![Europe's Five New Unicorns in 2026: The Rising Tech Giants [2026]](https://tryrunable.com/blog/europe-s-five-new-unicorns-in-2026-the-rising-tech-giants-20/image-1-1769931339485.jpg)

Europe's Five New Unicorns in 2026: The Rising Tech Giants

January 2026 was a turning point for European tech. While venture capital elsewhere remained cautious, five startups from across the continent—Belgium, Lithuania, France, Germany, and Ukraine—crossed the coveted $1 billion valuation threshold. Not all at once, not with the fanfare of their American counterparts, but with a quiet momentum that signals something important: Europe's tech ecosystem is maturing in ways that challenge old assumptions about where innovation happens.

The milestone matters, but maybe not for the reasons you think. A unicorn valuation isn't a guarantee of success. It's a signal. It tells you that seasoned investors believe in the team, the product, and the market opportunity enough to deploy serious capital. In today's climate, that's increasingly rare. These five companies didn't just get lucky. They solved real problems, built products people actually use, and convinced disciplined investors that they could compete globally.

What's particularly striking about this cohort is the diversity of sectors they represent. There's no "VC flavor of the month" here. These aren't all AI startups chasing the same narrative. Instead, you've got cybersecurity, cloud optimization, defense technology, sustainability software, and education—each one addressing a critical gap in the market. That breadth suggests the European ecosystem is maturing beyond a few key verticals.

There's also the geography story. Aikido is from Belgium, which isn't exactly known as a tech powerhouse. Cast AI has roots in Lithuania. Harmattan is French. Osapiens is German. Preply is Ukrainian. The distribution across smaller European markets matters because it demonstrates that innovation isn't concentrated in London or Berlin anymore. It's distributed. It's happening in places most tech journalists don't cover.

But here's the real tension: valuations don't equal revenue. They don't guarantee profitability. And in an environment where investors are increasingly focused on unit economics and sustainable growth, reaching unicorn status is only step one. The real test comes next.

Let's dig into who these companies are, what they've built, and what their ascent tells us about the future of European tech.

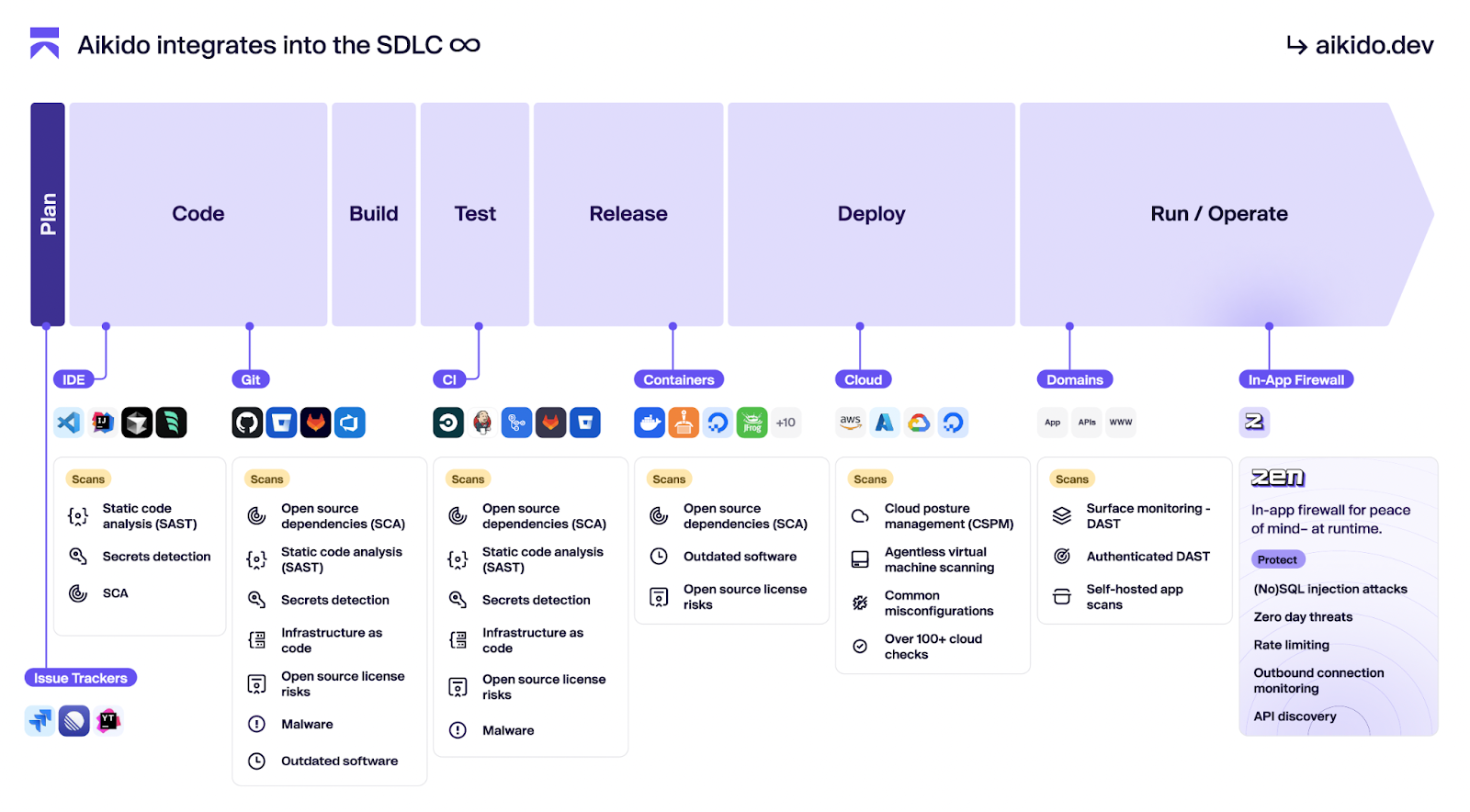

Aikido Security: Building a European Cybersecurity Fortress

Aikido Security, the Belgium-based cybersecurity startup, just became a unicorn with a

