B2B payments market is broken. Not metaphorically broken, but actually broken in ways that cost businesses millions annually and still rely on processes that haven't fundamentally changed since the 1980s. According to Statista, the global payments market is worth trillions, yet inefficiencies persist.

When an Indian exporter sends $2 million to a parent company for operations, they don't see the fees until the money lands. Sometimes it's a 2% haircut. Sometimes it's 3.5%. The settlement takes days, not hours. And the exchange rate they get? Whatever the bank felt like quoting that morning.

This is the problem Xflow is solving. The Bengaluru-based fintech startup just raised

Here's what makes this moment interesting. Cross-border B2B payments represent one of the last major financial infrastructure gaps in an otherwise digitizing world. India's domestic payment ecosystem—built on the Unified Payments Interface (UPI)—handles over 19 billion transactions annually with settlement happening in seconds. But the moment money leaves the country, everything reverts to legacy banking infrastructure.

Xflow's founders understand this friction intimately because they built cross-border payments at Stripe. Anand Balaji, Ashwin Bhatnagar, and Abhijit Chandrasekaran saw firsthand the gap between what's possible in modern fintech and what actually exists for businesses moving millions across borders.

The company claims to have processed $1 billion in annualized cross-border payment volume last year, up roughly 10-fold from 2024. Its customer base spans approximately 15,000 businesses, from SaaS firms and freelancers to global capability centers operated by multinational companies. This funding round opens the door to expanding that reach and adding new products on top of the core infrastructure.

But here's what you need to understand about why this matters. The cross-border B2B payments market is worth roughly $150 trillion globally, yet it remains dominated by banks charging 3-6% in fees, plus hidden FX spreads, plus settlement delays measured in business days rather than minutes. Fintech disruption has touched nearly every corner of payments, but this segment—the highest-value, highest-complexity corner—has been overlooked. Until now.

