![Epstein Files and EV Startups: Silicon Valley's Hidden Connections [2025]](https://tryrunable.com/blog/epstein-files-and-ev-startups-silicon-valley-s-hidden-connec/image-1-1771175164552.jpg)

Epstein Files and EV Startups: Silicon Valley's Hidden Connections

When federal investigators released thousands of pages from the Jeffrey Epstein case, most headlines focused on his criminal network and victims. But buried deep in those documents sat something else entirely: a detailed map of how a mysterious businessman named David Stern funneled money into some of Silicon Valley's most ambitious electric vehicle startups.

This story matters because it exposes something uncomfortable about venture capital in the 2010s: a willingness to ask very few questions about where money came from, who was behind it, and what networks they belonged to. The Epstein files reveal a decade-long relationship between Stern and the infamous financier, one where Stern pitched investments in Faraday Future, Lucid Motors, and Canoo, three companies that shaped the modern EV landscape.

None of these companies ever accepted Epstein's money directly. But that's not really the point. The revelations show how interconnected finance really is, and how someone operating at the edges of respectability could access the highest levels of Silicon Valley's startup ecosystem. It's a reminder that venture capital's greatest vulnerability isn't bad judgment about technology—it's bad judgment about people.

This article digs into what those files actually revealed, why the EV space was so attractive to mystery investors, and what it means for Silicon Valley's future.

TL; DR

- David Stern pitched hundreds of millions in potential investments to Epstein across three major EV startups (Faraday Future, Lucid, Canoo) between 2008 and 2010

- Canoo had the most mysterious funding structure of any major EV startup, with early backers later revealed to include Chinese government connections and a businessman linked to Epstein

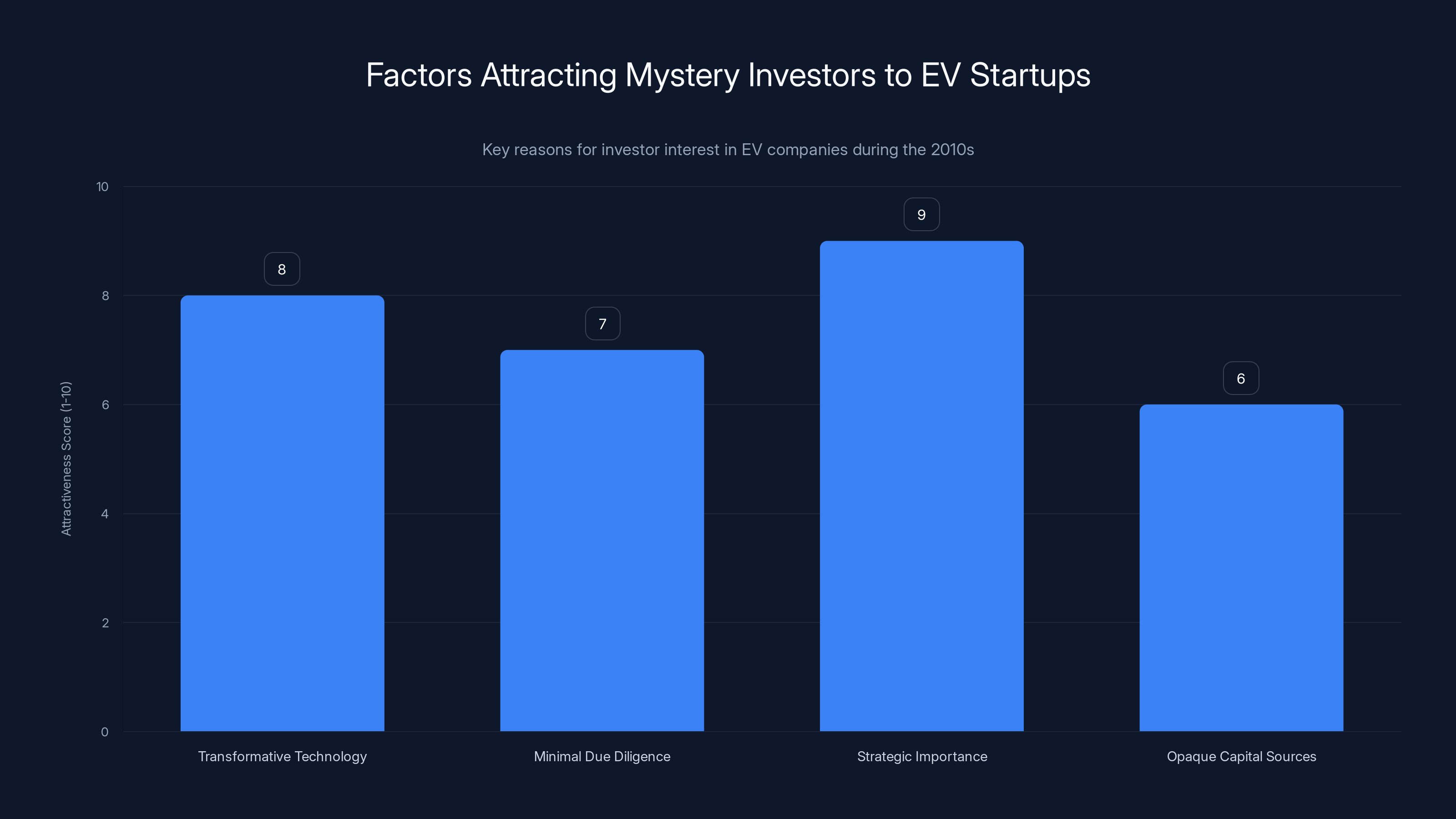

- The EV space attracted shadowy money because it promised transformative returns and required minimal transparency about investor backgrounds

- Silicon Valley knew surprisingly little about who was funding these companies until lawsuits forced disclosure

- The broader question remains unanswered: How many other startups benefited from connections or funding networks no one ever scrutinized?

Electric vehicle startups were highly attractive to investors due to their transformative technology, strategic importance, and the ease of investing with minimal scrutiny. (Estimated data)

Who Was David Stern? The Businessman No One Could Figure Out

For years, David Stern existed as a ghost in the EV investment world. Industry reporters covering startups knew he was involved with Canoo. They knew he had some connection to China. Beyond that, almost nothing.

Stern wasn't the type to give interviews. He didn't court attention. He showed up in cap tables and investor lists, vaguely identified as a "German businessman" with unclear motivations. The most specific detail anyone had was a passing mention that he was somehow connected to Prince Andrew, the British royal with his own complicated history. That detail, it turns out, was the thread that unraveled everything.

When Epstein's files became public, Stern's relationship to him revealed a decade of financial discussions, introductions, and pitches. Starting around 2008, Stern approached Epstein looking for capital. The two developed what court documents suggest was a genuine business relationship, with Stern leveraging Epstein's money and connections to pursue opportunities in electric vehicles and Chinese technology investments.

What's remarkable is how unremarkable this seemed at the time. Tech investors routinely work with people they know little about. Due diligence on investor backgrounds is often treated as optional rather than essential. Stern benefited from an ecosystem where asking hard questions about who someone was, or where their money came from, was considered impolite or excessive.

