MediaTek Slashes Employee Bonuses Amid Global Chip Shortage Crisis: What It Means for Tech Workers and the Industry

When a major semiconductor company starts cutting employee bonuses, it's not just bad news for the folks in accounting. It's a red flag that ripples across the entire tech industry—a signal that something's seriously wrong with the supply chain, profit margins, and the global appetite for chips.

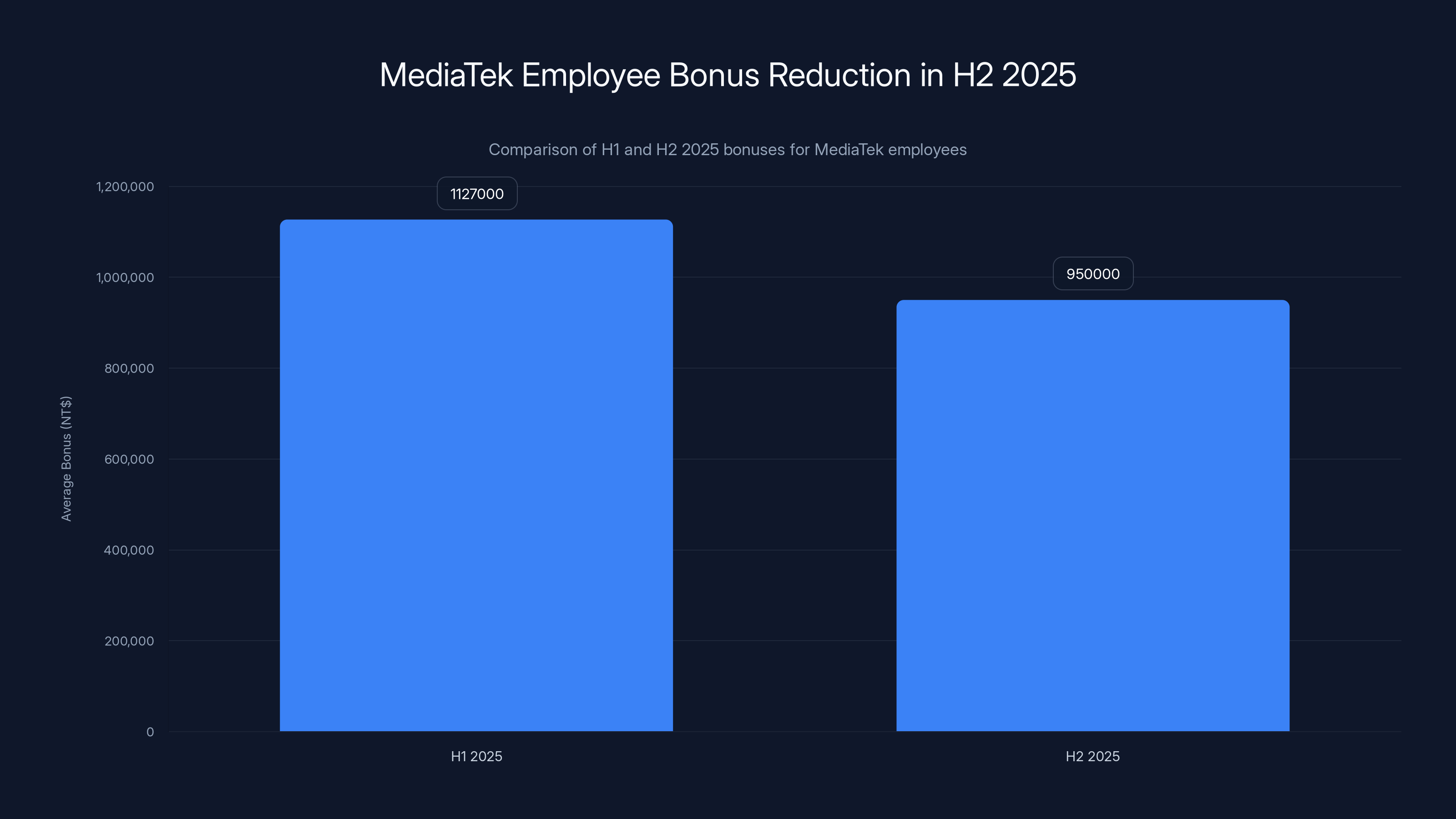

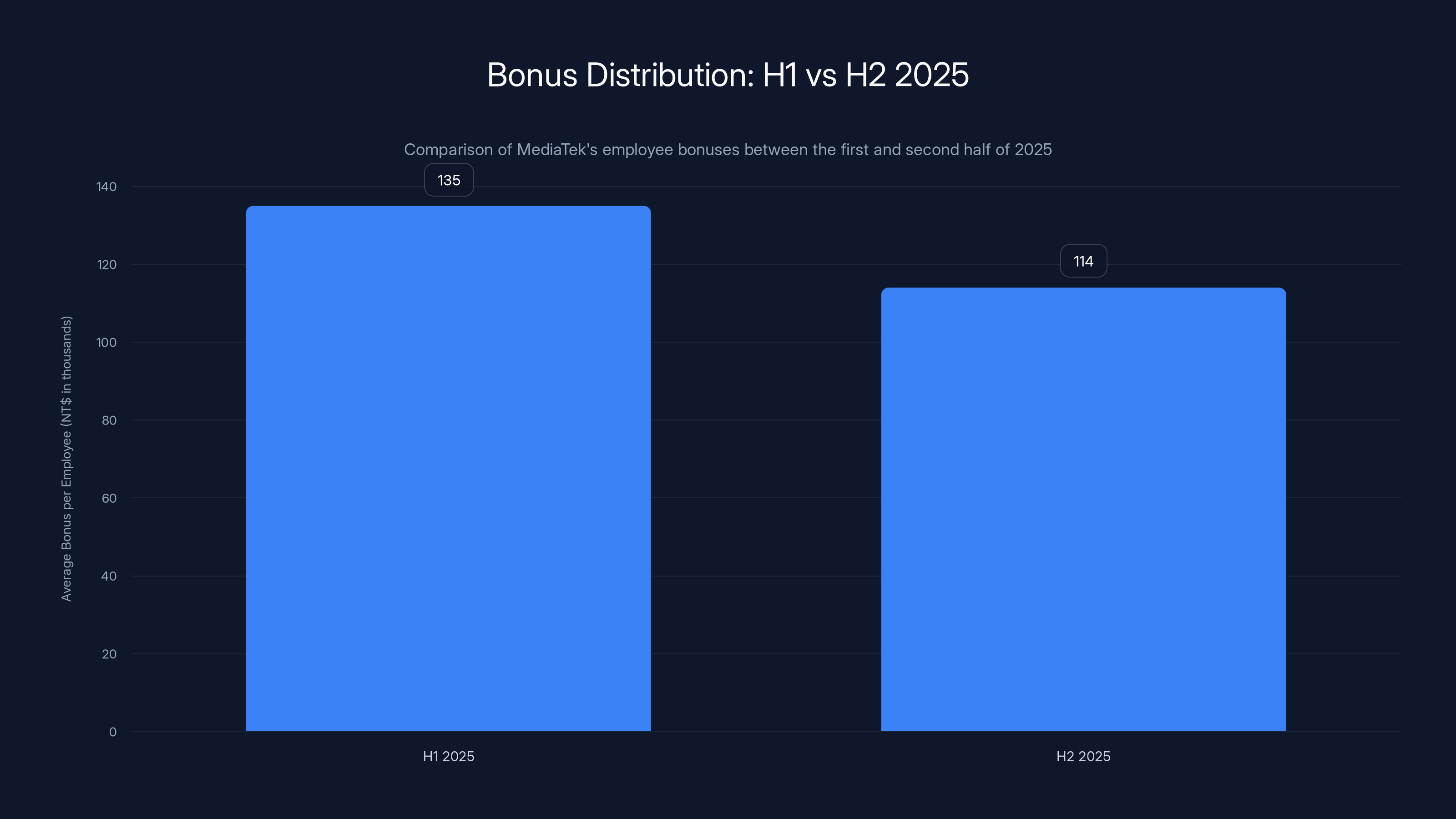

In late 2025, MediaTek did exactly that. The company reduced H2 2025 bonuses by 15.7% compared to what employees received in the first half of the year. For roughly 12,000 eligible employees, that meant an average H2 bonus of approximately NT

This isn't about mismanagement or a sudden drop in company performance. It's about pressure. Real, sustained pressure from two directions: tight DRAM (RAM) and NAND (storage) supplies constraining growth, and a global market for chips that's not expanding as fast as it used to. When companies start slashing bonuses—especially at the scale MediaTek operates—it means they're bracing for leaner times ahead.

Here's what you need to know about why this matters, how it happened, and what it tells us about where the tech industry is headed.

The 15.7% Bonus Cut Explained: What Changed Between H1 and H2 2025

Let's start with the numbers, because they tell the story better than any press release could. MediaTek's H2 2025 bonus pool totaled approximately NT

MediaTek doesn't typically announce bonus reductions. The company awards bonuses twice a year, determined by department performance, individual job level, and personal evaluations. When bonuses decline, it's usually because revenue targets weren't hit or profit margins contracted. In this case, both factors were at play.

What makes this cut interesting is the timing. Mid-2025 is when DRAM and NAND supply constraints really started biting. These aren't MediaTek's own products—the company is a fabless chipmaker, meaning it designs chips but outsources manufacturing to foundries like TSMC. What MediaTek does make are smartphone processors (the Dimensity series), Wi-Fi and Bluetooth chips, and components for IoT devices. All of those designs rely on DRAM and NAND as integrated components or companion chips in final products.

When DRAM and NAND get tight, two things happen. First, device manufacturers—the companies actually building phones and tablets—start hoarding chips or shifting orders to secure supply. This creates artificial demand spikes that distort the market. Second, costs for those memory components spike, squeezing margins for companies that need to bundle them with their main products.

For MediaTek, this means that even if they're shipping the same number of Dimensity processors, the overall revenue per chip could be lower, or the cost of goods sold could be higher. Either way, profit margins shrink. And when margins shrink, bonuses shrink with them.