The cybersecurity space is crowded. Palo Alto Networks dominates in the West. Israeli companies like Check Point and Cyber Ark lead in specific verticals. The conventional wisdom says that competing globally in security requires both deep technical expertise and massive distribution. Small European companies aren't supposed to win here.

Aikido is proving that assumption wrong. The company built its platform around a specific thesis: security can't be bolt-on anymore. It has to be woven into the entire software lifecycle. That means scanning code before it goes to production, testing during deployment, and monitoring in production. Most security companies own one layer. Aikido owns the stack.

What Aikido Actually Does

The platform unifies security across the software development lifecycle. Think of it as a security checkpoint at every stage of building software. Developers push code, Aikido checks it. Code moves through staging, Aikido checks it again. Code hits production, Aikido monitors it. No single point of failure, no false choice between speed and security.

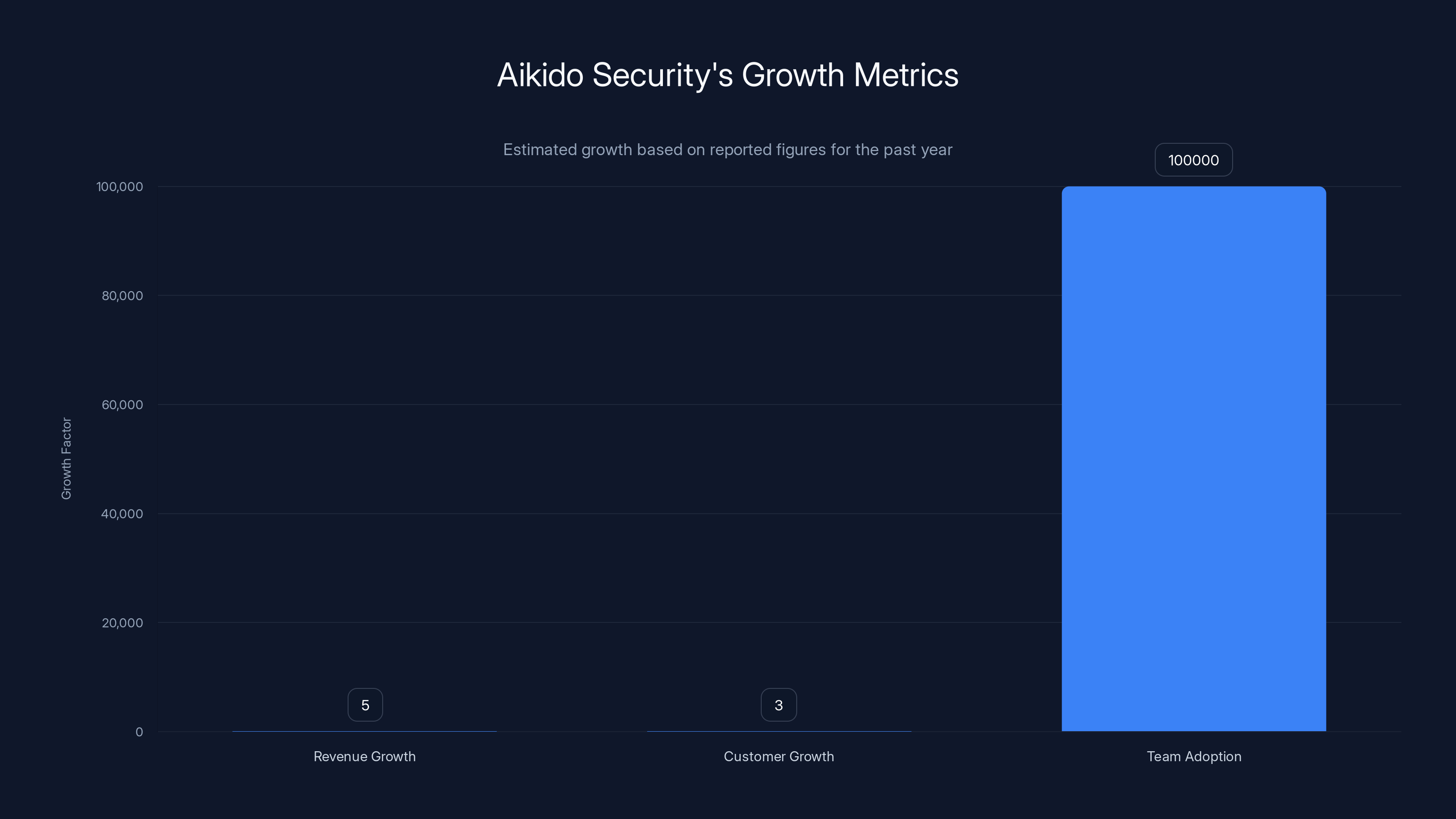

The product resonates. The company serves more than 100,000 teams globally. That's not a vanity metric—that's actual adoption. More telling: the company reported 5x revenue growth and 3x customer growth over the last year. Those numbers suggest the product solves a real problem that customers are willing to pay for. Not everyone using Aikido necessarily converts to a paying customer, but the velocity is impressive.