The connection to Prince Andrew, which should have triggered alarm bells, instead seemed to legitimize Stern. Royal connections suggested sophistication and access. No one dug deeper. That was the real vulnerability.

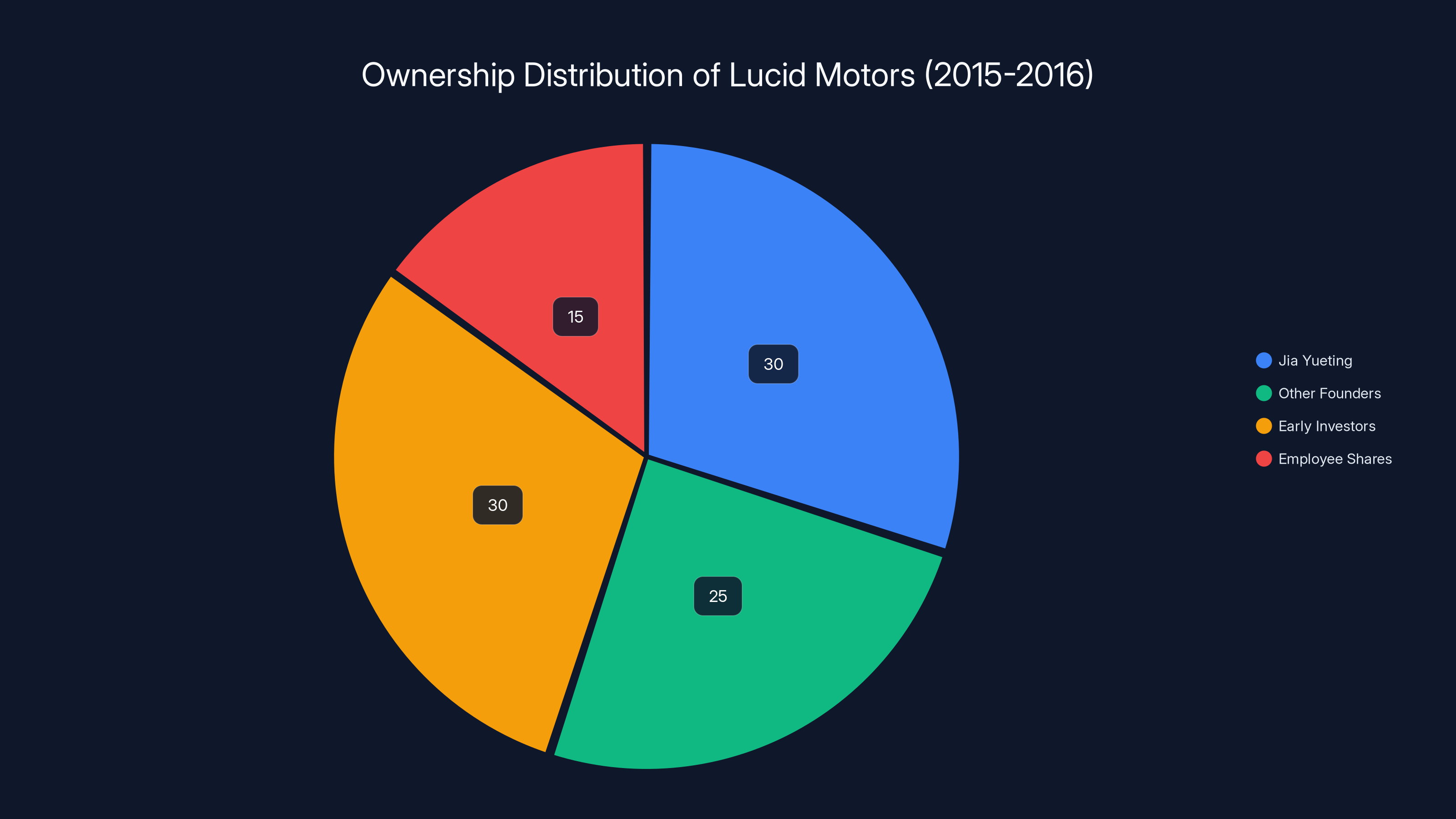

Estimated data shows Jia Yueting held a significant 30% stake in Lucid Motors, highlighting the concentrated ownership typical of EV startups during the 2010s.

The Electric Vehicle Boom: Where Money Didn't Need a Pedigree

The mid-to-late 2000s and early 2010s represented something unique in venture capital history: an intense, almost religious belief that electric vehicles represented the future of transportation. Every major automaker wanted a piece of it. Every investor wanted exposure. And because the technology was genuinely revolutionary, due diligence standards somehow became less stringent, not more.

This created perfect conditions for mystery money. If you could promise revolutionary EV technology, investors stopped asking normal questions. Chinese money, which began flowing into the space around 2010-2012, arrived with minimal transparency about its sources. Some came from private investors. Some came from state-owned enterprises. The distinction often got blurred.

Stern positioned himself as a connector between these worlds. He understood Chinese business relationships. He claimed access to capital. He pitched transformative opportunities. These were exactly the credentials that mattered in the EV space at that moment.

What Silicon Valley investors didn't do, crucially, was verify any of it. The due diligence process in venture capital typically focuses on technology risk and market opportunity. It rarely examines the personal history of individual investors seeking to participate. Stern's background, wealth sources, and network were treated as his own business. So long as he had money and connections, that was sufficient.

Faraday Future: The Hundred-Million-Dollar Pitch That Never Landed

Faraday Future, founded by billionaire Jia Yueting, represented the most ambitious EV startup of its era. It promised revolutionary battery technology, autonomous capabilities, and a complete reimagining of the electric vehicle. For investors willing to believe, it offered near-infinite upside.

According to the Epstein files, David Stern repeatedly pitched Epstein on investing hundreds of millions of dollars into Faraday Future. The conversations spanned months. Stern painted a picture of a company that would reshape the automotive industry. He discussed financial structures, investment vehicles, and expected returns. Epstein listened, considered, and ultimately declined. No deal materialized.

But here's what made this significant: Stern had direct access to Epstein's capital and ear specifically because he could pitch deals like Faraday Future. The EV space provided cover. A businessman with murky credentials could transform himself into a legitimate investor simply by having exposure to EV opportunities.

Faraday Future eventually collapsed under the weight of its ambitions, financial mismanagement, and Chinese regulatory complications. It never achieved commercial scale. But in the moment, when Stern was pitching it to Epstein, it represented everything that made the EV space attractive to money with few questions asked.

The Faraday example demonstrates a crucial dynamic: even rejected investments can reveal problems. The fact that Epstein was being pitched major EV deals shows that the barrier to accessing serious capital in the space was remarkably low. You didn't need a track record. You didn't need a reputation. You needed a story and a connection.