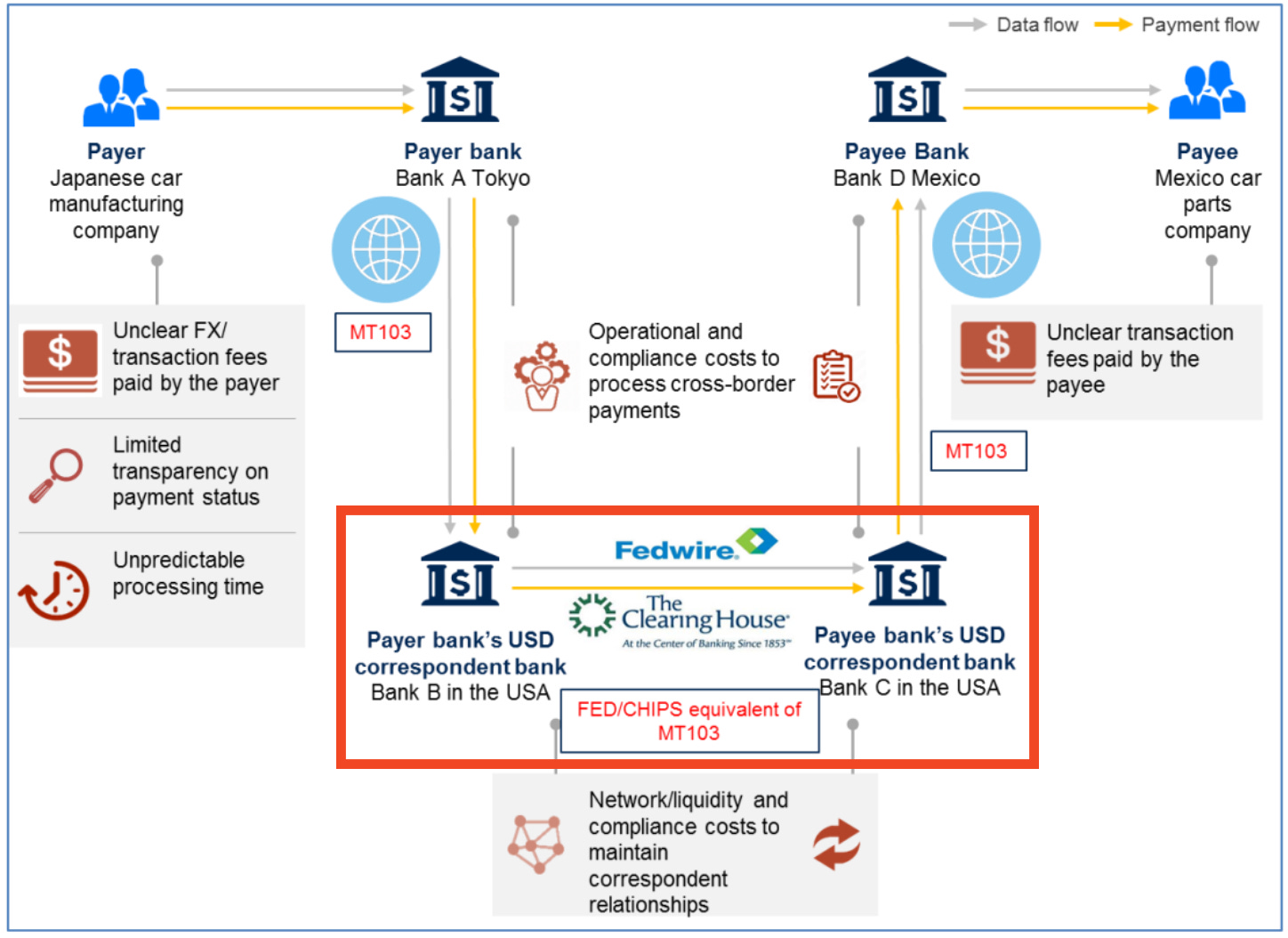

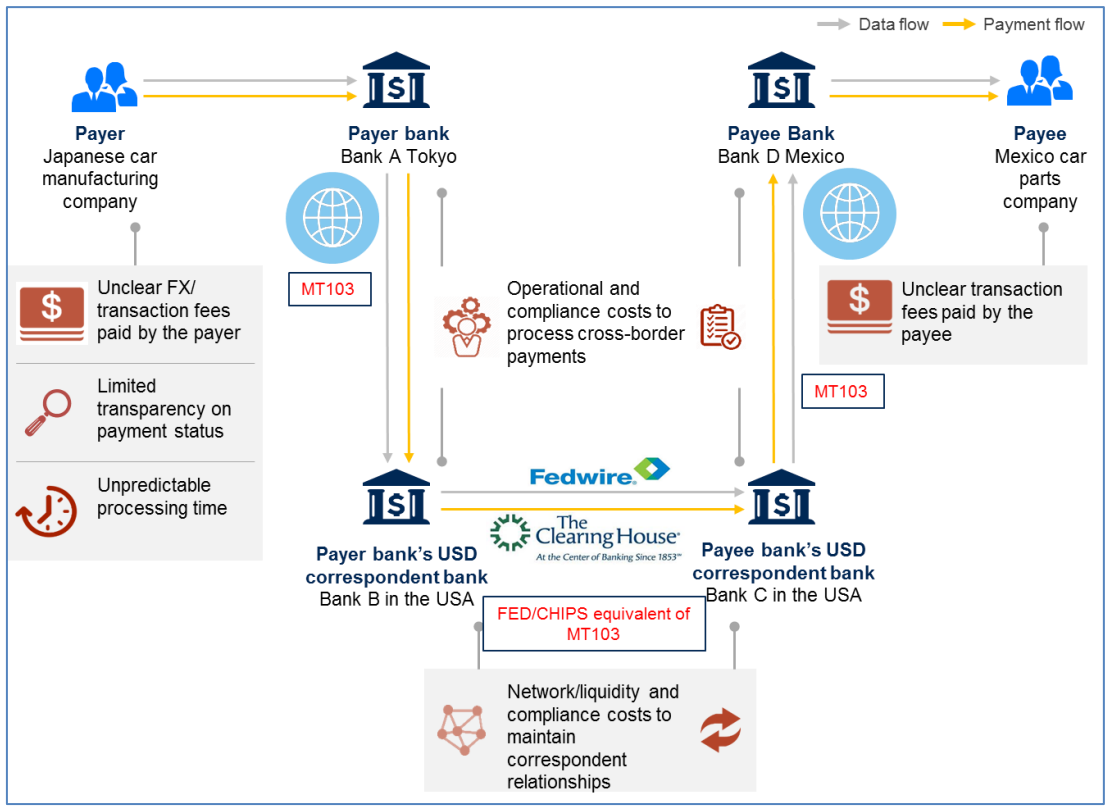

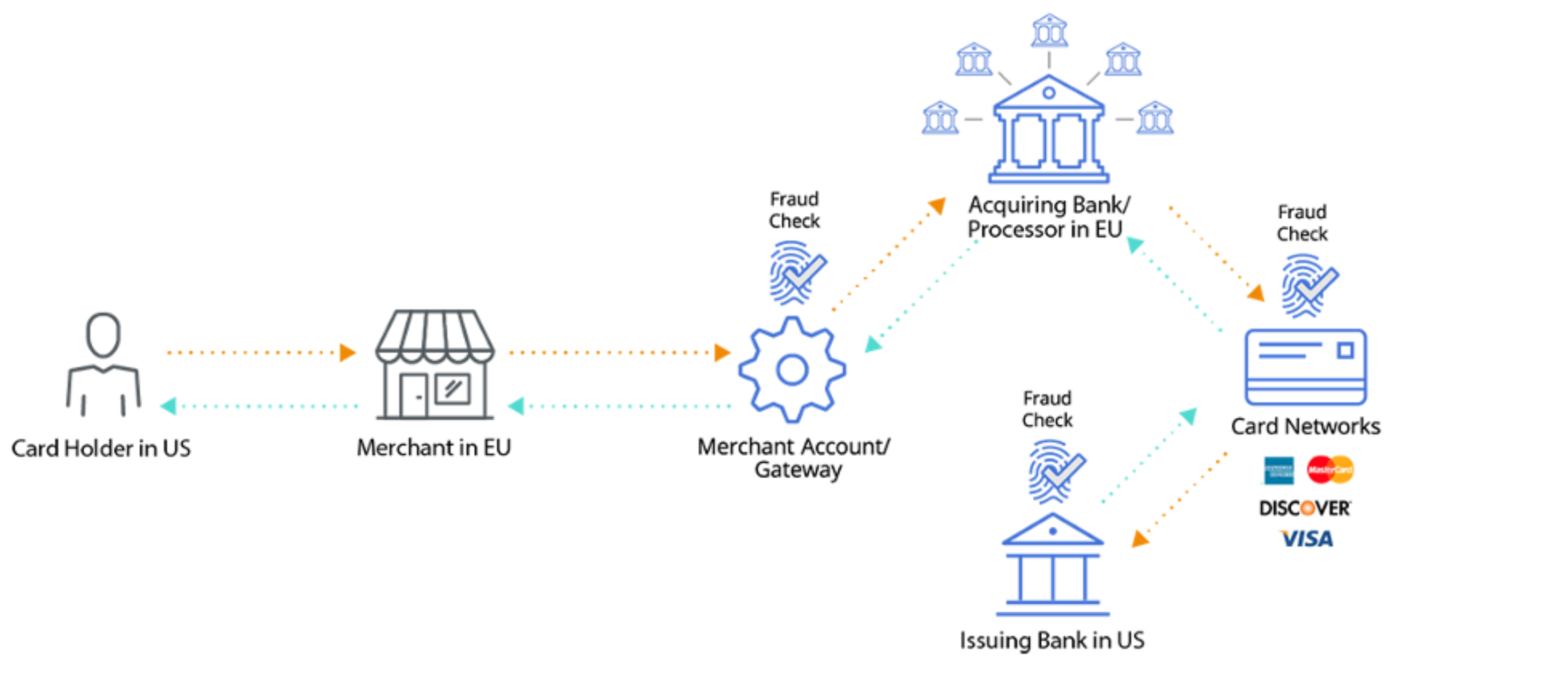

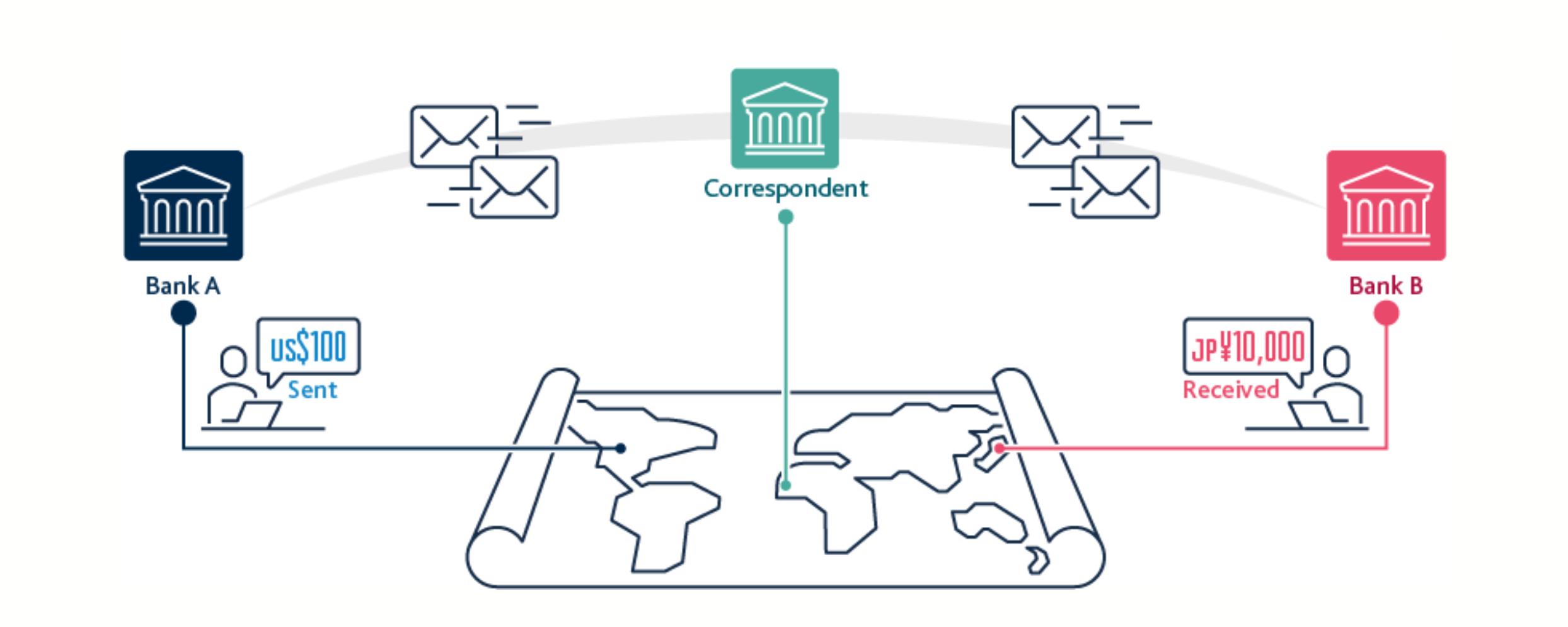

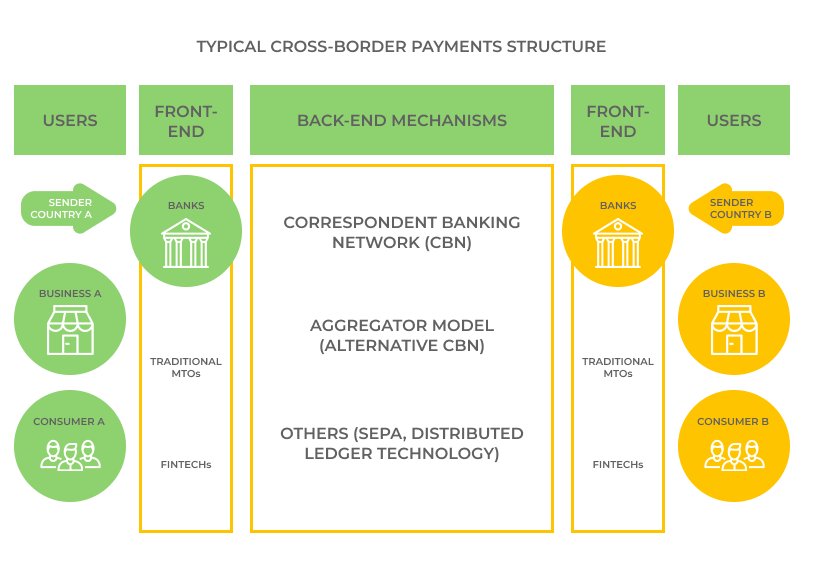

The Market Problem: Why Cross-Border B2B Payments Still Feel Like 1995

Take a concrete example. A mid-sized SaaS company based in Bangalore has customers across the US, EU, and APAC regions. Revenue flows in daily, but settlement to the Indian business bank account? That requires a series of manual steps: wire transfer instructions, bank codes, intermediary banks (sometimes multiple), and anywhere from 3-7 business days.

In that window, several things happen simultaneously: First, the company loses visibility into what's actually coming. FX rates fluctuate daily. An intermediary bank might shave 0.25% off the top for processing. The receiving bank applies its own fees. By the time money arrives, the original dollar amount and the rupee amount don't match what was expected—and nobody can explain why.

Scale this across thousands of transactions and you're looking at revenue leakage that nobody tracks properly. A

Now multiply that across India's entire export ecosystem. The country exported roughly $437 billion in goods and services in 2024. A significant portion of those payments come back through cross-border channels. And most of them still go through the same manual, slow, opaque process.

The problem gets worse at higher transaction sizes. Global capability centers—essentially offshore R&D and engineering centers that multinational companies operate in India—move millions monthly. An average transaction for these operations runs $1-2 million. The stakes are different. The players are different. But the infrastructure supporting these payments hasn't evolved.

The real kicker? Banks have no incentive to speed this up. They profit from the float, from the FX spread, from the opacity. A faster, more transparent system erodes those margins. So innovation in this space has to come from fintech players willing to build from scratch with different unit economics.

There's also a regulatory complexity layer. Cross-border transfers involve multiple jurisdictions, multiple currencies, and multiple layers of compliance. A UK bank wiring money to India goes through correspondent banking networks that add delays and fees at each hop. Building a platform that handles this requires deep expertise in regulatory frameworks across multiple markets.

