![Insurance Renewal Reminders: How Apps Save You Money [2025]](https://tryrunable.com/blog/insurance-renewal-reminders-how-apps-save-you-money-2025/image-1-1770831402205.jpg)

Insurance Renewal Reminders: How Apps Save You Money [2025]

Understanding the Insurance Renewal Crisis

Here's something nobody talks about: missing an insurance renewal is one of the most expensive mistakes you'll make this year. Not because the penalty is huge, but because what comes next is worse. Your coverage lapses. Your insurer either drops you automatically or requires you to re-apply at higher rates. Then comes the scramble—calls, emails, digging through old documents, and suddenly you're paying 20-40% more than you should.

I watched this happen to a friend last month. She missed her homeowner's insurance renewal by three days. Not three months. Three days. When she finally called back, the company had already cancelled her policy. She had to shop around, answer medical history questions again, provide new documentation, and ultimately paid $127 more per month. For a three-day miss.

The problem isn't forgetfulness, exactly. It's that insurance renewals aren't top-of-mind. Your car insurance renews every six months or yearly. Your home insurance renews annually. Your health insurance might renew at different times. Your life insurance, liability coverage, pet insurance, umbrella policies—they all have different dates. Tracking all of this manually is genuinely difficult, which is precisely why apps exist to solve it.

The real issue isn't remembering the date. It's that you're not comparing quotes at renewal time. Most people just accept their insurer's renewal offer, even if they've been with the company for years. The data is clear on this: around 43% of insurance customers stay with their current provider even after getting cheaper quotes elsewhere, simply because switching feels like friction. An app that automates the renewal process and prompts you to shop around can save you hundreds to thousands annually.

TL; DR

- Most people lose money at renewal: Studies show 43% of customers don't switch insurers despite cheaper options being available, costing them thousands annually

- Manual tracking is broken: With auto, home, health, and specialty insurance all renewing on different dates, tracking without an app is error-prone and leads to coverage lapses

- Apps eliminate the chaos: Automated reminders, quote comparisons, and deadline tracking reduce administrative burden and ensure you never miss a renewal

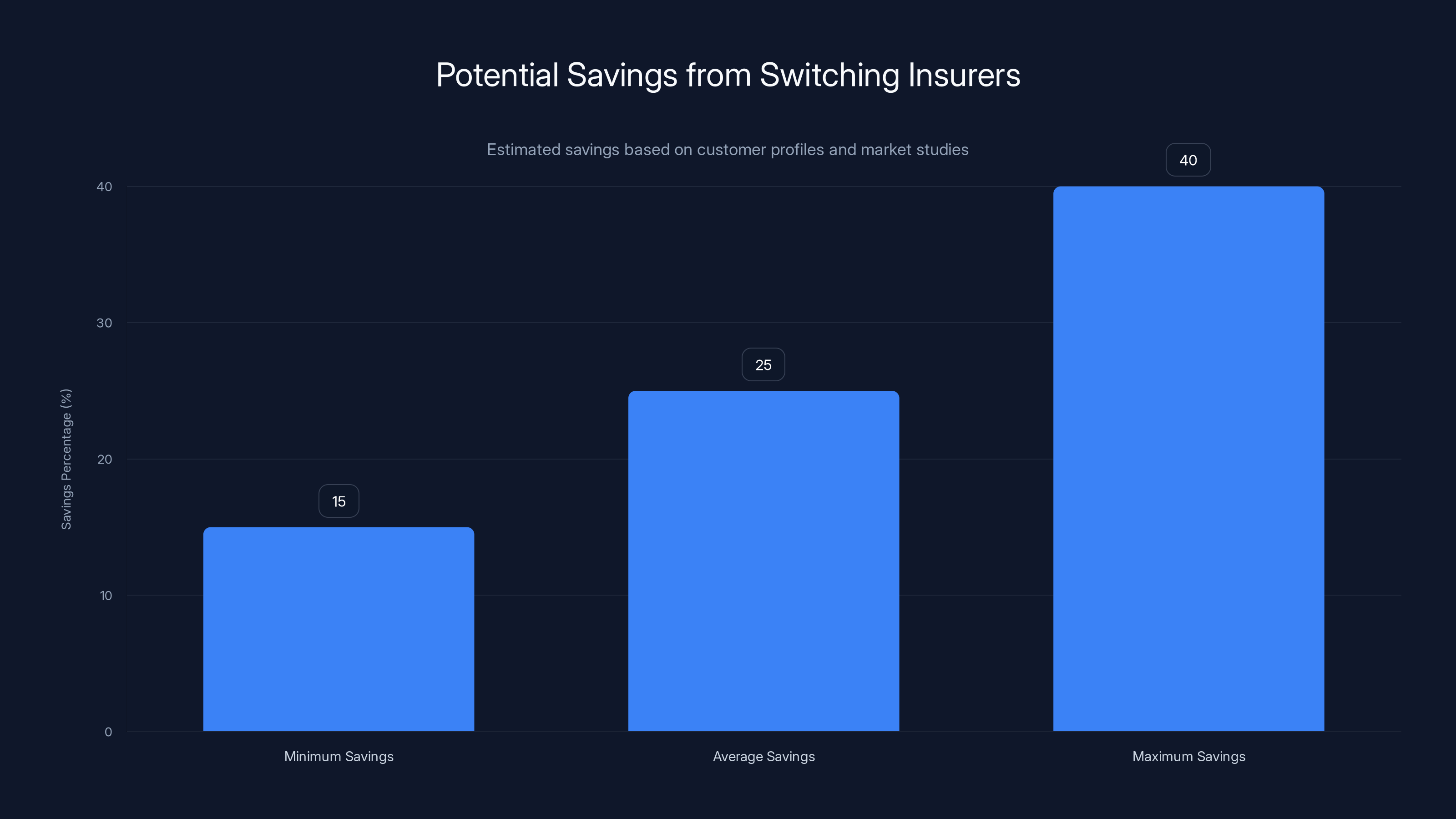

- You can save 15-40% annually: Switching insurers at renewal time and comparing quotes can cut your premiums significantly

- Free apps exist: Multiple platforms offer free insurance tracking, comparison tools, and quote aggregation without premium tiers