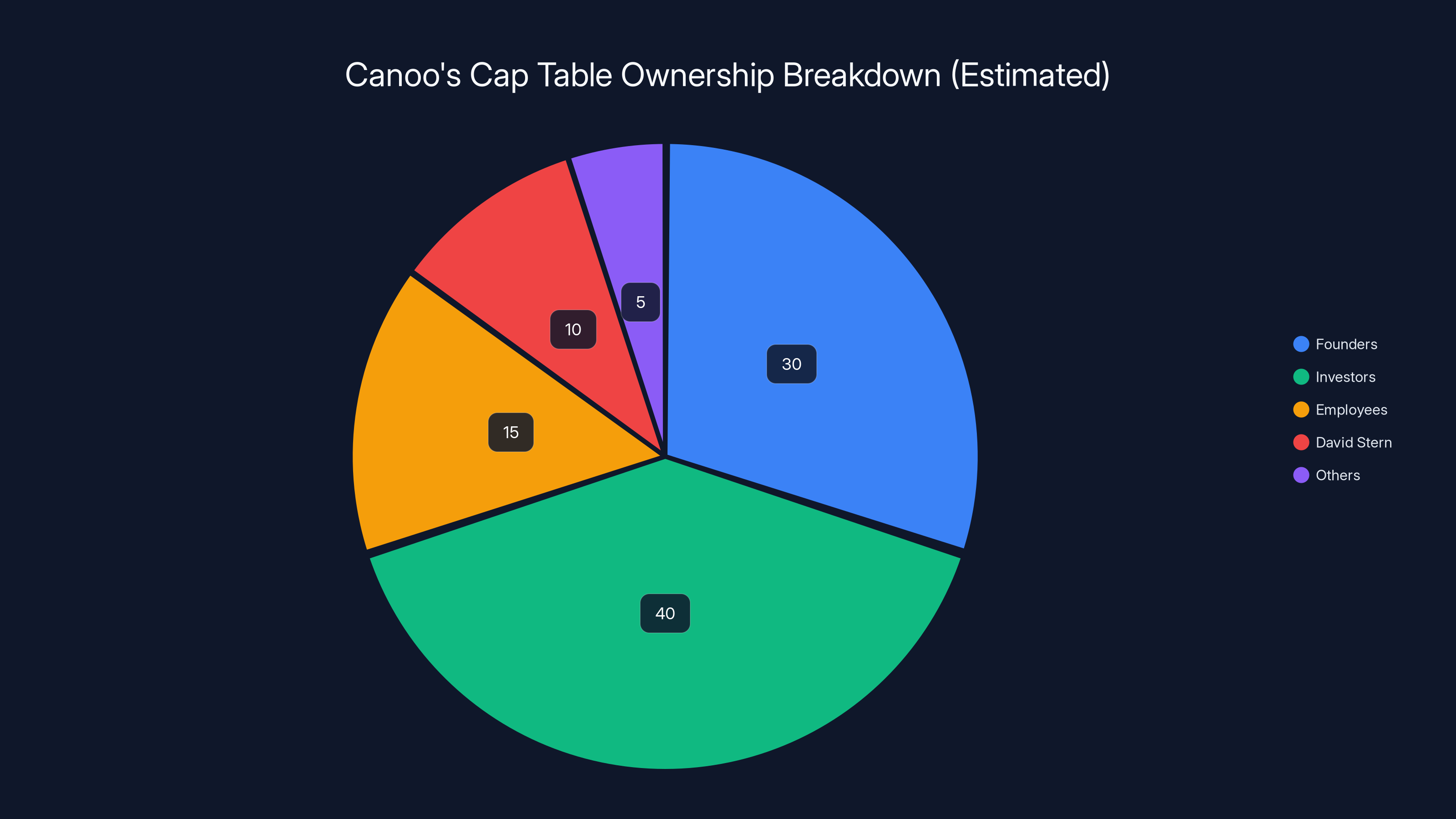

Estimated data showing a typical startup cap table distribution, highlighting the obscured ownership structure of Canoo at its launch.

Lucid Motors and the 30% Stake Deal: The Overlooked Acquisition

One detail from the Epstein files deserves more attention than it initially received: David Stern's involvement in a proposed acquisition of a significant stake in Lucid Motors through Faraday Future founder Jia Yueting's holdings.

Around 2015-2016, before Lucid became one of the most valuable EV startups in the world, Yueting had acquired roughly 30% of Lucid stock. According to court documents, Stern proposed that Epstein help finance a purchase of that stake, giving Epstein and his associates control of a major position in what many believed would be the next major EV manufacturer.

This deal structure is revealing because it shows how opaque EV startup ownership actually was. Lucid was a private company pursuing secretive development of advanced battery technology and autonomous driving systems. Yet a businessman with limited public credibility could propose to Epstein that he acquire a massive stake in the company through relatively simple negotiations with a single founder.

The deal never closed. Lucid pursued other funding routes, eventually taking investment from Saudi Arabia's Public Investment Fund, which brought its own set of geopolitical complications. But the fact that this deal was even proposed and seriously discussed suggests how little institutional rigor governed access to major EV companies during that era.