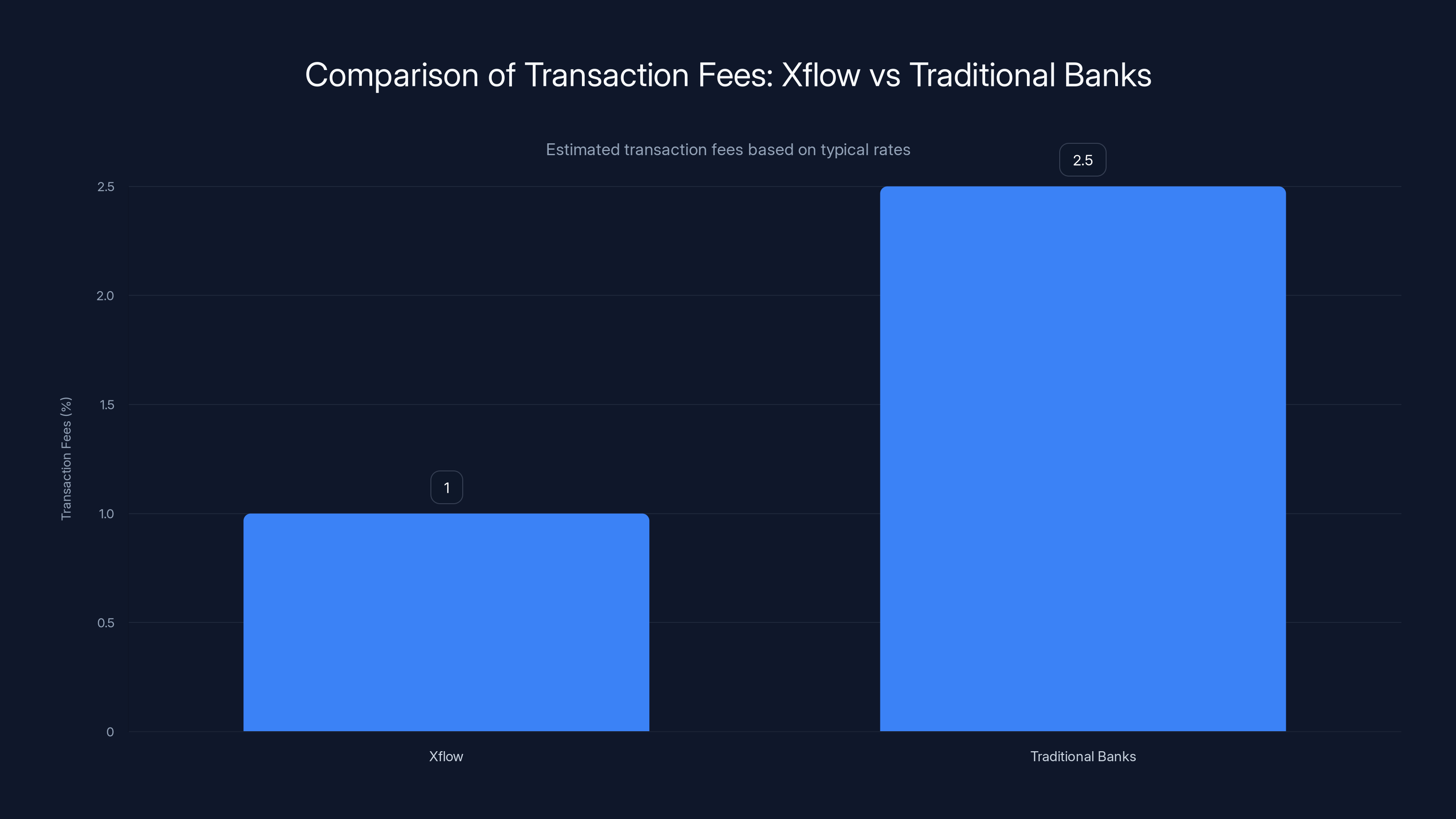

Xflow offers significantly lower transaction fees (1.0%) compared to traditional banks (2.5%), making it a cost-effective solution for cross-border payments. Estimated data.

Xflow's Solution: Infrastructure, Not Applications

Xflow's fundamental insight is that the market doesn't need another Wise or Remitly. The market needs the infrastructure layer that powers thousands of these services.

Specifically, Xflow positions itself as a payments infrastructure provider with APIs. Think of it like Stripe's original pitch for card payments. Before Stripe, accepting credit cards online required complex integrations, PCI compliance headaches, and relationships with multiple payment processors. Stripe abstracted all of that away into simple APIs.

Xflow is doing the same for cross-border B2B payments. Instead of SaaS companies, exporters, and platforms building their own cross-border infrastructure, they can embed Xflow's capabilities directly into their products via APIs.

Here's how it works in practice. A SaaS company wants to offer payment collection from international customers. Instead of implementing their own foreign exchange management, compliance checks, and settlement infrastructure, they call Xflow's API. Xflow handles the complexity. The SaaS company's customers see seamless international payment collection. Xflow gets the transaction flow and associated revenue.

This API-first approach matters because it changes the unit economics. Transaction fees become smaller in absolute terms, but volume scales exponentially because you're not competing on the consumer experience—you're enabling thousands of other services to offer that experience.

The company currently supports payments from over 100 countries in 25+ currencies, which means the infrastructure is already built to handle the global complexity. Their customer segments show the range:

SaaS firms typically move

This diversity matters. It means Xflow's infrastructure needs to handle everything from high-frequency small transactions to infrequent mega-transactions with vastly different customer sophistication levels.

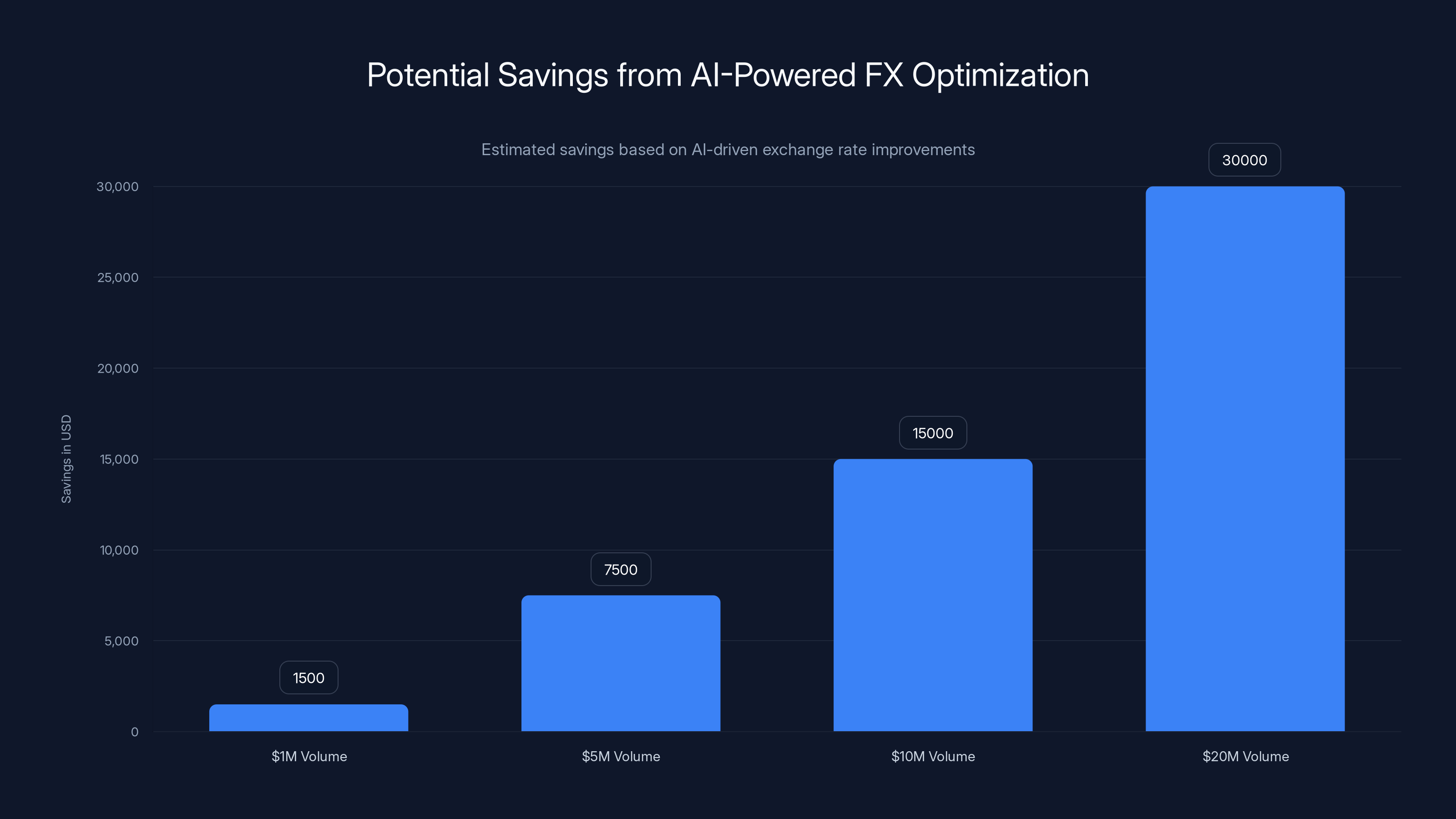

AI-driven FX optimization can lead to significant savings, with a

The AI Angle: Predictive Foreign Exchange Management

One feature that deserves deeper exploration is Xflow's AI-based foreign exchange optimization tool. This is where the company moves beyond being purely a pipe for payments.

Traditional cross-border payments present a timing problem. You need to move money, and you need to move it at some specific exchange rate. Most businesses take whatever rate is available at the moment of payment. Some sophisticated finance teams might watch trends and time transactions to catch favorable rates. But most SMBs? They just accept the daily bank quote.