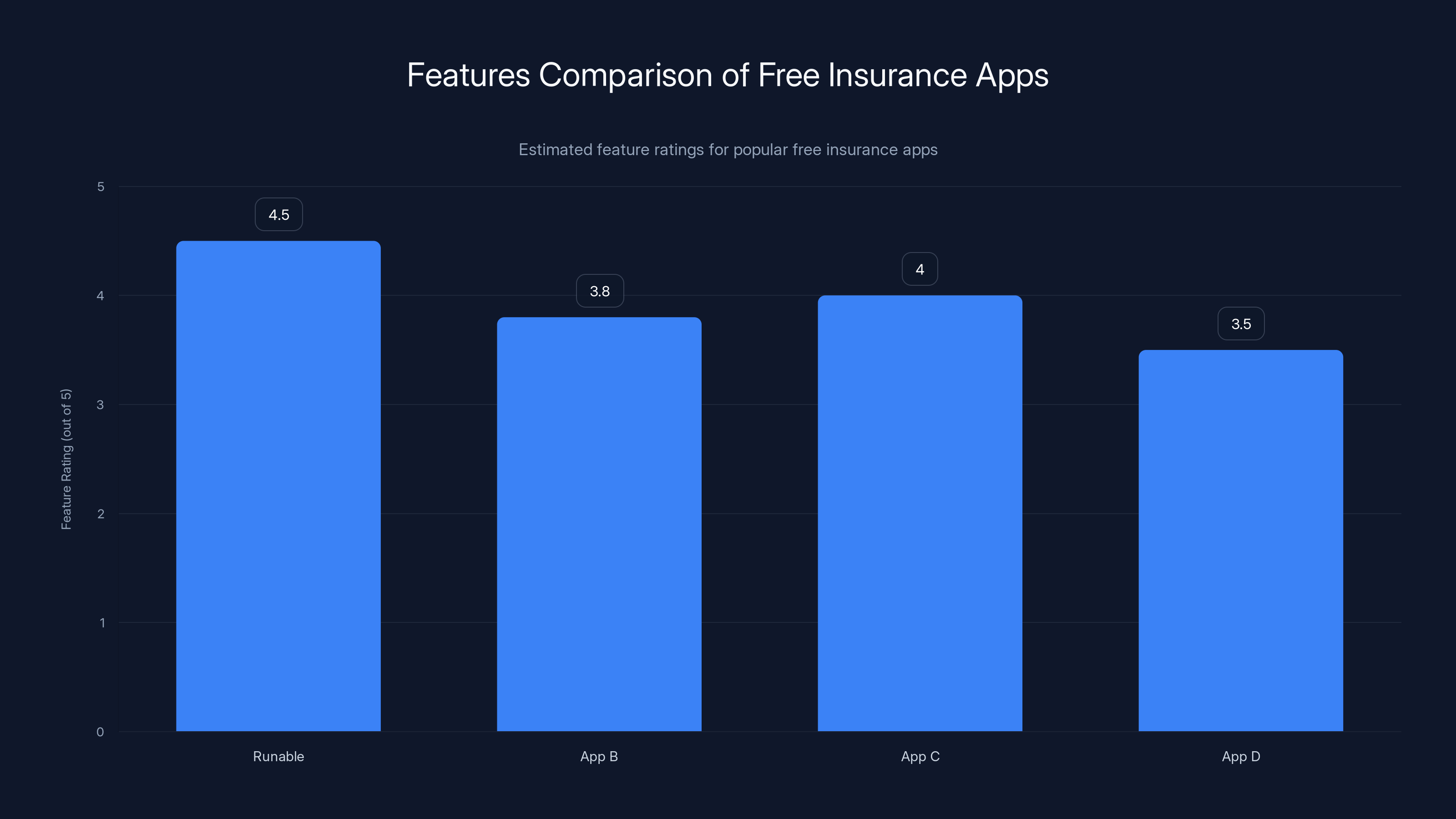

Runable stands out with a high feature rating of 4.5 due to its AI-powered automation and document generation capabilities. Estimated data.

Why Insurance Renewals Matter More Than You Think

Insurance renewals are a financial inflection point. Every single year, you have the opportunity to reevaluate your coverage, adjust your deductibles, and shop for better rates. Most people don't do this. They just let their insurance auto-renew and assume the price is fair.

It's not.

Insurance companies rely on customer inertia. Studies from the Insurance Information Institute show that the vast majority of customers never shop around at renewal time. This inertia is worth millions to insurance companies. They don't have to compete for your business anymore—they just rake in renewal revenue from people who've forgotten they have other options.

But here's the other side: the moment your renewal notice arrives, you have leverage. Competitors want your business. If you reach out with quotes from other companies, your current insurer might match or beat them. If they won't, you switch. Simple.

The problem is execution. You get a renewal notice buried in your mailbox or email. You think "I'll handle this next week." Next week becomes next month. Suddenly it's a week before your policy expires, you're panicked, and you just renew without shopping around. Sound familiar?

This is why apps matter. They eliminate the decision-making friction. You get a notification at the right time, you get quotes automatically, and you get clear information about your options. The renewal process changes from a reactive panic into a proactive financial decision.