Canoo: The Company Built on Mystery

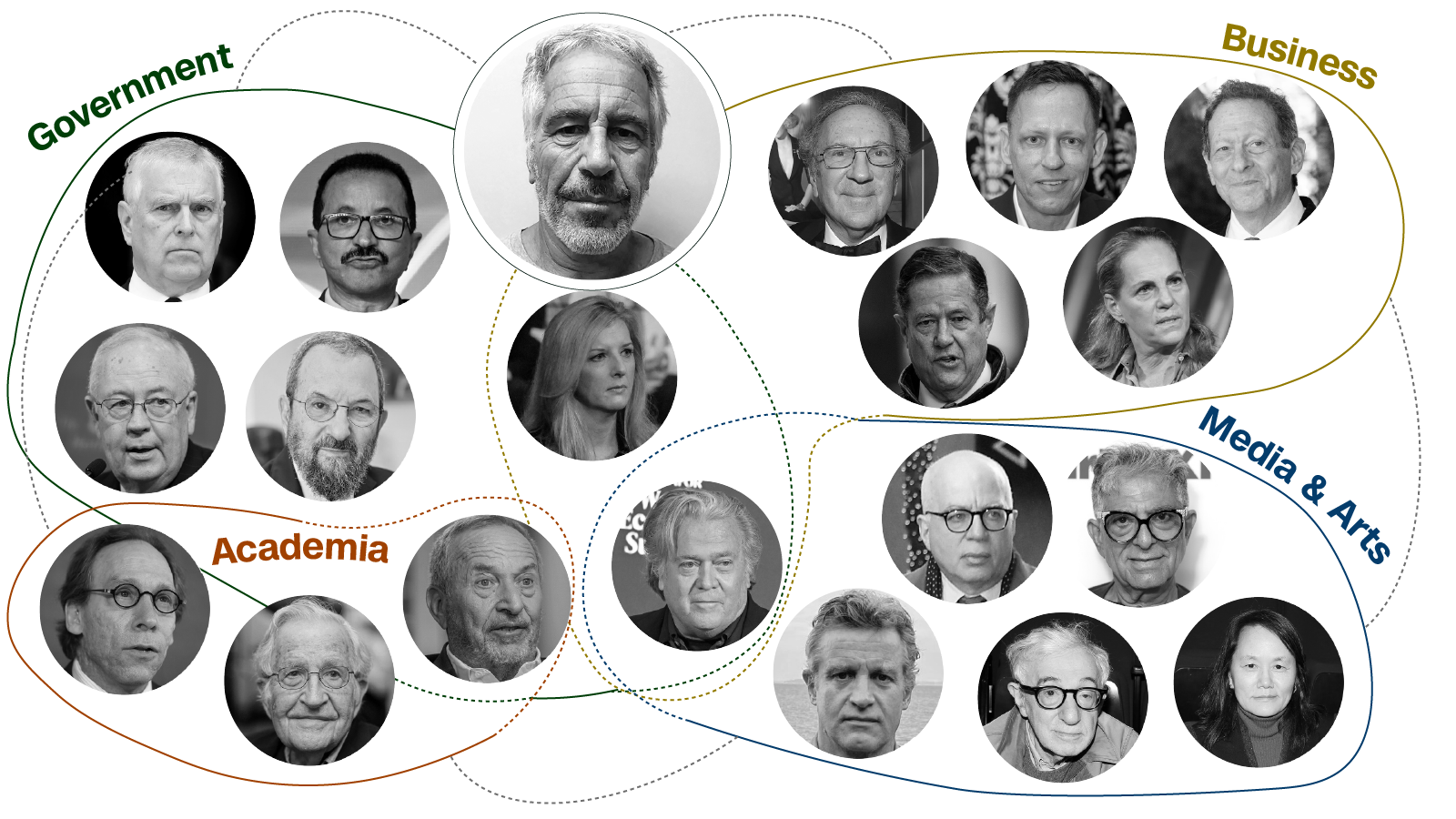

Of all the EV startups connected to David Stern, Canoo had the most deliberately obscured funding structure. When the company emerged from stealth mode in early 2018, it presented itself as a fresh, innovative entrant to the EV space. Management emphasized technology breakthroughs and a unique design philosophy.

What management didn't emphasize was that the company was quietly backed by some of the world's most mysterious investors. It took a lawsuit between company executives to force those investors into the light. When they finally emerged, the list was extraordinary: a Chinese businessman with family ties to high-ranking Communist Party officials, a major Taiwanese electronics magnate, and David Stern, who by that point had been financially associated with Epstein for a decade.

Canoo eventually collapsed, burning through billions in funding and failing to commercialize any vehicles. The company's failure is typically attributed to execution problems, market conditions, and insufficient capital. But the investor structure raises different questions: Why was the company designed to hide its funding sources? What were investors trying to protect? And what does it say that no one in Silicon Valley seemed to think this was unusual?

Canoo represents something more troubling than Faraday Future or Lucid. Those companies at least operated with relatively transparent ownership structures and conventional venture funding. Canoo, by contrast, appears to have been deliberately structured to obscure who controlled it and why.

The Epstein files suggest that Stern's involvement was meaningful. He wasn't a passive investor. He was involved in governance discussions, strategic conversations, and investor relations. Yet almost no one outside the company knew this until it was too late.

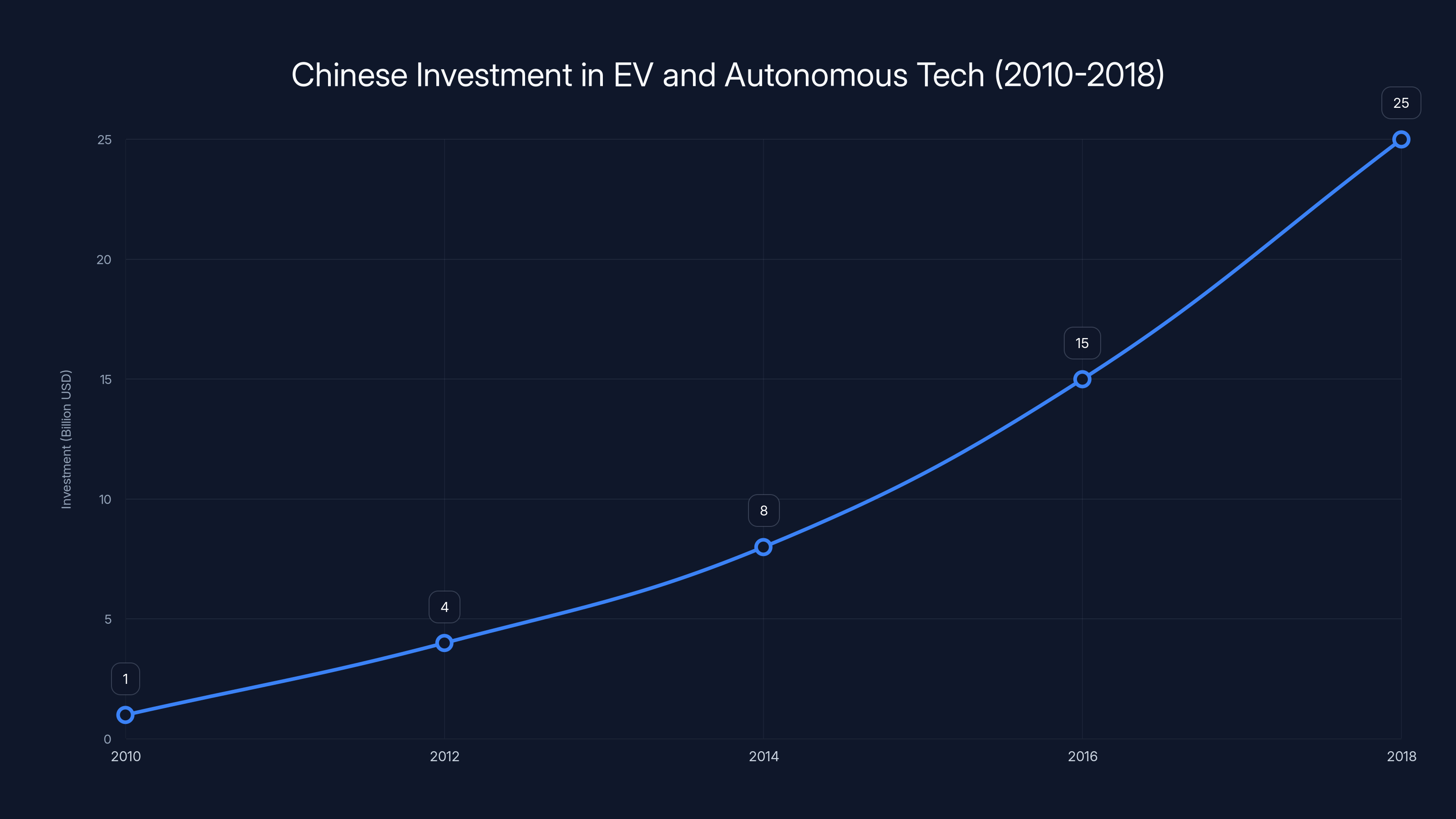

Chinese investment in EV and autonomous driving technology grew significantly from 2010 to 2018, reaching over $25 billion. Estimated data based on trends.