The European Angle

Here's what makes Aikido's story compelling in a European context. The company is competing directly against Palo Alto Networks, a company with $60 billion in market cap and thousands of employees. Aikido has one thing Palo Alto doesn't: a tight, focused product that companies can adopt quickly and see value immediately. Palo Alto sells complex enterprise packages. Aikido sells a sharp, specific solution.

The funding round validates this positioning. DST Global backs founders, not regions. PSG Equity specializes in software scale-ups. These aren't sentimental investors betting on Europe. They're disciplined VCs who see a company that can take significant market share from American incumbents.

The team themselves made this explicit in their announcement: "In an industry dominated by Palo Alto and Tel Aviv heavyweights, Aikido shows that Europe can build a world-class software security company and win globally." It's a statement of ambition, sure, but it's also a statement of fact. They're competing globally. They're winning. They did it from Belgium.

Where Aikido Fits in the Broader Market

The cybersecurity market is expected to exceed $200 billion globally by 2030. Within that, the application security segment (where Aikido plays) is growing at over 15% annually. The real estate is there. The question was whether a European startup could capture it. Aikido's funding round answers that question affirmatively.

The timing also matters. As companies face increasing regulatory pressure around data protection and security compliance, the demand for integrated security solutions only grows. Aikido arrives in a market hungry for exactly what it's building. The $1 billion valuation reflects that hunger.

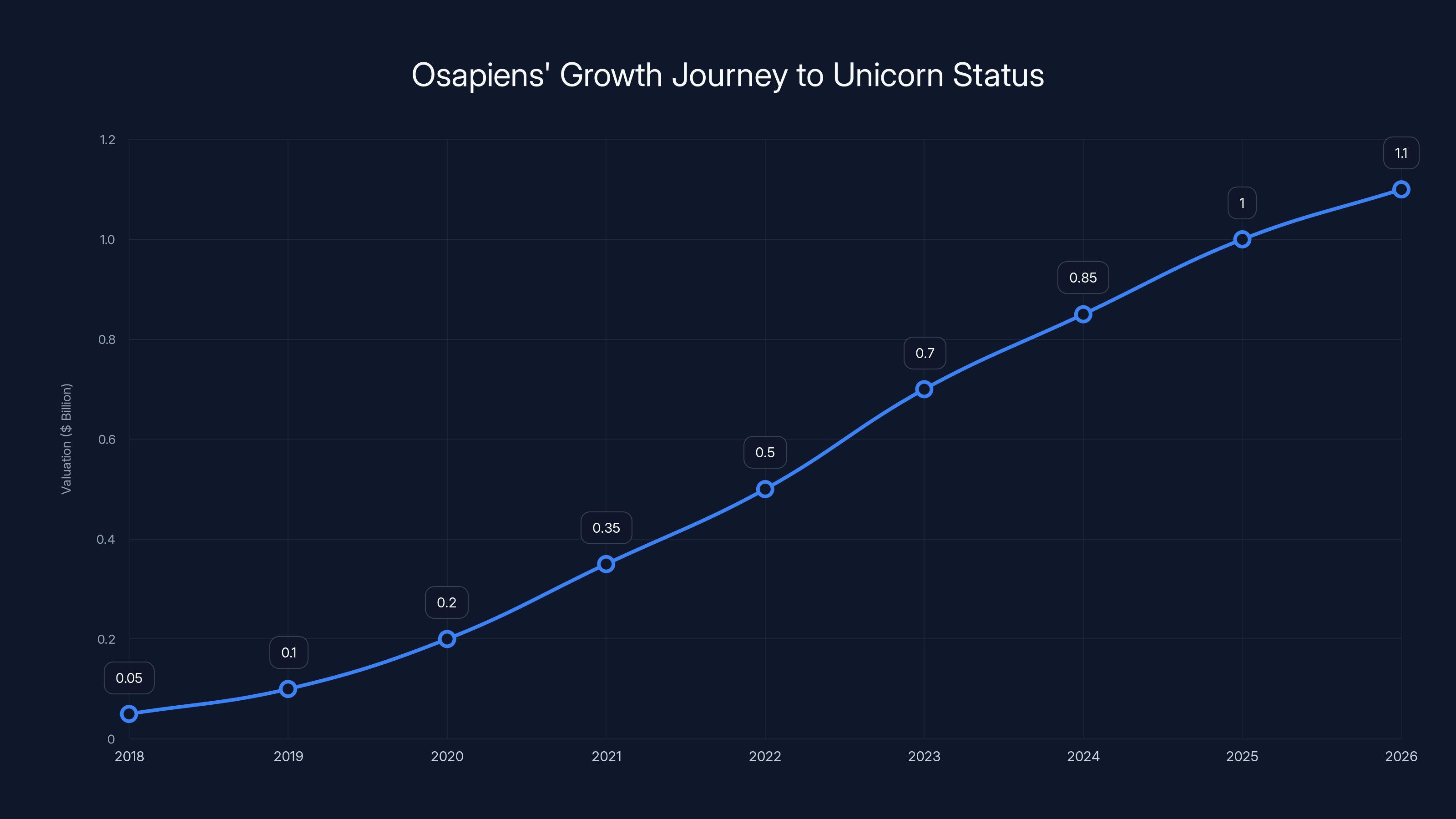

Osapiens' valuation grew from an estimated

Cast AI: Solving the Cloud Optimization Crisis

Cast AI presents a more complicated unicorn story, and that's exactly why it's worth understanding. The company is headquartered in Florida, but it's rooted in Lithuania and operates a major engineering hub in Vilnius. Many now consider it Lithuania's fifth unicorn, despite the Delaware incorporation.