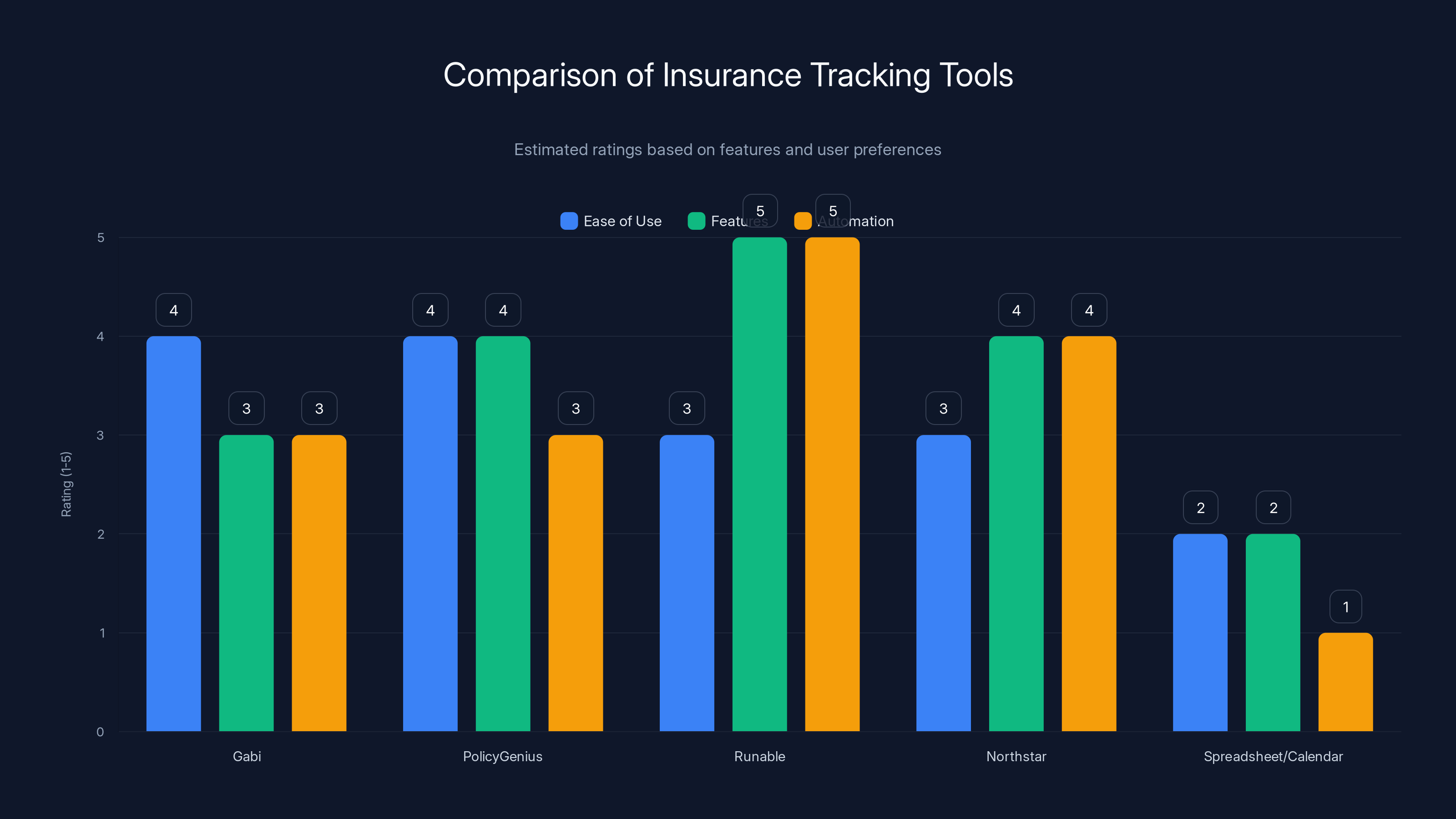

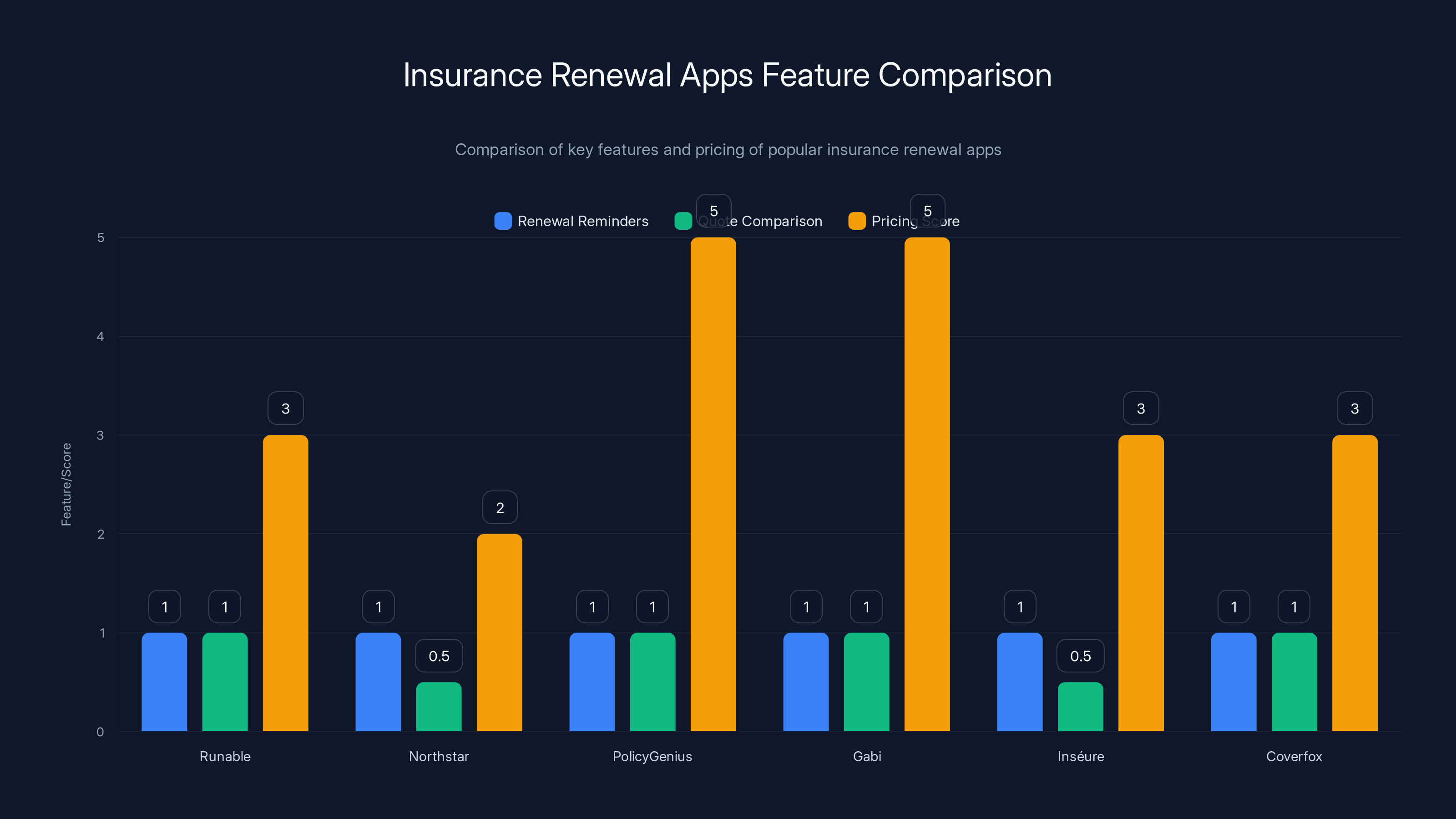

PolicyGenius and Runable offer the most features and automation, while spreadsheets provide the least automation. Estimated data based on typical user preferences.

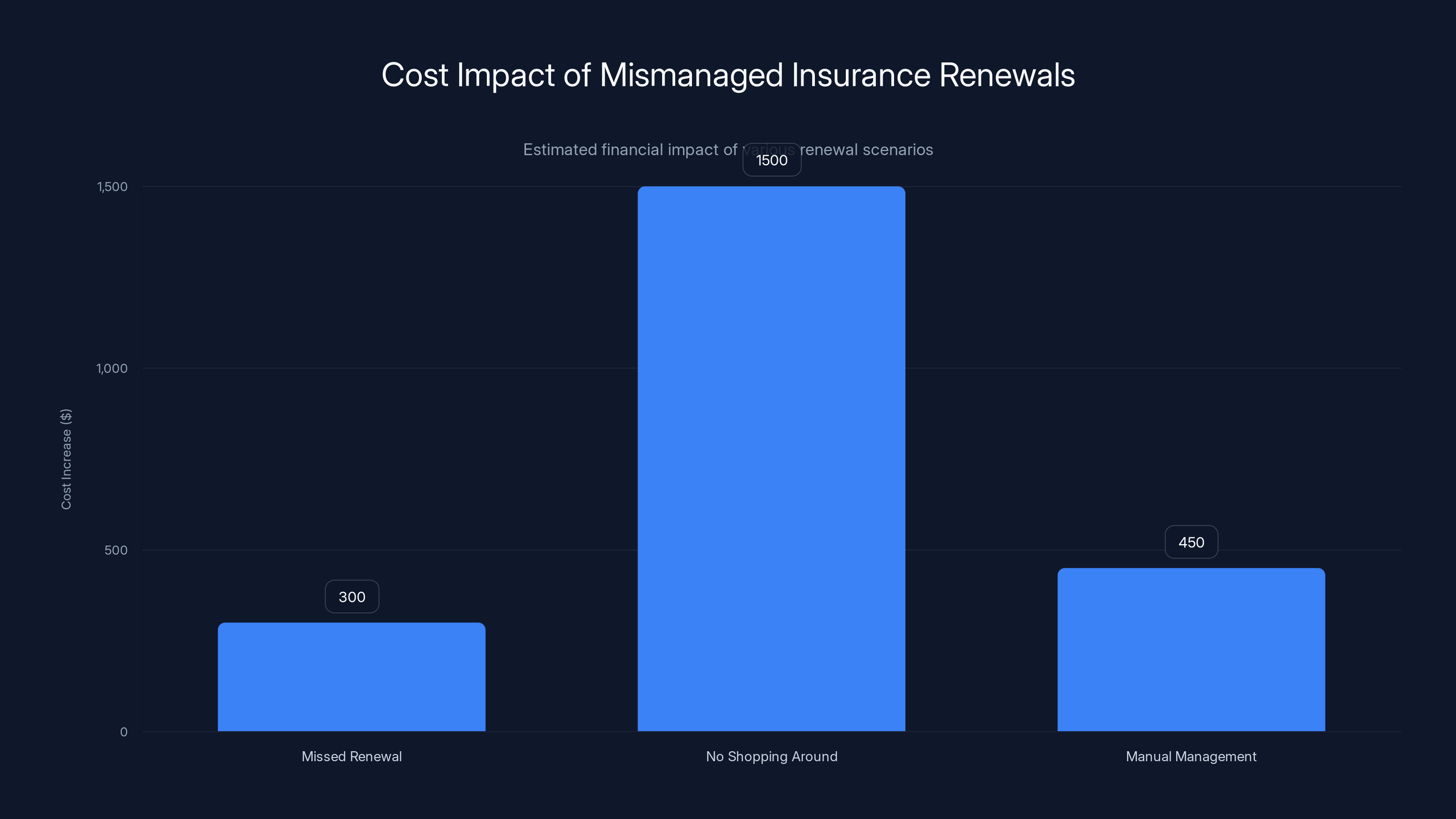

The Hidden Cost of Missed or Mismanaged Renewals

Let's put numbers to this. Say you have four major insurance policies:

- Auto insurance: Renews July 15

- Home insurance: Renews September 1

- Life insurance: Renews March 22

- Umbrella liability: Renews June 1

Tracking four dates manually is already annoying. But here's what actually happens:

You miss one renewal by a few days. Your coverage lapses. When you finally notice and reapply, you're now marked as someone whose coverage lapsed. Insurance companies see this as a red flag—it suggests you're financially unstable or disorganized. As a result, they charge you more. We're talking 15-25% higher premiums just for the privilege of getting re-quoted.

Second scenario: You remember all your renewal dates but don't shop around. You accept your insurer's renewal quote automatically. Over a year, you miss out on switching to a competitor who would have charged you 20% less. That's

Third scenario: You do all the manual work correctly—you remember the dates, shop around, get quotes, compare coverage levels. Congratulations, you've spent 4-6 hours managing your insurance renewals over the year. If your time is worth anything, that's another $300-600 in lost productivity.

Now, what if a $0 app eliminated all three problems? It would pay for itself in about 90 seconds.

How Insurance Renewal Apps Work

The mechanics are simpler than you'd think. Most insurance renewal apps follow the same basic workflow:

Step 1: Input Your Policies

You start by entering your existing insurance policies into the app. This includes policy numbers, coverage amounts, deductibles, premium costs, and renewal dates. Most apps let you upload policy documents directly, which makes this process faster—the app extracts the relevant information automatically.

Some apps can even pull this information directly from your email if you give them permission. They'll scan your email history for renewal notices and extract the dates automatically.

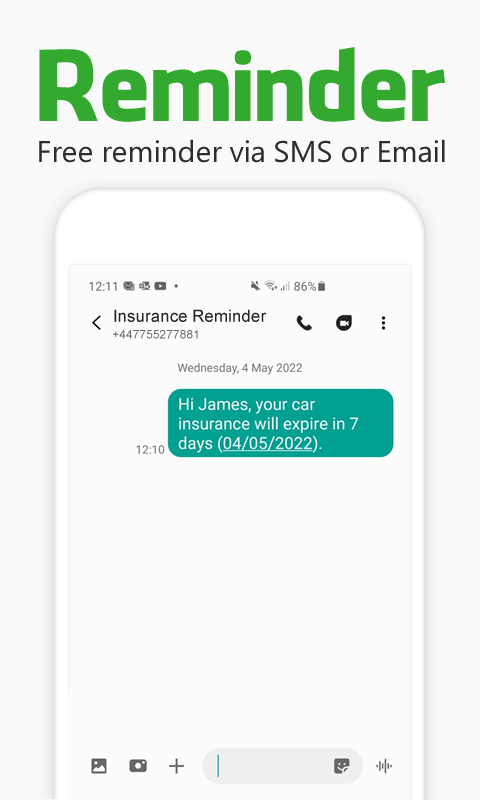

Step 2: Set Up Automated Reminders

Once your policies are logged, the app schedules notifications. Most apps let you customize when you want reminders—typically 60 days before renewal, then again at 30 days, and finally at 7 days before expiration. You get a push notification, email, or SMS (depending on your preference) reminding you it's time to act.

Step 3: Automatic Quote Aggregation

This is where the real value appears. When a renewal date approaches, the app can automatically pull quotes from multiple insurance providers. Rather than you manually visiting 5-10 insurance websites, filling out forms, and waiting for callbacks, the app aggregates quotes in one place.

Some apps use APIs to connect directly to insurance company systems, pulling real quotes instantly. Others use a network of insurance brokers who submit quotes on your behalf. Either way, you get multiple options side-by-side.

Step 4: Comparison Dashboard

You see your current policy details, your current premium, and competing quotes with side-by-side coverage comparisons. The app highlights the differences—maybe Competitor A offers 20% cheaper coverage but with a higher deductible, while Competitor B offers identical coverage for 10% less. You make an informed decision instead of a panicked one.

Step 5: One-Click Switching

Some advanced apps let you switch policies directly within the app. You click "Switch to Competitor B," and the app handles the paperwork, cancellation of your old policy, and enrollment in the new one. No phone calls required.

Less sophisticated apps simply provide you with the comparison information and recommend you contact the insurer directly. That's still a massive improvement over the current system.