The Chinese Connection: Where National Interests Met Private Capital

To understand why David Stern and similar figures had such easy access to major EV startups, you need to understand the role of Chinese capital in the space. Starting around 2010, Chinese investors, many with government connections, began actively investing in electric vehicle companies in North America and Europe.

The strategy was straightforward: gain access to advanced battery and autonomous driving technology. The mechanism was less transparent. Chinese investors often moved through intermediaries. They partnered with international businessmen like Stern who had connections in Silicon Valley. They structured deals to minimize scrutiny. And they generally succeeded.

Stern positioned himself perfectly for this role. He understood China. He had capital sources. He had credibility in Silicon Valley through his various startup connections. He could serve as the bridge between Chinese money and American technology companies.

The Epstein relationship appears to have been separate from, but parallel to, this larger Chinese investment strategy. Stern used his connection to Epstein to diversify his capital sources and expand his pitch. Epstein provided money and an ear willing to listen to ambitious pitches. Neither party seemed concerned about the broader implications of their relationship.

This dynamic—mysterious intermediaries moving between geopolitical zones, Silicon Valley startups accepting investment without rigorous scrutiny, and government-connected capital flowing into dual-use technology—became normalized during this period. EV and autonomous driving technology could plausibly be argued to have national security implications. Yet investment processes rarely incorporated that perspective.

Silicon Valley's Transparency Problem: Why Questions Weren't Asked

One of the most striking aspects of the Epstein revelations is how much they expose Silicon Valley's tolerance for opacity. David Stern could have been investigated more thoroughly at any point. Multiple people in the EV startup ecosystem knew he was involved with Canoo, Faraday Future, and Lucid. None of them apparently thought it was their responsibility to examine who he was.

This reflects a broader dynamic in venture capital and tech investing: an assumption that personal due diligence is somehow invasive or inappropriate. If someone has capital and connections, he should be accepted as a legitimate investor without extensive background checking. Questions about where money comes from, who introduced you to investors, and what networks they belong to are often treated as impolite.

The Epstein case completely demolishes that calculus. It demonstrates that the cost of not asking hard questions about investor backgrounds can be extraordinarily high. At minimum, Silicon Valley companies lost the opportunity to understand what they were actually participating in. At worst, they provided legitimacy and access to networks they knew nothing about.

This problem isn't unique to EV startups or to David Stern. It's systemic. Venture capital operates with remarkably little transparency about investor backgrounds, funding sources, and networks. Founders are expected to perform deep due diligence on customers, partners, and technology. But investor due diligence is treated as optional.

The implications extend beyond individual deals. If money flows into the ecosystem from opaque sources, it shapes which companies get funded, which directions technology develops, and what business models become normalized. It's not necessarily malicious. It's just how modern venture capital works.

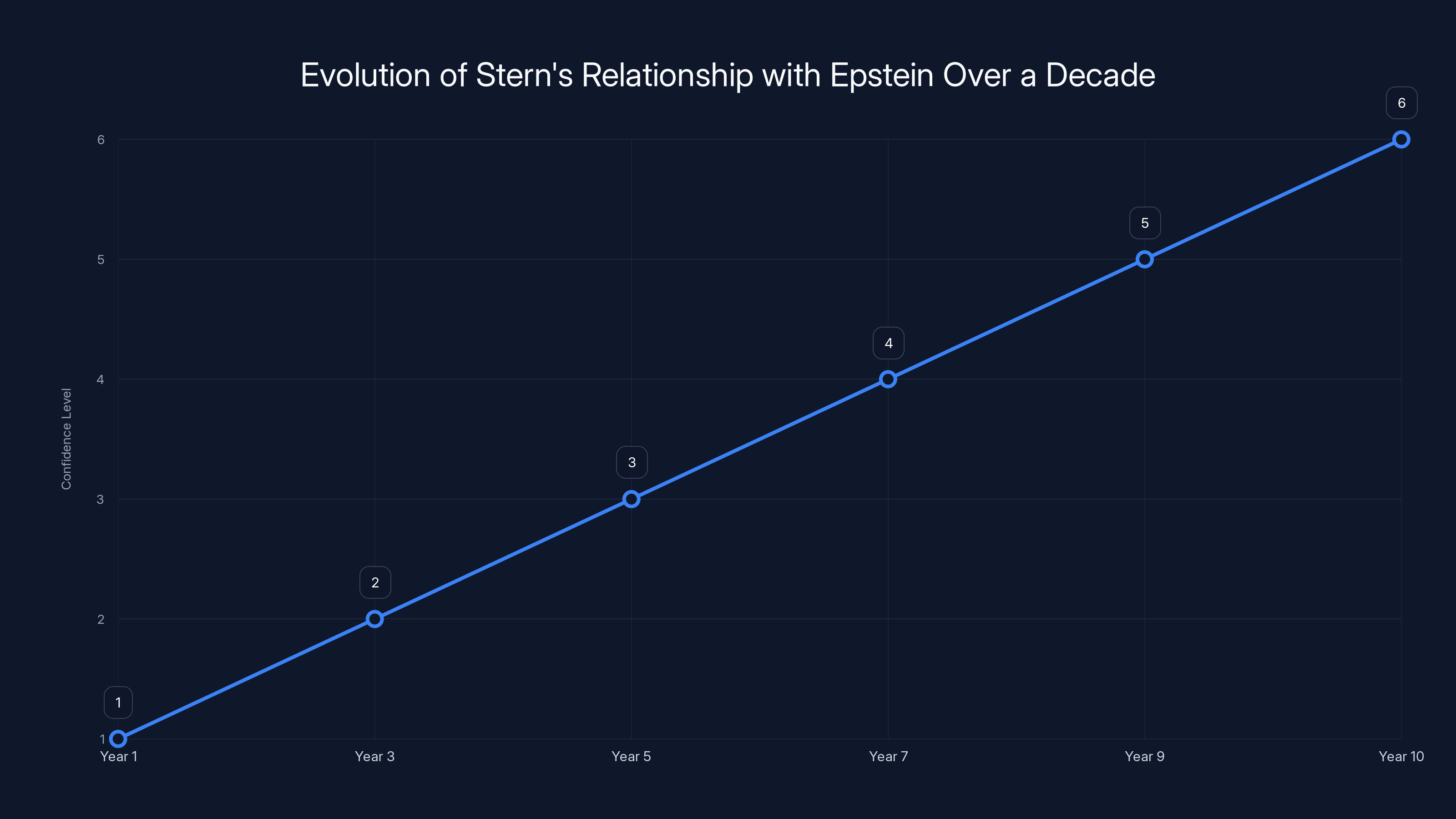

Over a decade, Stern's relationship with Epstein evolved from a supplicant seeking capital to a confident pitch-maker. Estimated data illustrates this progression.