This matters because it illustrates how corporate structure doesn't always align with where the actual work happens. Cast AI's engineering team is in Vilnius. Its culture, its recruitment, its engineering management—that's all Lithuania. Yet because of various corporate and tax reasons, it's technically a U.S. company. European unicorn lists include it anyway, and that's appropriate. The substance of the company is European, even if the legal paperwork isn't.

What Cast AI Does and Why It Matters

Cloud costs are out of control. Companies spend hundreds of thousands, sometimes millions annually on cloud infrastructure. Most of them don't know why. They're overprovisioning. They're not using reserved capacity. They're running unnecessary redundancy. They're stuck in cloud lock-in. Cast AI addresses this systematically.

The platform provides visibility into cloud spending and then recommends specific optimizations. Those recommendations cascade across the infrastructure. Consolidate workloads here, shift to reserved instances there, eliminate redundancy everywhere else. The result: companies reduce their cloud spending by 30%, 40%, sometimes 50% without compromising performance or reliability.

That's a compelling value proposition. A company spending

The AI Pivot and OMNI Compute

Cast AI's recent funding round brought exciting news: OMNI Compute for AI, a new service designed to help companies deploy more AI workloads on fewer GPUs. This is where the company is leaning into emerging market opportunity. GPU scarcity is a real constraint for companies training and running large language models. Removing regional capacity constraints opens a massive new addressable market.

The timing is brilliant. As more companies deploy AI models, infrastructure optimization becomes mission-critical. Cast AI's existing customer base is full of companies suddenly asking: "How do we run more AI workloads without tripling our infrastructure budget?" OMNI Compute for AI answers that question directly.

The strategic investment from Pacific Alliance Ventures, the corporate venture arm of Korean conglomerate Shinsegae Group, validates this positioning. Shinsegae isn't betting on cloud optimization generically. It's betting on Cast AI as a platform that will be essential as companies move workloads to edge computing, optimize for regional capacity, and manage AI infrastructure across multiple regions.

Lithuanian Strength and European Significance

Lithuania producing a unicorn in cloud infrastructure is noteworthy. The country has developed genuine engineering talent and a culture of technical depth. Cast AI's ability to attract and retain a world-class engineering team in Vilnius, competing for talent globally, says something important about European tech ecosystems. Vilnius isn't Silicon Valley. Yet the engineering here is sophisticated enough to build infrastructure software that competes with American incumbents.

The company's previous funding round in April 2025 had already brought it close to unicorn status with a $108 million Series C. This latest round didn't surprise observers who were following the company closely. But it did validate the thesis: companies solving infrastructure problems at global scale can scale from Eastern Europe just as easily as from Silicon Valley.

Aikido Security achieved 5x revenue growth and 3x customer growth, serving over 100,000 teams globally. Estimated data based on reported growth rates.