Estimated data shows that missing renewals can increase costs by

The Best Free Insurance Apps Currently Available

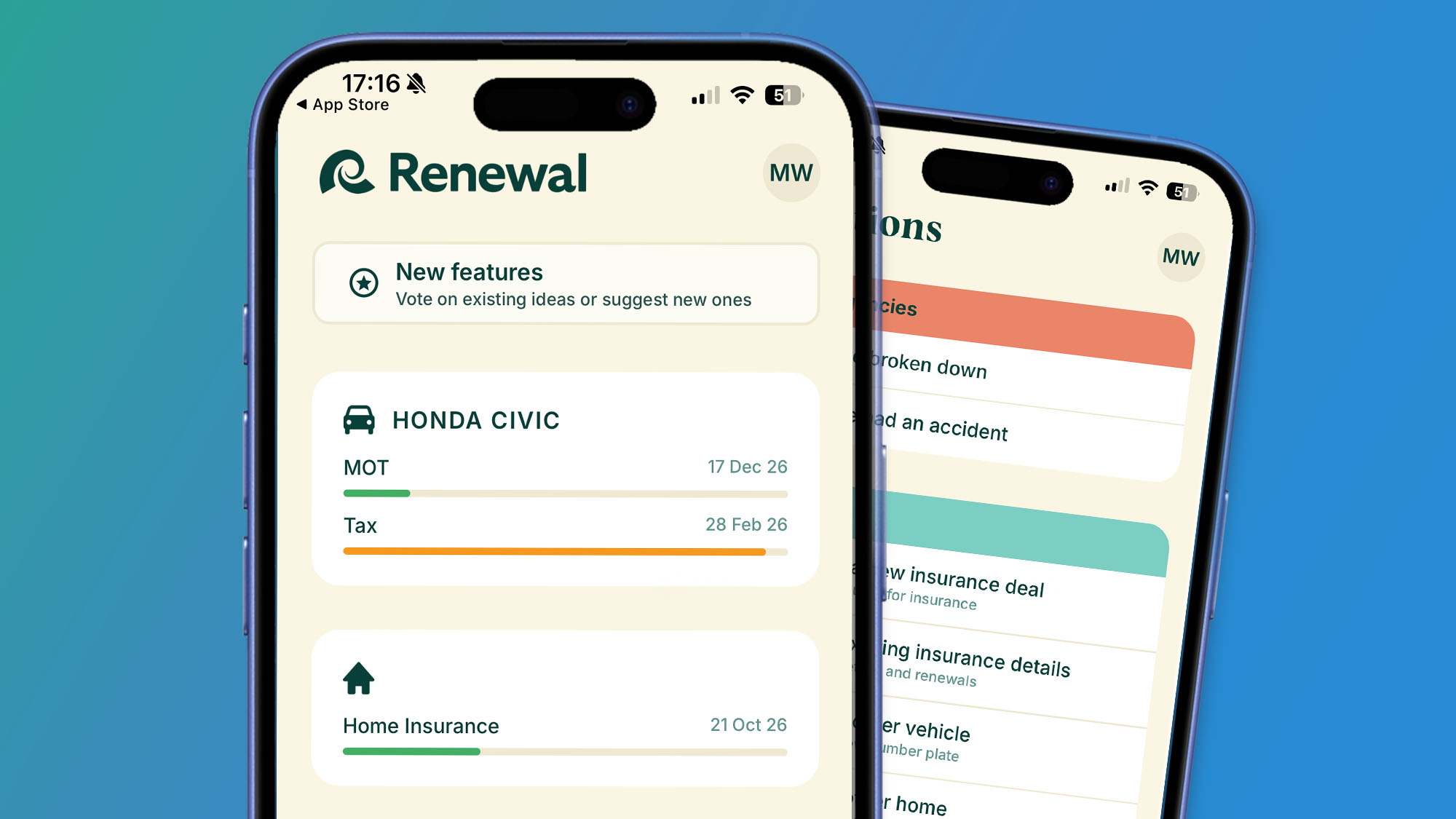

Runable

Runable offers an AI-powered automation platform that helps teams and individuals organize, track, and manage recurring tasks like insurance renewals. Rather than a dedicated insurance app, Runable functions as a comprehensive workflow automation solution that teams can customize for insurance management.

The platform creates automated dashboards that consolidate all your insurance policy information in one place. You input your policy details once, and Runable's AI agents set up recurring reminders, track renewal dates, and flag policies approaching expiration. The system integrates with your calendar and email, ensuring renewal notifications arrive at the optimal time.

What makes Runable particularly useful is its document generation capability. You can create standardized insurance comparison spreadsheets, quote tracking templates, and policy summaries automatically. Rather than manually maintaining multiple spreadsheets, Runable generates and updates these reports on demand.

The pricing starts at $9/month, making it affordable for individuals while scalable for families or small business insurance management. The free tier allows basic policy tracking, making it worth testing before committing to a paid plan.

Real-World Use Case: Sarah manages her family's four insurance policies and her small business liability coverage. Rather than managing five separate spreadsheets and calendar reminders, she uses Runable to consolidate everything. The AI system automatically alerts her 60 days before renewal, generates a comparison template, and tracks which quotes she's received. She's saved an average of 3 hours per renewal cycle and caught a renewal notice she would've otherwise missed.

Honest Assessment: Runable's strength is flexibility and automation, but it requires more setup than a dedicated insurance app. You're building your system rather than using a pre-built one. For people who like customization, it's powerful. For people who want something immediately ready-to-use, it might feel like overkill.

Use Case: Consolidate all your insurance renewals in one place and get automated reminders 60 days before expiration.

Try Runable For FreeHey Advisor (Now Part of Northstar Wealth)

Northstar, which acquired Hey Advisor's insurance technology, provides an intelligent insurance dashboard that integrates with your financial life. The platform consolidates all your insurance policies, tracks renewal dates, and provides AI-powered recommendations.

The interface is clean and intuitive. You upload your insurance documents (or connect them via email), and the system extracts key information automatically. The dashboard shows you at a glance which policies are expiring soon, where you might have coverage gaps, and where you're overpaying.

What sets Northstar apart is the integration with other financial planning tools. It sees your insurance within the context of your overall financial picture. For example, if you increase your home value, it might recommend adjusting your home insurance coverage. If you get married or have children, it prompts you to review your life insurance.

The free tier is legitimately useful. You get unlimited policy tracking, renewal reminders, and basic recommendations. The paid tier ($99/year) adds more detailed analysis and access to human advisors.

Real-World Use Case: Marcus has auto insurance, home insurance, life insurance, and an umbrella policy. He uploads all four policies to Northstar and sets up notifications. When his auto insurance is about to renew, he gets a notification not just about the renewal date, but also Northstar's analysis of whether his current coverage is appropriate for his situation and whether he should consider adjusting deductibles or coverage limits.

Honest Assessment: Northstar is excellent for integrated financial planning, but it's overkill if you just need basic renewal reminders. The free tier is genuinely helpful, though. Worth signing up just for the basic tracking, even if you don't use the premium features.

Policy Genius

Policy Genius started as a term life insurance marketplace but has expanded into a comprehensive insurance management platform. The app tracks all your insurance policies and connects you with agents to help you find better rates.

The free tracker lets you consolidate all your policies in one place. You upload documents, and Policy Genius extracts the key details. When renewal dates approach, you get notifications. Policy Genius then connects you with insurance agents who can shop around on your behalf and provide quote comparisons.

The agent-based model is interesting. Rather than pulling automated quotes from insurance systems, Policy Genius's agents manually shop around with multiple insurers. This is slower than automated systems but sometimes results in better deals because agents have access to special discounts and can explain nuances that automated systems miss.

The service is free to use. Policy Genius makes money from referral commissions when you buy a policy through them. This creates an incentive misalignment you should be aware of—they profit when you switch, which could theoretically encourage unnecessary switching. That said, their reviews suggest the recommendations are generally reasonable.

Real-World Use Case: Janet has auto insurance, home insurance, health insurance, and life insurance spread across different providers. She inputs all four policies into Policy Genius. When her auto insurance renewal arrives, Policy Genius connects her with an agent who gathers quotes from five different insurers. The agent presents her with options and explanations. She finds she can save $40/month by switching to a different insurer with slightly higher deductibles—a trade-off she's comfortable making.

Honest Assessment: Policy Genius is effective for people who want agent assistance rather than doing the legwork themselves. The downside is that you're interacting with salespeople, which adds time to the process. But for complex policies or situations where expert advice is valuable, that's worth it.

Gabi

Gabi focuses specifically on auto and home insurance with an emphasis on finding you the best rates. The app tracks your policies and automatically compares your current premium against what competitors are offering.

What makes Gabi unique is its "set it and forget it" philosophy. You grant the app permission to monitor your current premium, and Gabi periodically runs comparisons in the background. When it finds a better deal, you get a notification. No need to wait for renewal dates or manually shop around—Gabi does the monitoring continuously.

The app integrates with your phone to track your driving habits if you're willing to let it. This data helps Gabi find usage-based insurance discounts from companies that offer them. Some insurers give you 10-25% discounts based on safe driving records, and Gabi helps you access those deals.

Gabi is free to use. The company makes money through referral fees when you switch insurers. Like Policy Genius, this creates a potential misalignment, but the service has been around for years and maintains generally positive reviews.

Real-World Use Case: David has auto and home insurance with the same company. He connects Gabi to his policy information. Over the next six months, Gabi runs comparisons seven times. Five times, it finds no better rates. But twice, it identifies competitors offering 15-20% savings. David switches to one of them and saves approximately $50/month on his auto insurance. He stays with his original provider for home insurance because that quote was better there.