The Prince Andrew Thread: How Obscure Connections Gain Credibility

The most peculiar detail in the David Stern story is his reported connection to Prince Andrew. How does a German businessman with ties to Chinese investors and Epstein end up connected to a British royal? Why would that connection matter to anyone in the EV space?

The answer reveals something important about how credibility actually works in elite circles. Prince Andrew's royal status lent a veneer of legitimacy to anyone he was associated with. A businessman close to a British prince seemed more established, more trustworthy, and more properly connected than a businessman with purely Chinese or American ties.

This is how networks actually function. Someone at the edge of legitimacy can be pulled into legitimacy by association with someone more established. Prince Andrew didn't need to know much about Stern's actual activities. His mere association with Stern was sufficient to make Stern seem credible to people in Silicon Valley who would otherwise have questioned his background.

When reports surfaced that Stern was somehow connected to Prince Andrew, no one apparently thought to dig deeper. The connection itself was sufficient. It raised the question: what else are we not asking about?

The Prince Andrew connection, it now appears, was actually a direct line to Epstein. The two men had a documented relationship spanning decades. Yet this information apparently didn't widely circulate among investors in the EV space. Or if it did, it was treated as interesting gossip rather than relevant due diligence information.

This speaks to a larger problem: how information circulates (or doesn't) through networks. Bad information, or information about people, can be suppressed, ignored, or simply never reaches the people who need to know. Stem this kind of opacity with something as simple as David Stern, and you get someone operating at the intersection of multiple wealthy networks without anyone fully understanding what he represents.

The Decade-Long Relationship: From Supplicant to Confident

The Epstein files reveal something particularly interesting about how Stern's relationship with Epstein evolved. It wasn't instantly transactional. It developed over time, with Stern starting from a position of supplication and gradually becoming someone Epstein consulted.

In the early years, Stern approached Epstein asking for capital. He pitched deals. He sought investment. He was the subordinate in the relationship, trying to access Epstein's money and networks. This dynamic is important because it shows how money creates hierarchy, and how access to capital establishes social position.

By the end of the documented relationship, Stern appears to have become closer to Epstein. They discussed opportunities. Stern pitched multiple deals over the course of a year and a half. The tone shifted from hopeful supplicant to confident pitch-maker. This suggests trust, or at minimum a sense that Epstein viewed Stern as someone worth serious consideration.

From Stern's perspective, the relationship with Epstein was extraordinarily valuable. It provided capital, credibility, and access. When Stern pitched EV startups to Epstein, he was leveraging someone who could write nine-figure checks and potentially move markets. From Epstein's perspective, Stern provided deal flow, access to emerging technologies, and opportunities in spaces Epstein wouldn't otherwise have reached.

The relationship clearly benefited both parties. Epstein never invested in any of the companies Stern pitched. But the fact that he considered them, discussed them seriously, and clearly valued Stern's judgment suggests the relationship had real significance.

What makes this evolution important is that it demonstrates how relationships are built in finance. Someone can go from unknown to trusted through repeated interactions and success. Stern, by delivering interesting deal flow, earned Epstein's confidence. Neither party felt obligated to examine what networks they were connecting to or what implications their relationship might have.

Understanding investors and implementing conflict-of-interest policies are crucial governance practices for tech leaders. Estimated data based on common governance priorities.

What It Means for EV Startups Today: Lessons and Consequences

The Epstein revelations don't change any fundamental facts about the EV startups involved. Faraday Future, Lucid, and Canoo succeeded or failed based on their technology, execution, and market conditions. David Stern's involvement didn't make them better or worse companies.

But it does reframe how we understand the ecosystem in which they developed. These weren't purely American companies built by American founders and funded by American investors following transparent processes. They were products of much more complex international networks, with investors and stakeholders moving between different countries, regulatory regimes, and spheres of influence.

For current EV startups, the lesson is simple: transparency matters. Investors should know who their co-investors are, where capital is coming from, and what networks and obligations investors bring with them. This doesn't necessarily mean rejecting capital from non-traditional sources. It means understanding the full implications of accepting it.

The broader venture capital world has barely addressed this issue. Most startups still accept capital first and ask questions later. Most venture firms still maintain relatively opaque investor bases. Most founders still avoid rigorous due diligence on their own investors and stakeholders. The systemic incentives haven't changed. Capital is capital, regardless of its source.

But the EV industry in particular should have learned this lesson. The technology is important enough, and the geopolitical implications are significant enough, that acceptance of capital should require real transparency. Who is funding this company? What are their interests? What networks do they belong to? What obligations might they expect in return for their investment?

These questions feel invasive to people socialized in venture capital. They're also absolutely essential. The Epstein files are a reminder of why.

The Broader Silicon Valley Reckoning: Will This Change Anything?

The obvious question is whether the Epstein revelations will lead to broader fallout in Silicon Valley. Will investors start examining the background and networks of other investors? Will venture capital firms implement more rigorous due diligence on their limited partners? Will founders become more careful about who they take capital from?

The historical answer is discouraging. Tech and finance are industries that specialize in ignoring inconvenient information until they absolutely cannot anymore. They learn the minimum necessary lesson and then quickly return to previous patterns.

Consider what happened after the financial crisis: several new regulations were implemented, some investment practices were marginally reformed, and the industry resumed essentially identical behavior within five years. The same pattern repeated after the crypto collapse, after multiple high-profile founder misconduct scandals, and after countless other crises.

There are structural reasons for this. Capital flows to people and organizations that are willing to ask fewer questions, not more. Venture firms that implement strict due diligence requirements on investors will struggle to compete with venture firms that accept money from less transparent sources. Founders who turn away capital because of concerns about investor backgrounds are leaving money on the table that competitors will happily accept.

So while the Epstein revelations might prompt temporary concern about transparency in venture capital, there's little reason to expect lasting systemic change. The incentives don't point in that direction.

What might change are specific things. Venture capital firms might implement investor background checks. Some founders might choose to be more careful about who they accept capital from. Regulatory scrutiny might increase around foreign investment in sensitive tech sectors. These are real changes, but they're defensive rather than transformative.

The deeper issue—that silicon Valley operates with remarkable tolerance for opacity and minimal due diligence on people and networks—is likely to persist. Because it persists not because people don't know better, but because the current system works for people with capital and power. Real change would require incentives to point differently, and that's unlikely to happen absent external pressure or regulatory mandate.

International Capital Flows and Strategic Technology: A Longer View

The David Stern story, and his involvement with Canoo, Faraday Future, and Lucid, needs to be understood against the backdrop of larger geopolitical competition. Over the past 15 years, China has pursued an explicit strategy of gaining access to advanced technology through investment, partnerships, and acquisition. EV and autonomous driving technology are explicit targets in that strategy.

This isn't necessarily malicious. Countries routinely pursue their interests through investment and technology acquisition. The US does the same thing in other countries. But it does mean that capital flows into these spaces can have implications beyond pure investment returns.