Xflow's AI tool takes a different approach. Instead of forcing an immediate decision, the tool allows businesses to set target conversion rates—essentially limit orders for foreign exchange. The system then predicts exchange rate movements over the next three days with what the company claims is about 92% confidence.

When rates hit the target, the conversion happens automatically. It's like putting a limit order on a stock trade, except the asset is currency and the prediction engine is powered by machine learning models trained on historical FX data.

The practical impact? A company looking to move $1 million from USD to INR doesn't have to accept today's rate. If they're willing to wait, they can set a target rate. The system watches the market. When the rate moves to their target, the transaction executes automatically.

For high-volume businesses, this compounds. Even a 0.15% improvement in exchange rates across monthly transactions adds up to meaningful savings. A

Now, is 92% confidence a real number? TechCrunch's original reporting couldn't independently verify it, which tells you something. But the concept is sound. FX prediction is genuinely possible at 3-day time horizons using models trained on decades of tick-by-tick currency data combined with macroeconomic indicators.

Why Stripe and PayPal Ventures Are Betting on This

The fact that two of the world's largest payment ecosystems are simultaneously backing Xflow needs context. This isn't capital from generic venture firms hunting for returns. This is capital from operators.

Stripe's investment makes the most sense on the surface. Stripe was a founder himself to many of Xflow's leaders, so there's existing relationship and confidence. But it also signals something deeper: Stripe sees cross-border B2B as an important part of its future platform. By investing in Xflow, Stripe can potentially work with them, learn from them, and ensure they're plugged into the broader Stripe ecosystem.

PayPal's involvement is perhaps more significant. PayPal Ventures invests in companies that complement or extend PayPal's capabilities. PayPal's expertise has historically been in individual-to-individual and individual-to-merchant payments. But PayPal has been increasingly focused on B2B payment infrastructure over the past few years.

An investment in Xflow suggests PayPal sees the Indian cross-border B2B market as significant enough to warrant strategic capital. It also provides optionality—either as a potential acquisition target, a partnership, or simply as validation that this market is about to explode.

The broader funding round was led by General Catalyst, with existing investors Square Peg, Lightspeed, and Moore Capital also participating. This is a strong syndicate. General Catalyst is known for backing infrastructure plays in emerging markets. Square Peg is a top-tier Indian venture firm with deep local expertise.

Total funding to date exceeds

Wise and Payoneer lead the cross-border payments market with strong B2C and small B2B focus, while Xflow differentiates by targeting high-value transactions. Estimated data.

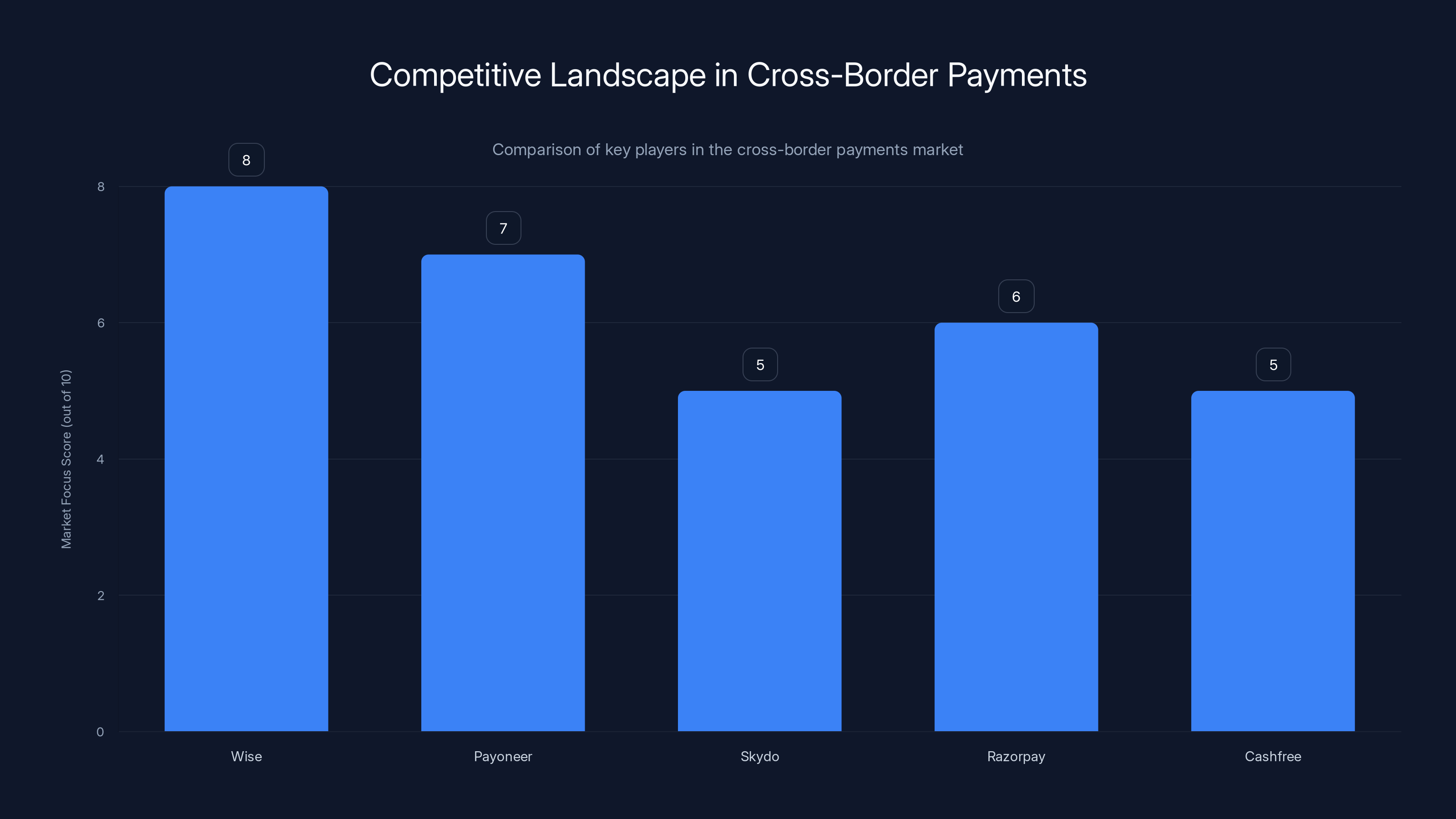

The Competitive Landscape: Wise, Payoneer, and Everyone Else

Xflow isn't operating in a vacuum. The cross-border payments market has several strong competitors already established.

Wise is the obvious one. Wise started in the UK as TransferWise, focused on helping individuals and small businesses send money internationally. Wise has expanded into business payments and now handles tens of billions in annual volume. Wise's magic is transparency and real exchange rates. Their entire brand is built on "hiding the real cost of international money transfers."

But Wise's model is still primarily B2C and small B2B. The company makes money on transaction volume and small markup on FX rates. This works great for frequent, moderate-size transfers. It works less well for the $10 million global capability center transaction that happens once a quarter.