Honest Assessment: Gabi is excellent for people who want passive monitoring. You're not required to actively search for quotes—the app does it for you. The integration of driving habit tracking for discounts is genuinely valuable. The only downside is that it's limited to auto and home insurance; it doesn't help with health, life, or specialty policies.

Inséure

Inséure is a newer platform focusing on comprehensive insurance management with an emphasis on documentation and claim tracking. Beyond renewal reminders, Inséure helps you maintain organized policy records and makes filing claims easier.

The app consolidates all your policies in one place, tracks renewal dates, and sends reminders. But where it distinguishes itself is in document management. You can scan and store all insurance documents—policies, declarations pages, receipts, photos of valuables for inventory purposes—in one secure location. This is tremendously useful if you ever need to file a claim. Rather than digging through filing cabinets or old emails, everything is in one place with OCR-extracted search capability.

Inséure also tracks claim deadlines. Once you file a claim, the app monitors deadlines for submission of supporting documents, insurer responses, and follow-up actions. This prevents you from missing deadlines that could jeopardize your claim.

The basic tier is free with some storage limits. Premium tiers cost $49-99/year depending on storage needs and additional features.

Real-World Use Case: The Garcia family has extensive property through their home insurance—artwork, jewelry, electronics. Inséure helps them photograph and document all their valuables, storing the photos in the app with the policy. When a pipe breaks and causes water damage, they file a claim through their insurer. With Inséure, they have photos proving what they owned, policy details showing coverage limits, and a timeline of claim progress all in one place. The claim is processed faster because the documentation is organized and accessible.

Honest Assessment: Inséure is ideal if you've ever experienced the chaos of managing a claim or wanted organized insurance records. If you're just looking for renewal reminders, you're paying for features you don't need. But for comprehensive insurance life management, it's excellent.

Coverfox (Available in Select Markets)

Coverfox operates primarily in India and Southeast Asia but is expanding. The platform consolidates insurance policies and provides AI-powered recommendations based on your life circumstances.

Focusing on developing markets, Coverfox solves a particularly acute problem: in countries where insurance literacy is lower and insurance company switching is less common, people often have inadequate coverage or are paying unnecessarily high prices. The app addresses this through simplified interfaces and AI recommendations.

Unlike some competitors, Coverfox doesn't operate on a commission model from insurance companies. Instead, it's subscription-based—$0-100/year depending on tier—which removes the incentive misalignment issue. The company profits from user subscriptions, not from steering you toward specific insurers.

Coverfox's AI analyzes your profile and recommends coverage types and amounts based on Indian and Southeast Asian insurance standards. This is particularly valuable in markets where insurance norms are less established than in the US or Western Europe.

Real-World Use Case: Priya lives in Bangalore and has life insurance, health insurance, and auto insurance from different providers. Coverfox consolidates all three policies and analyzes them. The AI recommends increasing her health insurance coverage from 5 lakh to 10 lakh rupees based on her age and income level. It also suggests she's overpaying for auto insurance and shows her options with competitors. She increases her health coverage and switches her auto insurance, improving her financial security while reducing overall costs.

Honest Assessment: Coverfox is excellent for emerging markets but less relevant if you're in the US, Europe, or other developed markets where more localized options exist. The subscription model is refreshingly honest compared to commission-based competitors.

Comparison Table: Insurance Renewal Apps at a Glance

| App | Best For | Key Feature | Renewal Reminders | Quote Comparison | Pricing |

|---|---|---|---|---|---|

| Runable | Customizable automation | AI-powered workflow, document generation | Yes, automated | Via templates | $9/month |

| Northstar | Integrated financial planning | Insurance in financial context | Yes | Limited, recommendations | Free+ $99/year |

| Policy Genius | Agent-assisted shopping | Human agent comparisons | Yes | Yes, agent-powered | Free |

| Gabi | Passive monitoring | Continuous background comparison | Yes | Yes, auto/home only | Free |

| Inséure | Document organization | Claim tracking and OCR | Yes | Limited | Free + $49-99/year |

| Coverfox | Emerging markets | AI recommendations, subscription model | Yes | Yes | Free + $0-100/year |

This chart compares insurance renewal apps based on renewal reminders, quote comparison capabilities, and pricing scores. All apps offer renewal reminders, but their quote comparison features and pricing vary significantly.

Quick Navigation

- Runable for AI-powered automation and custom tracking

- Northstar Wealth for integrated financial planning

- Policy Genius for agent-assisted shopping

- Gabi for passive auto/home monitoring

- Inséure for document organization

- Coverfox for emerging markets

How to Implement an Insurance Renewal System

Step 1: Gather All Your Policy Information

Start by collecting every insurance policy you currently have. This includes:

- Auto insurance (car, motorcycle, RV if applicable)

- Home insurance (homeowner's, renters, condo)

- Health insurance (personal, family, supplemental)

- Life insurance (term, whole, variable)

- Disability insurance (short-term, long-term)

- Umbrella liability insurance

- Business insurance (if self-employed)

- Pet insurance

- Travel insurance

- Any other specialized coverage

For each policy, you need:

- Policy number

- Provider name and contact information

- Coverage amounts and deductibles

- Current premium (annual and monthly)

- Renewal date

- Policy highlights (what's covered, what's not)

Most of this information is on your policy documents or renewal notices. If you don't have these documents, contact your insurers and request copies or log into their websites to access the information.

Step 2: Choose Your Insurance Tracking Tool

Decide whether you want:

- A dedicated insurance app like Gabi or Policy Genius for simplicity

- A general automation platform like Runable for customization

- A financial planning tool like Northstar for integrated analysis

- A spreadsheet or calendar system if you have very few policies and prefer manual control

Consider your comfort level with technology, the number of policies you have, and your desire for automation. Start with free options to test before committing to paid tiers.

Step 3: Input Your Policies Into Your Chosen System

Enter each policy's information into your chosen app. Most apps let you upload policy documents directly, which extracts information automatically. This is faster than manual entry.

If using a spreadsheet or calendar system, create a table with renewal dates and set calendar reminders for 60, 30, and 7 days before each renewal.

Step 4: Set Up Notifications

Configure your app to send you reminders at strategic intervals—typically 60 days before renewal (giving time to shop around), 30 days before (for decision-making), and 7 days before (for final follow-up if you haven't acted).

Choose your notification method: push notifications, email, SMS, or calendar events. Most people benefit from multiple notification types to ensure they don't miss anything.

Step 5: Create a Comparison Framework

When renewal notifications arrive, use your app's quote comparison feature or manually gather 3-5 quotes from competitors. Create a comparison sheet showing:

- Current premium vs. competitor quotes

- Coverage limits and deductibles side-by-side

- Exclusions and special conditions

- Discounts available (safety features, bundling, etc.)

- Customer service ratings

- Claim processing reputation

Step 6: Make an Informed Decision

Don't just look at price. Consider the full package:

- Price: Is it meaningfully cheaper (15%+ savings)?

- Coverage: Is the coverage equivalent to what you currently have?

- Deductible: Are you comfortable with higher deductibles to save money?

- Customer service: Have you heard anything about this insurer's customer service?

- Claims processing: Do they have a good reputation for handling claims efficiently?

Make your decision based on the combination of these factors, not just the lowest price.

Step 7: Complete the Switch (If Warranted)

If you're switching to a competitor, follow their enrollment process. Most allow you to switch directly online. Some may require a phone call. Make sure you understand when coverage starts and when your old policy ends. Ideally, you want new coverage to start on the day your old coverage ends, with no gaps.