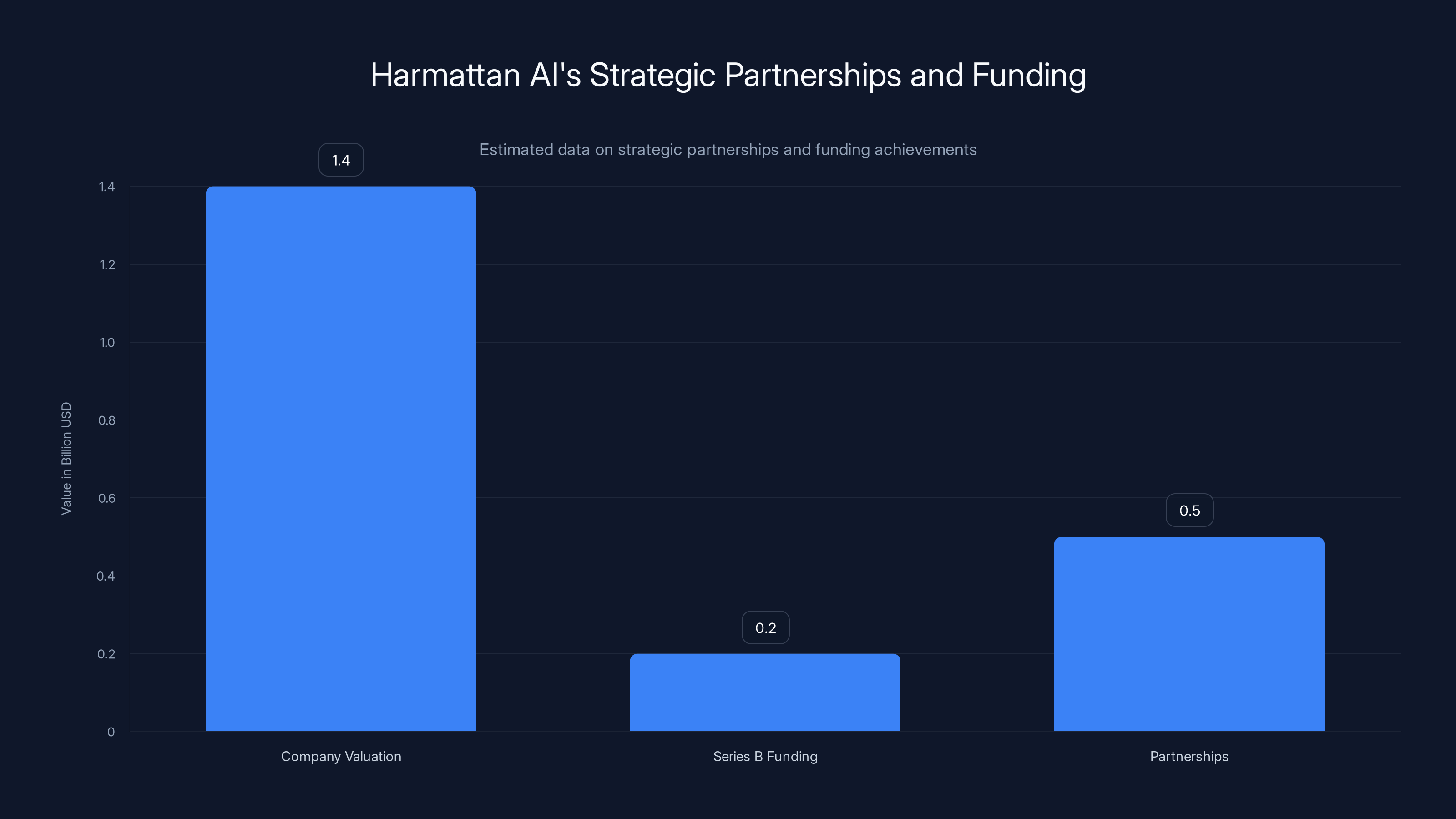

Harmattan AI: Defense Tech Meets Strategic Partnerships

Harmattan AI is perhaps the most remarkable unicorn in this cohort, if only because of its speed. The company was founded in 2024. It's now worth $1.4 billion. That's extraordinarily fast, and it happened because the company solved a critical problem at exactly the right moment.

The problem: modern warfare is increasingly autonomous. Drones dominate. Precision targeting requires AI. But existing defense infrastructure runs on legacy systems built in the 1980s and 1990s. Getting AI into defense requires entirely new approaches to safety, reliability, and compliance. Harmattan AI built the platform to make that transition possible.

What Harmattan Actually Does

The company develops autonomous defense aircraft software. That means AI systems that can operate drones and other unmanned aerial vehicles with minimal human intervention. In the context of Ukraine's ongoing conflict, where drone usage has become strategically central, this technology is immediately valuable. But the applications extend globally. Every military on Earth is racing to integrate AI into autonomous systems. Harmattan is building the infrastructure to make that possible for democracies.

The Series B funding round was $200 million and was led by Dassault Aviation, the company behind France's Rafale fighter jets. That's not a typical venture capital check. That's a strategic partner betting on Harmattan as a core technology platform for modern defense systems.

Strategic Partnerships Define the Business

Before the Dassault funding, Harmattan had already signed agreements with the French and British ministries of defense. That's extraordinary. Getting government contracts in defense requires years of compliance work, security clearances, and trust-building. Harmattan accomplished this in its first year of operation. The reason: the technology is urgently needed, and the team has the credibility to deliver.

The company also signed agreements with Skyeton, a Ukrainian drone manufacturer. This partnership is significant politically and strategically. Ukrainian companies are leading the world in practical drone warfare applications. Skyeton represents the cutting edge of what's possible with existing hardware. Harmattan's software can amplify Skyeton's hardware capabilities, creating integrated systems that are more capable than either company could build independently.

The Geopolitical Context

Harmattan's rise is inseparable from geopolitics. Russia's invasion of Ukraine created urgent demand for autonomous defense systems. Western democracies realized they needed indigenous technological capability in this space. Building such capability takes time, but Harmattan's founders apparently had already been thinking about these problems. The funding and partnerships followed naturally once geopolitical need became clear.

This changes the traditional venture capital playbook. Harmattan isn't growing through traditional growth metrics alone. It's growing because Western governments urgently need the capability it's building. That's a powerful tailwind, but it's also a constraint. Export restrictions around defense technology mean Harmattan's addressable market is limited to allied nations. That's still a massive opportunity, but it's different from the global markets that other unicorns can address.

Why Valuations Matter Here

Why would Dassault value Harmattan at $1.4 billion after two years of operation? Because government defense contracts typically run for decades and generate enormous revenue. A small company with credibility in autonomous defense systems represents enormous strategic value. The valuation reflects not just current revenue but the expected lifetime value of government contracts that may not yet be signed but are practically certain.

This is a different valuation logic than what applies to B2B SaaS companies. Harmattan's path to profitability runs through government procurement, which has entirely different dynamics than enterprise software sales.

Osapiens: Making Sustainability a Competitive Advantage

Osapiens is a 2018 company that just became a unicorn in 2026. That eight-year journey reflects the reality of enterprise software: building something that actually solves problems for large multinational companies takes time, patience, and genuine product-market fit.