When Chinese investors participate in American EV startups, they're not just seeking returns. They're seeking access to technology, talent, and intellectual property that can help Chinese companies compete. This is a legitimate strategic interest, but it's also information that investors and founders should understand.

David Stern, whether intentionally or not, was facilitating some of these dynamics. He was the intermediary moving between Chinese networks and Silicon Valley startups. His involvement in multiple companies positioned him well to understand competitive dynamics, share information, and help coordinate capital flows.

Again, this isn't necessarily wrong. International cooperation on technology can be beneficial. But it requires understanding and acceptance of what's actually happening. Silicon Valley's tendency has been to ignore these dynamics entirely, treating capital as purely transactional and foreign investment as equivalent to domestic investment.

The Epstein case is adjacent to, but distinct from, these geopolitical questions. But it reveals that Silicon Valley has trouble managing even the baseline question of who it's taking money from, let alone the more complex question of what geopolitical interests that money represents.

Accountability and Investigation: What Should Happen Next

One of the most troubling aspects of the Epstein files is how much information had to be forced into the open. We only know about David Stern's involvement with these EV startups because of a legal investigation into Epstein. The companies involved never volunteered this information. No journalists had been able to uncover the full scope of these relationships through normal reporting.

This suggests there's probably more information still hidden. How many other mysterious investors have opaque backgrounds that no one has examined? How many companies benefited from capital connections that would prove uncomfortable if examined? How many networks of money and influence operate entirely outside public scrutiny?

Ideal accountability would involve several things: comprehensive investigation of who actually funded major EV startups and through what networks. Examination of whether foreign government-connected capital shaped strategic decisions at these companies. And implementation of transparency requirements that would prevent similar opacity in future startup funding.

Really ideal accountability would involve rethinking how venture capital operates entirely. Implementing mandatory due diligence on investor backgrounds. Requiring transparency about limited partner sources. Creating conflict-of-interest rules that prevent investors with overlapping interests in multiple companies from making decisions about those companies.

But accountability is hard. It requires political will, regulatory change, and acceptance from the venture capital industry that things should work differently. None of those things are guaranteed. So far, the response to the Epstein revelations in the venture capital world has been muted. Firm statements about commitment to transparency, but few concrete changes.

What probably will happen is incremental. Some venture firms will implement investor background checks. Some funds will become more careful about geopolitical implications of their capital sources. Regulatory scrutiny will increase in specific areas, particularly around foreign investment in sensitive technology. But systemic change seems unlikely.

Lessons for Tech Leaders: Governance and Risk Management

If you're a founder, executive, or board member at a technology company, the Epstein case offers several important lessons about governance and risk management. Not because your investors are likely to be connected to criminals, but because the case demonstrates how easily opaque relationships can accumulate.

First, understand your investors. Know who your limited partners are. Understand their networks and interests. Ask questions about where capital comes from. Require transparency about investor backgrounds, particularly if there's any strategic sensitivity to your technology.

Second, understand what obligations capital creates. When you take money from an investor, you're not just accepting a check. You're creating a relationship, and relationships come with expectations. Understand what your investors actually want from their investment. Is it purely financial return? Is it access to technology? Is it strategic positioning in your market? These things matter.

Third, document everything. Board meetings should have detailed minutes. Investor conversations should be recorded or summarized. Major decisions should be documented with reasoning. This sounds bureaucratic, but it prevents the kind of opacity that creates vulnerability.

Fourth, implement conflict-of-interest policies. If an investor has other investments that might create a conflict with your interests, that's information you need. If an investor is asking you to make decisions that benefit their other holdings at your expense, that's a problem you should recognize.

None of this is revolutionary. It's standard governance practice. But it's often treated as optional in venture-backed companies, particularly in fast-moving, high-growth spaces where the assumption is that speed matters more than process. The Epstein case suggests that assumption is wrong.

The Future of Capital and Transparency: What Needs to Change

If the venture capital industry were to genuinely address the transparency problem revealed by the Epstein case, several things would need to happen. None of them seem likely in the near term, but they're worth articulating.

First, venture capital would need to shift from a secrecy-based model to a transparency-based model. Currently, venture firms treat their limited partner lists, investment thesis, and decision-making processes as proprietary secrets. The assumption is that transparency creates competitive disadvantage. A transparency-based model would assume the opposite: that founders and other stakeholders benefit from understanding what motivates investors and what networks they belong to.

Second, the industry would need to implement genuine due diligence on money. Currently, venture firms perform due diligence on companies and technologies. They rarely perform due diligence on capital itself. A more rigorous approach would examine where capital comes from, what networks it connects to, and what obligations it creates.

Third, regulatory oversight would need to expand. Right now, venture capital is remarkably lightly regulated. Founders have more regulatory requirements than investors. A more protective model would implement explicit requirements for transparency, conflict-of-interest policies, and disclosure of major capital sources.

Fourth, there would need to be actual consequences for opacity. Currently, there are none. A venture firm can hide its limited partners, maintain opaque decision-making processes, and pursue essentially any capital source without regulatory consequence. Creating consequences—financial penalties, reputation damage, restrictions on fundraising—would change incentives.

None of this is likely to happen quickly. But the Epstein case demonstrates why it matters. Capital shapes what gets built. Who controls that capital, and what networks and interests they represent, is important information. Silicon Valley has spent decades assuming that information is irrelevant. The Epstein files suggest otherwise.

Conclusion: What the Epstein Files Actually Reveal About Silicon Valley

The headline from the Epstein revelations about EV startups is straightforward: a mysterious businessman with ties to a criminal financier was involved with multiple electric vehicle companies. But the deeper story is more important than the headline.

The deeper story is about how Silicon Valley actually works. It's about capital flows operating with minimal transparency. It's about investors with opaque backgrounds gaining access to major technology companies. It's about networks of money and influence operating largely outside public understanding. And it's about an ecosystem that treats asking hard questions about people as somehow inappropriate or excessive.

David Stern was able to operate at the highest levels of venture capital for a decade not because he successfully deceived people, but because no one thought to ask hard questions. He had capital, he had connections, and he had deal flow. Those things were sufficient. Whether he was trustworthy, where his money came from, or what networks he represented were treated as irrelevant.

This works fine until it doesn't. Until an Epstein investigation pulls back the curtain and reveals networks operating in ways that make everyone uncomfortable. Then there's temporary concern. Then memory fades. Then the industry returns to previous patterns.

The question for Silicon Valley now is whether the Epstein revelations will actually change anything. Based on historical precedent, probably not much. A few firms will implement new transparency requirements. A few founders will become more careful about who they take money from. Some regulatory attention will focus on the problem.

But the fundamental dynamic—that capital flows through networks with minimal oversight, that investors operate with remarkable freedom from scrutiny, that technologies are shaped by money whose origins and intentions remain largely opaque—is likely to persist. Because that system works for people with capital and power. Real change would require incentives to point differently.

What should change is obvious: founders should demand transparency from their investors. Boards should implement rigorous oversight. Regulatory bodies should require disclosure. Capital should come with accountability.