Payoneer operates in a similar space, primarily targeting freelancers and small businesses with international payment collection and payout capabilities. Payoneer's volume is significant, but again, the company serves a different customer segment than Xflow's sweet spot.

Skydo and other players focus on specific corridors or specific customer segments. Some companies like Razorpay and Cashfree have launched cross-border features, but again, these are additions to broader payment platforms rather than core infrastructure.

Xflow's differentiation rests on several factors:

First, focus on high-value transactions. The $1-2 million transaction for a global capability center isn't typical for fintech payments companies. These transactions still almost exclusively flow through banks. Xflow is specifically building for this segment.

Second, API-first infrastructure. Unlike most competitors, Xflow isn't building a direct-to-consumer app or a SaaS dashboard. The company is building APIs that other platforms can embed. This is a more capital-efficient model and creates network effects as more platforms integrate.

Third, deep India expertise combined with global operations. The founders built Stripe's India business, which means they understand both the Indian regulatory environment and the global payment infrastructure. This combination is rare.

Fourth, regulatory positioning. Xflow has secured a Payment Aggregator–Cross Border (PA-CB) license from the Reserve Bank of India. It also holds a payments license in Canada and is pursuing licenses in Singapore. This regulatory progress matters because it validates the legitimacy of the business model.

But competition will intensify. Wise is watching this market. PayPal is absolutely watching this market. And banks themselves may eventually modernize their offerings, though this is unlikely given the incentives involved.

The India Opportunity: Why Now?

There's a timing element worth exploring. Why is this happening in 2025, not 2020?

Several macro trends converged. First, India's domestic payment infrastructure has matured significantly. UPI processes over 19 billion transactions monthly, and the entire ecosystem is extremely digital. This created a benchmark. When you're using UPI for domestic payments and paying near-zero fees, waiting days for a cross-border payment while paying 3-6% in fees feels broken.

Second, India's tech export economy scaled dramatically. The global capability center model expanded. More companies established significant engineering operations in India. More SaaS companies were founded in India. All of these segments needed efficient cross-border payment solutions.

Third, regulatory clarity improved. The Reserve Bank of India has been increasingly open to fintech innovation in the payments space, including creating specific license categories for cross-border payments. This created a path for startups that didn't previously exist.

Fourth, international investor sophistication about the India opportunity reached a tipping point. Early-stage India fintech companies struggled to raise because international VCs didn't understand the market. By 2024, India was a proven market for fintech. Capital became available.

Fifth, and importantly, the pain became quantifiable. As more companies operated cross-border, they started measuring the actual cost of international transfers. They realized they were bleeding money. This created immediate demand rather than hypothetical demand.

Xflow's timing is smart. The company is entering a market that's large, underserved, and increasingly frustrated with the status quo.

A mid-sized SaaS company with

Product Roadmap: What's Coming

Xflow's near-term product expansion includes import capabilities and geographic expansion. Imports are crucial because the infrastructure needs to work bidirectionally. Companies need to collect international payments, but they also need to make international payments. An Indian company might need to pay suppliers in Vietnam or processors in the US.

Geographic expansion into Singapore and other markets makes sense given the concentration of multinational companies and regional hubs in Southeast Asia. Singapore is particularly strategic because it's a major financial hub with significant flows between India and the rest of Asia.

The company also plans to build additional products on top of the core infrastructure. This could include things like automated invoice management, expense categorization, reporting dashboards, or working capital solutions. Infrastructure companies typically evolve this way—start with the core utility, then wrap value-added services around it.

Existing partnerships with Easebuzz and Drip Capital suggest a strategy of embedding into existing platforms rather than building end-to-end. Easebuzz is a payment aggregator for businesses. Drip Capital is a supply chain finance company. Both need cross-border capabilities. By embedding Xflow, these platforms can offer international payment features without building in-house.

This partnership approach is evidence-based. The company isn't trying to be everything to everyone. Instead, it's becoming the infrastructure layer that powers other platforms.

The Regulatory Path: Navigating RBI Requirements

The Reserve Bank of India's Payment Aggregator–Cross Border license is a recent development worth understanding. The RBI created this license category specifically to enable fintech companies to operate cross-border payment services without becoming full banks.

Obtaining this license requires demonstrating regulatory compliance, financial stability, and technical security. The fact that Xflow has already secured it suggests they've satisfied the RBI's requirements—no small feat for a startup.

This matters because it provides legal certainty. Xflow can operate in India's market with explicit regulatory approval, which reduces the risk for large enterprise customers. Global capability centers and SaaS companies can confidently use the platform knowing it's operating within the regulatory framework.

Canada's payments license suggests similar progress in another key market. Canada is important for Indian companies because of the large Indian diaspora population and the significant IT services trade between India and Canada.

The Singapore license pursuit is strategic for regional expansion without needing to raise additional capital for each new market. A Singapore license could enable operations across Southeast Asia.