Step 8: Update Your Tracking System

Once you've switched, update your app with the new renewal date for the next cycle. Your system should now be continuously tracking your new policy alongside any other policies you've kept.

Switching insurers at renewal can lead to significant savings, ranging from 15% to 40% on average. Estimated data.

Common Mistakes to Avoid When Managing Insurance Renewals

Mistake 1: Not Comparing Quotes

The most expensive mistake is simply accepting your insurer's renewal rate without comparing. You're essentially leaving money on the table. Studies show switching insurers at renewal can save 15-40% on average.

The fix: Always get at least three competing quotes before renewing. It takes 15-20 minutes and can save you hundreds annually.

Mistake 2: Lowering Coverage to Save Money

It's tempting to drop coverage or reduce limits to lower your premium. This is usually a mistake. If you have a claim and you don't have adequate coverage, you're paying out of pocket.

The smarter move: Shop for better rates while keeping the same coverage. This is usually possible. If you're forced to choose between price and coverage, prioritize essential coverage (liability for auto, structural for home) and consider raising deductibles instead of dropping coverage.

Mistake 3: Forgetting About Discounts

Insurance companies offer discounts you probably don't have active:

- Safe driver discounts (especially if you've had no accidents in several years)

- Bundling discounts (combine auto and home with one insurer)

- Home security discounts (for burglar alarms, fire systems, etc.)

- Usage-based discounts (your driving habits, home safety systems)

- Affinity discounts (through employer, alumni association, etc.)

- Payment method discounts (automatic payment, paying in full annually)

When getting quotes, explicitly ask about these discounts. Often a lower-priced competitor loses its advantage once you add applicable discounts to your current insurer.

Mistake 4: Not Setting Reminders in Advance

Waiting until your renewal date arrives puts you in reactive mode. You're rushed, stressed, and make worse decisions. Setting reminders 60 days in advance gives you time to shop, think, and negotiate.

The fix: The moment you buy or renew a policy, put the next renewal date in your calendar with reminders at 60, 30, and 7 days before.

Mistake 5: Letting Lapses Happen

A lapse in insurance coverage—even by a single day—can damage your rates for years. Insurance companies categorize you as higher risk if you've had coverage gaps. When you re-apply, you'll be quoted at higher rates.

The fix: Make sure new coverage starts before old coverage ends. If switching, confirm your new policy is active before cancelling the old one.

Mistake 6: Not Reviewing Your Coverage Annually

Your needs change. You might have paid off your car, gotten married, had children, increased your home value, or changed your job. Your insurance should reflect your current situation, not your situation from five years ago.

The fix: During renewal time, take 15 minutes to review your coverage and adjust as needed. A $50 increase to higher home insurance coverage might be the right move if you've renovated your home. Dropping life insurance when you have young children is definitely the wrong move.

Advanced Strategies for Maximum Insurance Savings

Strategy 1: Bundle for Serious Discounts

Insurance companies love bundling. They'll offer 10-25% discounts if you buy multiple policies from them. In some cases, bundling can save you more than switching to a competitor entirely.

When comparing quotes, always ask what the bundled rate would be. Often the lower-priced competitor loses its price advantage when you add bundling into the equation.

The math: You might save

Strategy 2: Increase Deductibles to Lower Premiums

Increasing your deductible (the amount you pay out of pocket before insurance kicks in) lowers your premium substantially. The question is whether you have emergency funds to cover a higher deductible if you need to file a claim.

The math: Increasing your auto insurance deductible from

General rule: Never increase your deductible beyond what you can actually afford to pay out of pocket in an emergency.

Strategy 3: Time Your Renewals Strategically

Some insurers offer better rates at specific times of the year. For example, some auto insurers offer better rates for renewals in January-March (when fewer people are shopping) versus August-September (when everyone is renewing).

You can sometimes request a renewal date change. Contact your insurer and ask if they offer better rates if you shift your renewal date a month or two earlier or later. It's unconventional but sometimes works.

Strategy 4: Use Affinity Discounts

Many employers, universities, alumni associations, professional organizations, and membership groups have negotiated insurance discounts with major insurers. You might qualify for 5-15% discounts you're not aware of.

Check with your employer's HR department, your college alumni association, and any professional organizations you belong to. Ask if they offer insurance discounts.

Strategy 5: Monitor Your Insurance Continuously, Not Just at Renewal

Life changes between renewals. You might get married, buy a home, have children, or change jobs. Each of these changes might unlock new discounts or warrant coverage adjustments.

Don't wait for renewal. If you have a major life event, contact your insurer immediately. You might get better rates mid-term, or you might want to adjust your coverage.

Strategy 6: Use Credit Monitoring for Rate Changes

Some insurers factor credit scores into their rates. If you've improved your credit score since your last renewal, you might qualify for better rates. Some apps can flag credit improvements and alert you to follow up with your insurer.

Customers who shop around at renewal can save between 15% to 40% on premiums. Estimated data based on market studies.

The Future of Insurance Renewal Management

AI-Powered Personalized Recommendations

The next evolution of insurance apps will use more sophisticated AI to understand your unique situation and make personalized recommendations.

Instead of just comparing prices, AI will analyze factors like:

- Your driving habits and accident history

- Your home's specific risks (location, age, construction type)

- Your health data and family history

- Your income and financial situation

- Your risk tolerance

Based on this analysis, AI will recommend not just which insurer is cheapest, but which insurer and coverage combination best matches your specific needs and risk profile.

Integration With Digital Wallets and Smart Homes

As smart home technology expands, insurance will become increasingly integrated. Your smart home system will communicate with your insurer, proving that your home has security systems, fire detection, and water leak sensors.

Your insurer will automatically apply applicable discounts based on these systems. You won't need to manually claim the discount—it'll be automatic. Similarly, your insurance documents, policy information, and quotes will live in your digital wallet alongside other financial documents.

Real-Time Claims Processing

Today's claims process involves documentation, investigation, and waiting periods. Tomorrow's system will process claims in real-time.

When you have an accident or incident, your smart home or phone will automatically document it (photos, video, timestamps). Your insurer will process the claim immediately, and payment will be issued within hours rather than days or weeks.

Blockchain-Based Policy Management

Blockchain technology could revolutionize policy administration. Your policy information would be stored on a blockchain, accessible to you and your insurer, but protected by cryptography. This would eliminate document fraud, speed up claims processing, and make transferring between insurers nearly instantaneous.

Why Free Apps Make Sense for Insurance Companies

If these apps are free, how do they make money? Understanding this helps you assess whether they're trustworthy.

Commission Model: Most free insurance apps (Gabi, Policy Genius, Coverfox in some regions) make money by receiving referral commissions when you switch to a competitor insurer. They profit from your switch, creating an incentive to recommend switching even when it might not be in your best interest.

This isn't necessarily nefarious. In many cases, the app's recommendations are legitimately good. But understand the incentive structure. An app that profits from switching is more likely to recommend switching than an app that doesn't.

Freemium Model: Apps like Northstar and Inséure offer free basic tiers with limited features and paid premium tiers for more detailed analysis or additional storage. They profit from users who upgrade.

This model removes the switch-incentive problem. These apps make money whether you switch or stay, so they have no financial motivation to recommend unnecessary switching.

Data Model: Some apps make money by anonymizing your insurance data and selling it to researchers, insurers, or marketing companies. This helps insurance companies understand market trends and pricing.