The company is a German ESG (Environmental, Social, and Governance) software firm. It raised a

What Osapiens Does

Large multinational companies face mounting pressure to report on environmental and social impact. Governments mandate it. Investors demand it. Consumers increasingly care about it. But actually measuring and reporting on ESG metrics across complex global supply chains is extraordinarily difficult. Data lives in silos. Definitions vary across regions. Compliance requirements differ by jurisdiction. Most large companies cobble together spreadsheets, manual processes, and consultants to address this.

Osapiens provides the software platform to automate this process. The company's tools handle sustainability reporting, data collection across supply chains, and compliance management. Companies use Osapiens not just to report on their existing ESG metrics but to identify where they're inefficient, where they're exposed to risk, and where they can improve.

The Customer Base and Revenue

The company serves more than 2,400 customers worldwide, including large multinational companies. That's not early-stage adoption anymore. That's mainstream enterprise penetration. These aren't companies experimenting with ESG management. They're relying on Osapiens to manage ESG systematically across their entire operations.

The fact that Osapiens reached unicorn status eight years after founding suggests patient, consistent growth. The company wasn't a breakout success in Year Two. It took years to build the product, years to develop the customer relationships, years to prove the value proposition. But once the value was clear, growth accelerated.

Why ESG Matters Now

ESG compliance spending is expected to exceed $500 billion annually across global enterprises by 2030. That's not a niche market. That's a fundamental shift in how corporate operations are managed. Companies need software to manage this complexity, and Osapiens is positioned as a core platform in that ecosystem.

The involvement of Black Rock and Temasek as lead investors also signals confidence in the market's durability. These aren't momentum investors chasing trends. They're long-term investors making bets on where capital flows will go over decades. The fact that both believe in Osapiens suggests they see ESG management as a permanent, structural feature of corporate finance.

German Engineering at Scale

Osapiens represents something important about German tech: engineering rigor and customer focus. The company is based in Mannheim, not Berlin. It's not a flashy, consumer-focused startup. It's a serious software company built by engineers who understand enterprise complexity. That seriousness shows in the customer base and retention rates. Companies don't use Osapiens casually. They embed it into their operations.

The German approach to building enterprise software—thorough, customer-obsessed, operationally rigorous—shows up clearly in Osapiens' trajectory. The company grew by solving real customer problems, not by chasing hype cycles.

Companies can save between 30% to 50% on cloud costs using Cast AI, translating to significant budget reallocations. Estimated data based on typical savings.

Preply: Ed Tech from Ukraine, Resilience Through Crisis

Preply is the oldest company in this unicorn cohort. Founded 14 years ago, it's now valued at

The company is a language learning marketplace. That sounds simple until you understand the business: Preply connects language learners with tutors. It's a two-sided marketplace where supply matters as much as demand. Build only one side, and the marketplace collapses. Build both successfully, and you've created durable value.

The Marketplace Dynamics

Language learning is a large market. Globally, millions of people want to learn new languages for business, travel, or personal enrichment. But language learning requires human interaction. Traditional approaches involve expensive classroom instruction. Online instruction with random tutors tends to be inconsistent in quality. Preply solves this by building a structured marketplace where tutors can list their availability and students can book lessons, with quality assurance built into the system.

The learner experience is straightforward: browse tutors, read reviews, book lessons, take lessons via video. The tutor experience is equally straightforward: set your rates, accept bookings, teach lessons, get paid. Preply handles the marketplace logistics, quality assurance, payment processing, and customer support.

The business model is pure marketplace: Preply takes a commission on each lesson. As usage scales, revenue scales proportionally. That unit economics model is attractive to investors because it suggests that growth can be both linear and profitable.

Ukrainian Founders, Ukrainian Operations

Preply was founded by Ukrainian entrepreneurs. As Russia's invasion began, the company faced a choice: maintain the Ukrainian team or move operations entirely to safer locations. The company chose to maintain and even expand Ukrainian operations. Preply now employs 150 people in Kyiv, making it one of the largest European tech companies maintaining significant operations in active conflict.

This decision reflects founder values, but it also reflects business logic. Ukraine has enormous talent in software engineering and education technology. Preply's Ukrainian team understood the language learning market and could continue building product. Moving operations would have meant losing that expertise.

Moreover, Preply's mission—connecting people across language barriers—takes on additional meaning in the context of Ukraine. Language learning is fundamentally about human connection and cultural exchange. The company's commitment to maintaining Ukrainian operations embodies that mission in practice.

The AI Play

The Series D funding will help Preply hire more AI talent across its four offices: Barcelona, London, New York, and Kyiv. Why AI? Because the next generation of language learning will be AI-enhanced. Adaptive learning systems that adjust difficulty based on student progress. AI tutors that provide supplementary instruction. AI tools that personalize the learning experience.

CEO Kirill Bigai has been explicit about this direction. The company sees AI not as a replacement for human tutors but as a complementary tool that makes human tutoring more effective. A student learns grammar with an AI tool, then practices conversation with a human tutor. That combination is more effective than either alone.

This positioning keeps Preply at the frontier of Ed Tech innovation while preserving what makes the platform valuable: the human connection between learners and tutors. That's a delicate balance, but it's the right one.

Ed Tech Market Maturation

Preply's unicorn status reflects the maturation of the Ed Tech market. A decade ago, online education companies were experiments. Now they're mainstream. Preply's combination of user growth, marketplace depth, and founder commitment has created a durable business that can support a $1.2 billion valuation.