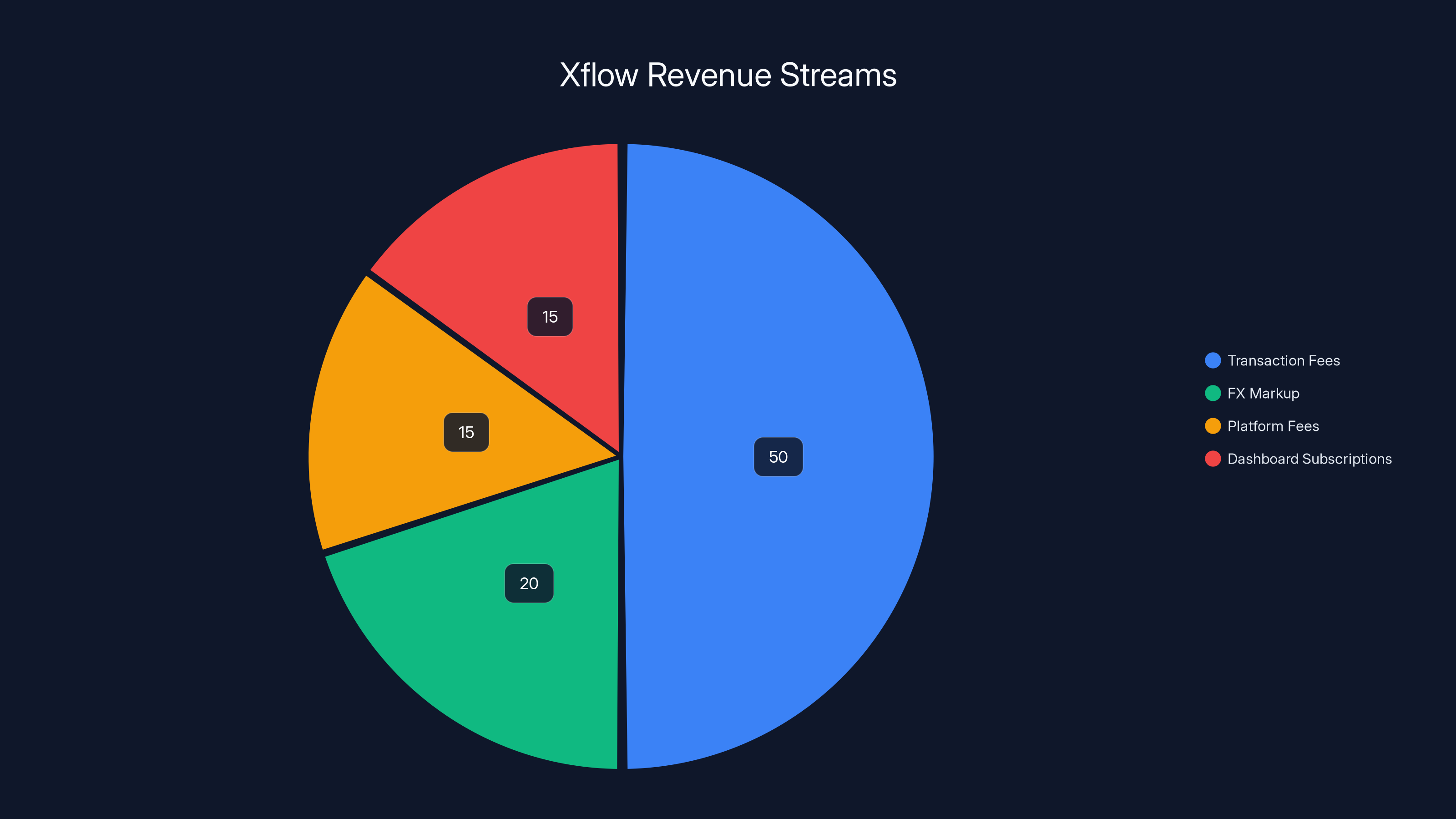

Estimated data suggests that transaction fees are the largest revenue source for Xflow, followed by FX markup and subscription fees. Estimated data.

Business Model: How Xflow Makes Money

Xflow hasn't disclosed exact pricing, but the model is likely transaction-based with a small percentage fee plus some markup on FX conversions. This is standard for payment infrastructure.

For developers and platforms embedding Xflow's APIs, there's likely a per-transaction fee (something like 0.5-1.5% of transaction value) plus a flat monthly platform fee for higher-volume users. This covers infrastructure costs, compliance, and customer support.

For direct customers using Xflow's dashboard and tools, the model might include tiered pricing based on transaction volume with lower percentage fees for high-volume users.

The FX markup is important but not disclosed. Based on the AI optimization feature, Xflow likely marks up FX rates slightly, but lower than banks. Instead of the typical 2-3% FX spread that banks apply, Xflow might apply 0.25-0.5%. This is still a 5-10x improvement for customers while providing meaningful revenue for Xflow.

At

This suggests the company is likely approaching profitability or is already profitable on an operational basis. The $16.6 million raise isn't necessarily for survival—it's for acceleration and geographic expansion.

The Broader Infrastructure Play

What's interesting about Xflow's success is what it says about the broader infrastructure opportunity in emerging markets. India's fintech revolution typically gets discussed in consumer payment terms: mobile wallets, UPI, digital banking. But infrastructure—the pipes that other companies build on—is the less glamorous but more defensible business.

If Xflow captures even a modest portion of cross-border B2B payment infrastructure in India, the revenue potential is substantial. And if the model works in India, it could scale to other emerging markets with similar characteristics: large export economies, mature domestic digital payment systems, and significant diaspora populations.

This is precisely why Stripe and PayPal are interested. These companies understand that controlling the infrastructure layer is more valuable long-term than controlling the interface layer. Build the pipes, own the flow, everyone else builds products on top.

Market Size and Growth Potential

Global cross-border B2B payment volume exceeds

If Xflow can capture even 1-2% of Indian cross-border B2B volume, that's

The company processed $1 billion in 2024 (implied by the 10x growth claim), so they're currently capturing roughly 0.02% of the Indian cross-border market. Reaching 1% would require 50x growth over the next 3-5 years. This is ambitious but not unrealistic for infrastructure play with strong founding team and payment from major investors.

Customer Acquisition and Go-To-Market Strategy

Xflow's current 15,000 customer base suggests they're doing something right in acquisition. The range of customer types—from freelancers moving

For platform partnerships (Easebuzz, Drip Capital), the acquisition model is basically sales to the platform. Once integrated, customers of these platforms get access to Xflow's capabilities automatically.

For direct customers, acquisition likely happens through multiple channels: industry-specific marketing targeting exporters and SaaS companies, content marketing around FX optimization, and partner referrals.

The company is also likely doing deeper relationship building with large customers. Global capability centers moving millions monthly warrant account management and custom support, not self-service models.

What Could Go Wrong

For all the positive signals, several risks exist. First, regulatory changes in India or major markets could restrict the business. The RBI could tighten cross-border payment rules in ways that hurt fintech companies. This is unlikely but possible.

Second, competition from banks shouldn't be discounted. Major Indian banks like HDFC, ICICI, and Axis Bank could modernize their cross-border offerings. They have the regulatory authority, the customer relationships, and the capital. If they do, they'd likely use pricing power and bundling (cross-border payments bundled with working capital, payroll, etc.) to compete.

Third, the international payment landscape is crowded. Wise continues to expand. New entrants constantly emerge. Unless Xflow's moat is very strong, it could become a commodity.

Fourth, the fundraising itself could create operational challenges. Rapid growth puts strain on teams, compliance, and infrastructure. Companies that raise significant capital often make growth mistakes.

Fifth, the global macro environment matters. If cross-border trade volumes decline due to recession or trade wars, demand contracts.

But the company has mitigated several risks. The Stripe and PayPal backing suggests both institutional confidence and potential access to those companies' ecosystems. The regulatory licenses provide legal certainty. The 10x growth rate is real and demonstrates strong product-market fit.

The Broader Fintech Context

Xflow's raise comes at an interesting moment for India's fintech market. After years of explosive growth in consumer payments, the market is consolidating. Venture capital is increasingly focused on unit economics and path to profitability rather than growth at all costs.

Xflow's positioning as a B2B infrastructure company with clear revenue generation aligns with this shift. The company isn't burning capital to acquire individual users. It's enabling other businesses to serve their customers better, taking a small cut on each transaction.

This infrastructure-first approach is proving more durable than consumer-first approaches in India's fintech market. Companies like Razorpay, which started as a payments processor and expanded into infrastructure, have proven more resilient than companies that started with direct consumer acquisition.

Xflow seems to have learned this lesson from the start. The API-first approach, the platform partnerships, the focus on high-value transactions—all of this suggests a team that understands what actually works in payments infrastructure.

What's Next: The 12-Month Outlook

Over the next year, Xflow will likely focus on geographic expansion (Singapore license, Southeast Asia operations), product expansion (import capabilities, working capital solutions), and customer growth.

The company has suggested it will maintain India as its primary market while expanding internationally. This makes sense. India is where the company has regulatory clarity, product-market fit, and execution confidence. Expanding elsewhere uses similar infrastructure and processes but requires new regulatory work and market education.

You should also expect partnership announcements. Fintech companies operating at the infrastructure layer typically announce partnerships frequently as part of their go-to-market strategy. More platforms adopting Xflow means more distribution channels and more transactions.