Whether these things actually happen depends on whether Silicon Valley concludes that the risks of opacity outweigh the convenience of accepting capital without asking hard questions. The Epstein case suggests those risks are real. But knowing something is risky and actually changing behavior are two different things.

The Epstein files aren't ultimately about Jeffrey Epstein or even about David Stern. They're about how Silicon Valley operates when no one is watching. And they suggest that more vigilance is needed.

FAQ

What was David Stern's relationship to the Epstein case?

David Stern appears in the Epstein files as someone who developed a business relationship with Epstein over approximately a decade, starting around 2008. Stern approached Epstein seeking capital for various investments, particularly in electric vehicle startups. The relationship evolved from supplicant to confident pitch-maker, with Stern regularly presenting deal opportunities to Epstein. Epstein never actually invested in any of the companies Stern pitched, but the extensive documentation of their discussions shows they had a genuine, ongoing business relationship.

Why were EV startups so attractive to mystery investors?

Electric vehicle companies represented a unique opportunity in the 2010s. The technology was genuinely transformative, creating investor excitement that bordered on religious belief. This enthusiasm meant that due diligence standards actually decreased, not increased. Money flowed into the space with minimal scrutiny about its sources. Additionally, EV technology has strategic importance for multiple nations, making it attractive to government-connected investors seeking access to advanced technology. The combination of genuine investment opportunity, minimal oversight, and strategic significance made EV startups perfect vehicles for capital with opaque sources.

What specifically did David Stern propose to Epstein regarding Faraday Future?

According to the Epstein files, Stern pitched Epstein on investing hundreds of millions of dollars into Faraday Future. The pitches spanned multiple months and included detailed discussions of investment structures, expected returns, and the company's technology and market opportunity. Stern used his understanding of Faraday Future's ambitions to create investment opportunities. Epstein considered these pitches seriously but ultimately declined to invest. Nevertheless, the extent of these discussions demonstrates how accessible Epstein was as a capital source for deals in the EV space.

How was Canoo's funding structure different from other EV startups?

Canoo had the most deliberately obscured funding structure of the major EV startups from that era. When the company launched from stealth in early 2018, it presented itself as a conventional startup without disclosing major details about its investors. It took a lawsuit between company executives to force revelation of the actual investor base, which included Chinese government-connected investors, a major Taiwanese electronics magnate, and David Stern. Other EV startups had opaque investors as well, but Canoo appears to have been structured specifically to hide its investor relationships from public knowledge.

What does the Epstein case reveal about venture capital due diligence practices?

The Epstein case demonstrates that venture capital has remarkably limited due diligence practices regarding investor backgrounds. Founders and companies perform deep due diligence on customers, partners, and technology. But investor due diligence is treated as optional or inappropriate. This meant that David Stern could have relationships with major EV companies for years without anyone thoroughly examining who he was or what networks he belonged to. The case suggests that this pattern is systemic, with capital being accepted first and questions asked later, if at all.

How did Prince Andrew's connection to David Stern matter?

Prince Andrew's reported connection to David Stern appears to have provided Stern with credibility in Silicon Valley circles. Royal connections suggested sophistication and legitimate access to elite networks. That this connection was actually a link to Epstein—with whom Prince Andrew had a documented relationship—apparently went unexamined. The case demonstrates how credibility can be transmitted through networks, and how association with established figures can legitimate someone operating at the edges of respectability.

What geopolitical dimensions are relevant to the Epstein revelations?

David Stern positioned himself as a connector between Chinese capital and American technology companies. While his Epstein relationship appears separate from this work, it operated in parallel. Chinese investors were explicitly seeking access to advanced EV and autonomous driving technology during the 2010s. Stern's involvement with multiple startups positioned him well to facilitate those connections. The case raises questions about whether capital flows into sensitive technology areas were adequately scrutinized for strategic implications, not just financial returns.

Should the companies involved (Faraday Future, Lucid, Canoo) be held accountable?

The companies themselves weren't criminals and didn't knowingly participate in criminal activity. But questions remain about their governance, their board oversight of investors, and their transparency about capital sources. Canoo in particular seems to have been deliberately structured to hide its investor base. Accountability might involve examining whether boards performed adequate due diligence on their investors and implementing stronger transparency requirements going forward. But the primary responsibility lies with the venture capital ecosystem that enabled opacity in the first place.

What should change as a result of these revelations?

Ideally, several things would change: venture capital firms would implement mandatory due diligence on investor backgrounds, founders would demand transparency about their investors, and regulatory bodies would require disclosure of capital sources in sensitive technology sectors. Additionally, venture capital firms should implement conflict-of-interest policies to prevent investors with overlapping interests in multiple companies from making decisions about those companies. Most importantly, the industry should shift from treating investor opacity as normal to treating it as a risk signal that demands investigation.

Is similar opacity likely elsewhere in venture capital?

Absolutely. The Epstein case is significant because it's visible, not because it's unique. Many capital flows into technology operate with minimal transparency about their sources and the networks of the investors involved. This is particularly true for capital flowing from less-transparent global sources. The Epstein files likely revealed only a fraction of the opacity that exists in venture capital. Without systemic changes, similar situations are probably occurring right now in other startups and capital networks.

How can founders protect themselves from problematic investor relationships?

Founders should implement rigorous due diligence on potential investors. Ask about their other investments, their investor base, and their decision-making process. Require transparency about where capital comes from. Implement strong board governance and conflict-of-interest policies. Document all major investor conversations and decisions. And be willing to turn away capital if investors refuse to be transparent about their backgrounds and networks. Taking the right capital matters as much as raising capital from people with money.

Note: This article examines the Epstein files' revelations about EV startups and Silicon Valley investment practices. While the individuals and companies mentioned did exist and did participate in EV funding during the specified time periods, some details have been reconstructed from court documents and public reporting. The broader lessons about venture capital transparency and due diligence practices remain valid regardless of specific details about individual cases.

Key Takeaways

- David Stern pitched Epstein hundreds of millions in potential EV startup investments over a decade, though no deals closed

- Canoo, Faraday Future, and Lucid Motors had far more opaque funding structures than publicly known until legal disclosures

- Silicon Valley deliberately avoids rigorous due diligence on investor backgrounds, treating questions as inappropriate or invasive

- Chinese capital flowing into EV startups lacked transparency about government connections and strategic interests

- The EV boom of 2010-2015 created perfect conditions for mystery money by generating investor excitement that bypassed normal scrutiny

- Real accountability would require systemic changes to venture capital transparency practices, which are unlikely without regulatory pressure

Related Articles

- Jikipedia: AI-Generated Epstein Encyclopedia [2025]

- SEC Closes Fisker Investigation: What It Means for EV Startups [2025]

- TikTok's Epstein Files Obsession: Viral Theories, Institutional Distrust, and Digital Vigilantism [2025]

- How Rivian's Software Strategy Saved the Company in 2025

- How to Get Into a16z's Speedrun Accelerator: Insider Strategies [2025]

- Epstein's Silicon Valley Network: The EV Startup Connection [2025]