This is fine as long as your data is truly anonymized. But understand that your participation makes you valuable to the company beyond the app itself.

B2B Model: Apps like Runable make money by selling to businesses and teams that use the platform for broader automation needs, not just insurance. Individual insurance management is a side use case.

This model also removes the switch-incentive problem. The company profits regardless of your insurance decisions.

Building Your Personal Insurance Renewal System

If you prefer not to use an app, you can build an effective system using free tools you already have:

The Spreadsheet System

Create a simple spreadsheet with columns for:

- Policy type (auto, home, health, etc.)

- Provider name

- Policy number

- Current annual premium

- Renewal date

- Months until renewal

- Notes about coverage

Sort by renewal date so you always know what's coming up next. Update it quarterly. When a renewal date approaches, manually shop around and enter competing quotes in a separate sheet.

Time investment: 1 hour to set up, 15 minutes per quarter to update, 30 minutes per renewal to shop around.

The Calendar System

Use your phone's calendar to create recurring events for each policy renewal:

- 60 days before renewal: "Shop for insurance quotes"

- 30 days before renewal: "Decision deadline - switch if warranted"

- 7 days before renewal: "Final check - confirm coverage starts today"

Set notifications for each event so you get reminders automatically.

Time investment: 15 minutes to set up, 30 minutes per renewal to execute.

The Email Folder System

Create an email folder specifically for insurance. As you receive renewal notices, policy documents, and quotes from competitors, file them in this folder. Use your email search function to find information quickly when you need it.

Time investment: 30 seconds per document to file, minimal ongoing maintenance.

The Hybrid System

Combine approaches: Use a spreadsheet to track renewal dates, your calendar for reminders, and an email folder to organize documents. This requires minimal tech savviness and costs nothing.

The Math of Insurance Renewal Savings

Let's calculate the actual financial impact of systematic renewal management:

Base Scenario (No Action)

- Auto insurance: 7,200

- Home insurance: 9,000

- Life insurance: 3,600

- Total over 6 years: $19,800

Active Shopping Scenario

Assume you save 20% by shopping around at each renewal (a conservative estimate).

- Year 1 (new policies from shopping): $2,100 total

- Year 2 (renewal, shop again, save 20%): $1,680

- Year 3 (renewal, shop again, save 20%): $1,680

- Year 4 (renewal, shop again, save 20%): $1,680

- Year 5 (renewal, shop again, save 20%): $1,680

- Year 6 (renewal, shop again, save 20%): $1,680

- Total over 6 years: $10,500

Difference: $9,300 saved over 6 years

That's

Even accounting for time spent, the financial case is overwhelming.

FAQ

What is an insurance renewal app?

An insurance renewal app is software that tracks your insurance policies, reminds you when renewals are approaching, aggregates quotes from multiple competitors, and helps you make informed decisions about switching providers. Apps range from simple tracking systems to complex AI-powered recommendation engines.

How do insurance renewal apps get my policy information?

Most apps ask you to upload policy documents directly, or they can access your email to find renewal notices and extract information automatically. Some advanced apps integrate directly with insurance company systems via APIs. You maintain complete control over what information you share.

Are these apps safe to use?

Reputable apps use standard encryption and security protocols to protect your information. However, you should verify the app's privacy policy before using it. Avoid apps that don't clearly explain how they protect your data or what they do with it. Established companies like Policy Genius and Gabi have been through security audits and are generally trustworthy.

Can I really save money by switching insurers?

Yes. Studies consistently show that customers who actively shop around at renewal can save 15-40% on insurance premiums. The exact savings depend on your profile, location, and coverage needs. Even a 15% savings is substantial. However, don't switch solely for price—ensure coverage levels are appropriate for your situation.

What if I'm happy with my current insurance company?

Still shop around. You might discover that your current company offers better pricing than you're currently paying, which you can use to negotiate a better renewal rate. Or you might find a competitor offering similar coverage for less, giving you the option to switch. Either way, having information improves your position.

How often should I shop for insurance?

Minimum: at every renewal date. If you're ambitious: every 1-2 years even if you're not at a renewal date. Major life changes (marriage, children, home renovation, job change) warrant a review of your coverage and rates even if renewal isn't approaching.

Can insurance companies penalize me for shopping around?

No. Shopping around has no impact on your rates or coverage. Many companies offer discounts specifically to attract customers who are switching from competitors. The only thing that affects your rates is whether you actually switch and what information you provide about accidents, claims, or lifestyle changes.

What information do I need to have before using an app?

Have ready: policy numbers, current premiums, renewal dates, coverage amounts, and deductibles for each policy. You'll also need some personal information (age, address, driving record) to get accurate competing quotes. Most apps guide you through what they need step-by-step.

Do I lose coverage if I switch during a renewal?

No, as long as you time it correctly. Your new coverage typically starts on the renewal date of your old policy. Your old policy ends that same day. There's no gap. However, make sure to confirm your new coverage is active before your old policy ends, just to be safe.

Are free apps really free or are there hidden costs?

Legitimate free apps don't charge you. They make money through referral commissions from insurance companies, data sales, premium tier upsells, or as a side service from a larger company. You don't pay directly. However, understand the financial incentives—an app that makes money when you switch might subtly encourage unnecessary switching. Read privacy policies to understand what data the company collects and sells.

Conclusion: Take Control of Your Insurance Renewals

Missing insurance renewals or passively accepting renewal quotes costs the average American thousands of dollars annually. It's one of the easiest areas of personal finance to improve, yet most people don't do it because the process feels complicated.

That's what apps solve. They take the complexity out of tracking, comparing, and switching. Some apps, like Runable, offer flexible automation platforms. Others, like Gabi or Policy Genius, specialize purely in insurance. Still others, like Northstar, integrate insurance into broader financial planning.

The specific app you choose matters less than the fact that you choose something. Even a simple calendar reminder system beats the current approach of "I hope I remember and I hope the renewal rate isn't terrible."

Here's what I'd recommend: Pick one app from this guide, spend 15 minutes setting up your policies, and let it manage your renewals for one year. You'll likely save enough money to cover the entire cost of any paid tier (if applicable) and then some. After one successful renewal cycle, you'll understand the process and can repeat it annually.

The time investment is minimal. The financial payoff is substantial. And the peace of mind of knowing you've actively managed your insurance—rather than hoping for the best—is priceless.

Start today. Pick an app. Input one policy. You'll be glad you did.

Key Takeaways

- Missing insurance renewals or passively accepting quotes costs the average American family $1,550+ annually

- Insurance renewal apps eliminate manual tracking and automatically compare quotes across multiple competitors

- Active shopping at renewal time saves 15-40% through switching providers or leveraging competing quotes for negotiation

- Free apps like Gabi, PolicyGenius, and Runable reduce the friction of insurance management without upfront costs

- Strategic renewal management requires setting reminders 60 days in advance and comparing coverage limits alongside price

Related Articles

- Monarch Money Budgeting App: Complete Guide to 50% Off Deal [2025]

- Best Budgeting Apps: Monarch Money 50% Off Deal [2025]

- Monarch Money Annual Deal: Save 50% on Premium Budgeting [2025]

- Monarch Money Budgeting App: $50/Year Deal + Complete Review [2025]

- Monarch Money Deal: $50 for One Year (50% Off) [2025]

- Monarch Money 50% Off Deal: Complete Guide to Annual Budgeting [2025]