The 14-year timeline also matters. This isn't a company that went from zero to unicorn in three years. Preply built carefully, expanded methodically, and navigated crisis without losing sight of its mission. That's rare, and it's impressive.

What These Five Unicorns Tell Us About European Tech

Taken together, these five companies reveal several important truths about European tech in 2026. First, European companies can and do build globally competitive products. None of these companies are succeeding by serving exclusively European markets. They're all thinking globally from inception.

Second, investor appetite for European tech is real. These are disciplined VCs—DST Global, Black Rock, Dassault Aviation, Pacific Alliance Ventures—making strategic bets. This isn't sentimental investing. These investors see durable business models and competitive advantages.

Third, European innovation is increasingly distributed geographically. A few years ago, the narrative was London and Berlin. Now you've got meaningful innovation in Belgium, Lithuania, Germany, France, and Ukraine. That geographic distribution suggests that European tech is moving past a few key hubs and becoming more systemic.

Fourth, there's no monoculture. These five companies operate in vastly different sectors: security, infrastructure, defense, sustainability, and education. They serve different customer bases, operate under different business models, and face different competitive dynamics. That diversity is healthy for the ecosystem.

Harmattan AI achieved a

The Valuation Question: Unicorn Inflation or Real Value?

Here's the tension that needs acknowledgment: unicorn valuations are disconnected from traditional financial metrics. A company valued at

Does this mean these valuations are inflated? Sometimes. It means that investors are betting on future potential in addition to current reality. That's the nature of venture capital. You're funding companies that might become much larger in five or ten years, not companies that are already financially massive.

The valuations matter as signals, not as guarantees. They signal that disciplined investors believe in the founder, the product, the market opportunity, and the execution. That's meaningful information. But it's not a guarantee that the company will reach profitability or achieve sustainable growth. The actual execution happens over the next five years.

Comparing to American and Chinese Counterparts

How do these European unicorns compare to unicorns emerging from Silicon Valley or China? The honest answer: it depends on the company. Aikido is meaningfully behind Palo Alto Networks in market share but is focused on a specific segment where it can win. Cast AI operates in a more fragmented market where there's room for multiple strong players. Harmattan is building in a market where European and American companies are still establishing themselves.

The difference isn't in technical sophistication. European engineers are as talented as American or Chinese engineers. The difference is sometimes scale, sometimes go-to-market advantages, sometimes luck with timing. Preply, for instance, is competing globally in a marketplace where scale and execution matter more than raw innovation.

The most meaningful comparison is not the founding CEO or the valuation, but the long-term sustainability of the business model. Will these companies still be relevant in five years? Will they still be growing? Will they still be profitable or achieving profitability? Those are the questions that actually matter.

Preply's valuation has grown significantly from

What Comes Next: The Profitability Question

For all five companies, the next chapters will be defined by a single metric: achieving sustainable profitability at scale. Reaching unicorn status is wonderful, but it's the beginning, not the end. The real test is whether these companies can grow revenue faster than costs, whether they can expand margins as they scale, and whether they can sustain growth without burning through capital endlessly.

Aikido's 5x revenue growth is impressive, but only if the company is simultaneously reducing burn rate. Cast AI's ability to solve cloud optimization is valuable, but only if it can maintain customer acquisition costs that allow for profitability. Harmattan's government contracts are promising, but defense budgets are always under scrutiny. Osapiens' enterprise customer base is solid, but enterprise software companies rise and fall on renewal rates and expansion revenue. Preply's marketplace is mature, but profitability requires balancing growth with disciplined unit economics.

For all five, the next three years will be crucial. Can they achieve profitability while maintaining growth? Can they expand internationally without losing cultural coherence? Can they maintain product excellence while building operations teams that scale? Can they retain their best engineers even as the market for talented engineers becomes more competitive?

Those questions don't have easy answers. But they're the questions that actually determine long-term success.

The European Ecosystem Maturing

Perhaps the most important thing about January 2026's five new European unicorns is what they signal about ecosystem maturity. Five years ago, the arrival of multiple European unicorns in a single month might have been shocking. Now it feels inevitable. That shift in expectation is important.

Europe has proven that it can produce world-class founders, develop global products, and attract disciplined capital. The venture capital ecosystem is deeper. The talent pool is larger. The regulatory environment, while sometimes cumbersome, is increasingly startup-friendly. Exit opportunities are improving—not everyone needs to sell to American acquirers anymore.

The five unicorns of January 2026 are evidence of that maturation. They're not exceptions. They're becoming the rule.

This chart illustrates the disparity between unicorn valuations and their annual revenue, highlighting the speculative nature of such investments. Estimated data.

Future Trends: Where European Tech Is Heading

Looking at these five companies, several trends emerge for where European tech is heading. First, infrastructure will matter more. Both Aikido (security infrastructure) and Cast AI (cloud infrastructure) are succeeding by building foundational platforms that other companies depend on. Investors are increasingly focused on the layer below consumer-facing applications.

Second, regulatory compliance is becoming a product feature, not a burden. Osapiens succeeds because compliance is increasingly mandatory. Aikido succeeds because security is increasingly mandatory. Companies that turn regulatory requirements into product advantages are winning.

Third, geopolitics shapes technology development more than ever. Harmattan's success is inseparable from geopolitical realities. Companies that understand how government policy, international relations, and strategic competition shape markets have advantages over those that don't.