The next funding round, if it happens, will likely be Series B in 18-24 months. By then, the company will have demonstrated sustained growth, expanded to 2-3 new geographies, and added multiple new products. A Series B would likely be

Why This Matters Beyond Xflow

Ultimately, Xflow's success matters because it validates a thesis that's been under-explored: infrastructure plays in emerging markets' fintech ecosystems are extremely valuable.

Remember, cross-border B2B payments have been broken for decades. Banks haven't fixed it because they profit from the inefficiency. International remittance companies like Wise fixed some of it for consumers and small businesses. But the mid-market to enterprise segment—millions of dollars in monthly cross-border transfers—has been ignored.

Xflow is proving that this segment is underserved and valuable. If the company succeeds in becoming the infrastructure layer for cross-border B2B payments in India, it won't just be a successful startup. It will be the foundation on which thousands of other services are built.

That's the Stripe playbook. And that's what makes Stripe and PayPal's confidence in Xflow more than just a financial investment. It's validation that cross-border B2B payments is the next frontier for fintech infrastructure in emerging markets.

FAQ

What is Xflow and what problem does it solve?

Xflow is a cross-border B2B payments infrastructure company based in Bengaluru that allows Indian businesses, exporters, and SaaS firms to collect and send international payments with greater transparency, faster settlement, and lower fees than traditional banking channels. The company solves the fundamental problem that cross-border B2B payments remain stuck in legacy banking infrastructure, with hidden fees, unpredictable exchange rates, and settlement delays measured in days rather than minutes.

How does Xflow's business model work?

Xflow operates as a payments infrastructure provider using an API-first approach. Instead of building a direct-to-consumer payment app, the company allows platforms, exporters, and SaaS companies to embed cross-border payment capabilities directly into their own products. The company generates revenue through transaction fees (typically 0.5-1.5% per transaction), platform fees, and small markups on foreign exchange conversions—significantly lower than the 2-3% FX spreads traditional banks apply. This model allows Xflow to scale efficiently without needing to acquire individual customers directly.

What are the key features of Xflow's platform?

Xflow's platform includes cross-border payment collection and settlement in over 100 countries across 25+ currencies, an AI-powered foreign exchange optimization tool that provides three-day FX rate forecasts with 92% confidence, regulatory compliance through RBI's Payment Aggregator–Cross Border (PA-CB) license and Canadian payments license, and API infrastructure that allows platforms to embed these capabilities into their own products. The platform supports transaction sizes ranging from

Why is Xflow's funding round from Stripe and PayPal significant?

The backing from Stripe and PayPal Ventures represents validation from two of the world's largest payment ecosystems and suggests these companies see significant value in cross-border B2B payments as a strategic focus area. For Xflow, this provides not just capital but credibility with banking and regulatory partners, potential partnerships with these platforms, and access to their ecosystems and expertise. The participation of both companies signals the market opportunity is real and worth pursuing at scale.

What distinguishes Xflow from competitors like Wise and Payoneer?

Unlike Wise, which focuses primarily on individual and small business transfers with moderate transaction sizes, Xflow specifically targets high-value B2B transactions ($1-10 million ranges). Unlike Payoneer, which serves freelancers, Xflow built an infrastructure-first model allowing platforms to embed its capabilities rather than requiring direct customer acquisition. Xflow also differentiates through deep India expertise from founders who built Stripe's India business, specific focus on the Indian export economy, and regulatory positioning through dedicated cross-border licenses.

What is the market size opportunity for Xflow?

Global cross-border B2B payment volume exceeds

How does Xflow's AI-powered FX optimization work?

Xflow's AI tool allows businesses to set target exchange rates instead of accepting prevailing bank quotes, similar to limit orders in trading. The system uses machine learning models trained on historical foreign exchange data to predict exchange rate movements over the next three days, then automatically executes conversions when rates hit the customer's target. The company claims this feature delivers approximately 92% accuracy in three-day forecasts, enabling businesses to optimize FX timing and capture better rates than they would through immediate market conversions.

What regulatory approvals has Xflow secured?

Xflow has obtained the Payment Aggregator–Cross Border (PA-CB) license from the Reserve Bank of India, enabling cross-border payment operations covering both exports and imports. The company also holds a payments license in Canada and is actively pursuing licenses in Singapore, which signals a strategy of expanding into additional key markets while maintaining India as its primary focus. These regulatory approvals provide legal certainty and reduce customer risk, making Xflow attractive to enterprise customers requiring compliance confidence.

What are Xflow's growth metrics and customer base?

Xflow processes approximately

What does Xflow plan to do with the Series A funding?

According to company founders, Xflow plans to deploy the $16.6 million Series A funding toward building additional products on top of its core payments infrastructure, securing regulatory licenses in new markets like Singapore, expanding geographic operations, and accelerating customer acquisition. Near-term product roadmap includes import capabilities (enabling businesses to both collect and pay internationally) and enhanced working capital solutions, while partnerships with platforms like Easebuzz and Drip Capital suggest a strategy of embedding Xflow's infrastructure into broader fintech ecosystems.

What could potentially threaten Xflow's growth?

Key risks include potential regulatory changes from the Reserve Bank of India that could restrict fintech cross-border operations, competition from major Indian banks that could modernize their cross-border offerings using pricing power and customer bundling, and competition from established international players like Wise and emerging fintech competitors. Additionally, the company faces operational scaling challenges from rapid growth, macroeconomic risks if cross-border trade volumes decline, and the risk of becoming commoditized if the technology moat proves weak. However, founder credibility, strategic investor backing, and regulatory approvals substantially mitigate these risks.

Try automating your cross-border payment workflows with intelligent infrastructure solutions. Runable helps fintech teams build and scale payment automation with AI-powered workflows, custom integrations, and real-time monitoring—all without extensive coding. Start building smarter payment infrastructure today at runable.com for just $9/month.

Key Takeaways

- Xflow raised 85M post-money valuation based on 10x growth to $1B annualized volume

- The company differentiates by targeting high-value B2B transactions ($1-2M for global capability centers) with API-first infrastructure model, not direct consumer apps

- Cross-border B2B payments remain dominated by legacy banking infrastructure charging 2-3% in opaque FX fees and taking 3-7 days for settlement—Xflow promises transparency and speed

- Xflow's AI-powered FX optimization tool predicts exchange rates three days ahead with 92% confidence, allowing businesses to set limit orders for currency conversions

- With India's $4.5-6 trillion annual cross-border B2B market and Xflow capturing only 0.02%, the company has 50x+ growth runway if it achieves 1% market share

Related Articles

- InScope Raises $14.5M to Automate Financial Reporting [2025]

- DG Matrix Raises $60M: Solid-State Transformers Transform Data Center Power [2025]

- Ever's AI-Native EV Marketplace: How $31M Redefines Auto Retail [2025]

- Complyance Raises $20M Series A: How AI Is Reshaping Enterprise Compliance [2025]

- Resolve AI's $125M Series A: The SRE Automation Race Heats Up [2025]

- Linq's $20M Series A: How AI Assistants Are Moving Into Messaging Apps [2025]