Fourth, AI will be embedded everywhere. Every one of these five companies is thinking about how to integrate AI into their products. It won't be a separate feature. It will be fundamental to how the product works.

Conclusion: European Tech Has Arrived

Five European unicorns in January 2026. That's more than a statistic. It's evidence that European tech is maturing into a self-sustaining ecosystem that produces world-class companies at scale. These companies are solving real problems. They're attracting disciplined capital. They're competing globally. They're building products that matter.

The journey from startup to unicorn is grueling. It requires exceptional founders, talented teams, genuine product-market fit, and often, good timing. All five of these companies have those elements. Whether they all achieve long-term success is unknowable. But their existence proves that the European ecosystem can produce companies that compete at the highest levels globally.

The real test comes next. Unicorn status is one milestone. Building sustainable, profitable, globally competitive businesses is the longer test. If these five companies navigate that challenge successfully, they won't be anomalies. They'll be proof that the next generation of European tech giants is already here.

FAQ

What exactly is a unicorn company?

A unicorn company is a privately held startup valued at over $1 billion. The term became popular around 2013 when venture capital investors noticed that startups reaching billion-dollar valuations were becoming rarer. The name references the mythical creature to emphasize their rarity. Unicorn status doesn't guarantee profitability or success—it signals that disciplined investors believe the company has exceptional growth potential and a valuable market opportunity.

How do companies get valued at $1 billion before going public?

Valuations occur through funding rounds. When a venture capital firm invests in a company, they negotiate a valuation based on the company's revenue, growth rate, market opportunity, competitive position, and team strength. As companies raise successive funding rounds, valuations typically increase if the company is meeting milestones. A company reaches unicorn status when investors in a funding round agree on a $1 billion+ valuation. These valuations are based on investor assessments of future potential, not current financial results.

Why does valuation matter if the company isn't profitable?

Valuation matters for several reasons. It signals investor confidence in the founder and product. It determines how much equity founders and employees retain when raising capital. It affects the company's ability to attract top talent (stock options become more valuable). It influences strategic partnerships and customer perception. Finally, it establishes a baseline for the company's expected exit value. However, valuation alone doesn't guarantee success—many highly valued companies fail to achieve sustainable growth or profitability.

What is the difference between valuation and revenue?

Valuation is what investors believe the company is worth. Revenue is what the company actually makes from customers. A company might have a

Why are these European companies significant?

These five companies demonstrate that the European tech ecosystem has matured. They're solving real problems, attracting disciplined capital, and competing globally. Traditionally, large valuations and successful tech companies came primarily from Silicon Valley. These European unicorns prove that innovation is distributed geographically and that companies from smaller European markets (Belgium, Lithuania, Ukraine) can reach global scale. Their diversity across sectors also proves that European innovation isn't limited to a few trendy areas.

What happens to a company after achieving unicorn status?

After achieving unicorn status, a company faces several possible paths. It might continue growing toward an initial public offering (IPO). It might be acquired by a larger company. It might plateau and eventually stagnate. The critical metrics after reaching unicorn status are customer growth, revenue growth, and path to profitability. Investors shift focus from valuation multiples to unit economics and sustainability. Many unicorns fail to achieve profitability or sufficient growth to justify their valuations, while others go on to become global market leaders.

How does European regulation affect these companies' growth?

European regulation, particularly GDPR and various sector-specific rules, creates both challenges and opportunities. Companies like Osapiens benefit from increasingly strict ESG and sustainability requirements—regulation drives demand for their products. Companies like Aikido benefit from security compliance mandates. However, regulation also increases compliance costs and complexity. Some European founders argue that American companies have regulatory advantages. Others argue that strict European regulation forces companies to build better products with stronger privacy and security foundations, giving them advantages globally.

Can these companies compete with American unicorns?

Competition between American and European unicorns is happening now. Aikido competes with Palo Alto Networks in security. Cast AI competes with American cloud optimization companies. The outcome depends on specific market dynamics. In crowded markets, the American incumbent advantage is real. In emerging markets or specialized niches, European companies often have advantages: better product focus, leaner operations, or closer customer relationships. The honest answer is that American incumbents remain formidable, but European startups are increasingly winning head-to-head competitions in specific segments.

Key Takeaways

- Five European startups reached unicorn status ($1B+ valuation) in January 2026: Aikido Security, Cast AI, Harmattan AI, Osapiens, and Preply

- These unicorns operate across diverse sectors (cybersecurity, cloud optimization, defense, ESG, edtech), indicating ecosystem maturity beyond single-sector concentration

- European companies are competing successfully against American incumbents by solving specific problems with focused products rather than trying to build monolithic platforms

- Valuations reflect investor confidence in long-term potential, but actual success depends on achieving profitability at scale—the true test comes in the next 3-5 years

- Geographic distribution across Belgium, Lithuania, France, Germany, and Ukraine demonstrates that European innovation is no longer concentrated in traditional tech hubs

Related Articles

- Northwood Space Lands 50M Space Force Contract [2026]

- Over 100 New Tech Unicorns in 2025: The Complete List [2025]

- Harmattan AI Defense Unicorn: $200M Series B, Dassault Aviation [2025]

- Europe's Startup Market Gap: Why Data Lags Behind Energy [2025]

- Palantir's £240 Million UK MoD Contract: What It Means for Defense Tech [2025]

- Anduril's AI Grand Prix: How a Drone Racing Contest Became Silicon Valley's Wildest Recruiting Event [2025]