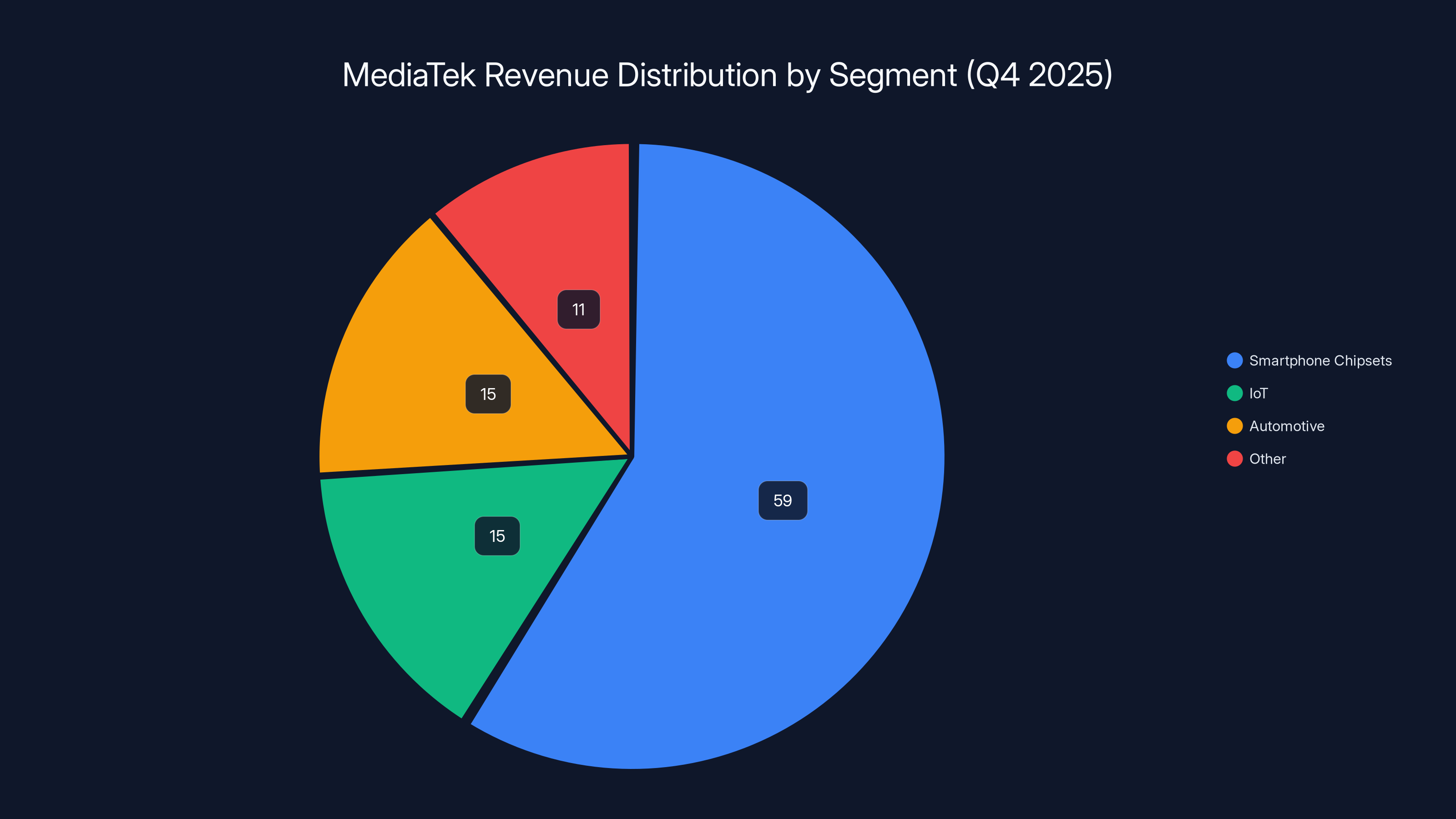

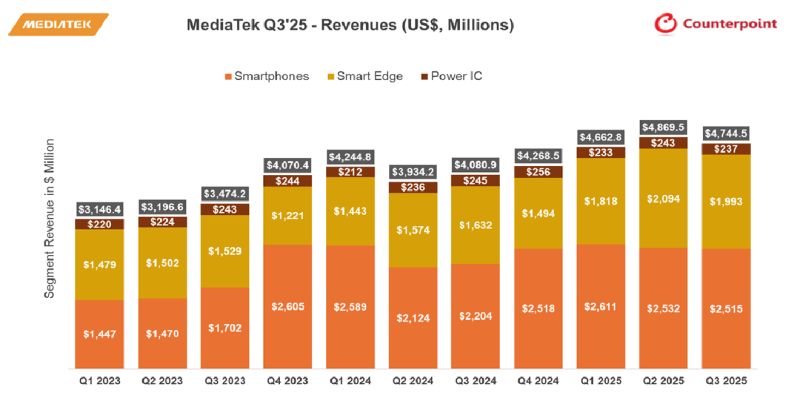

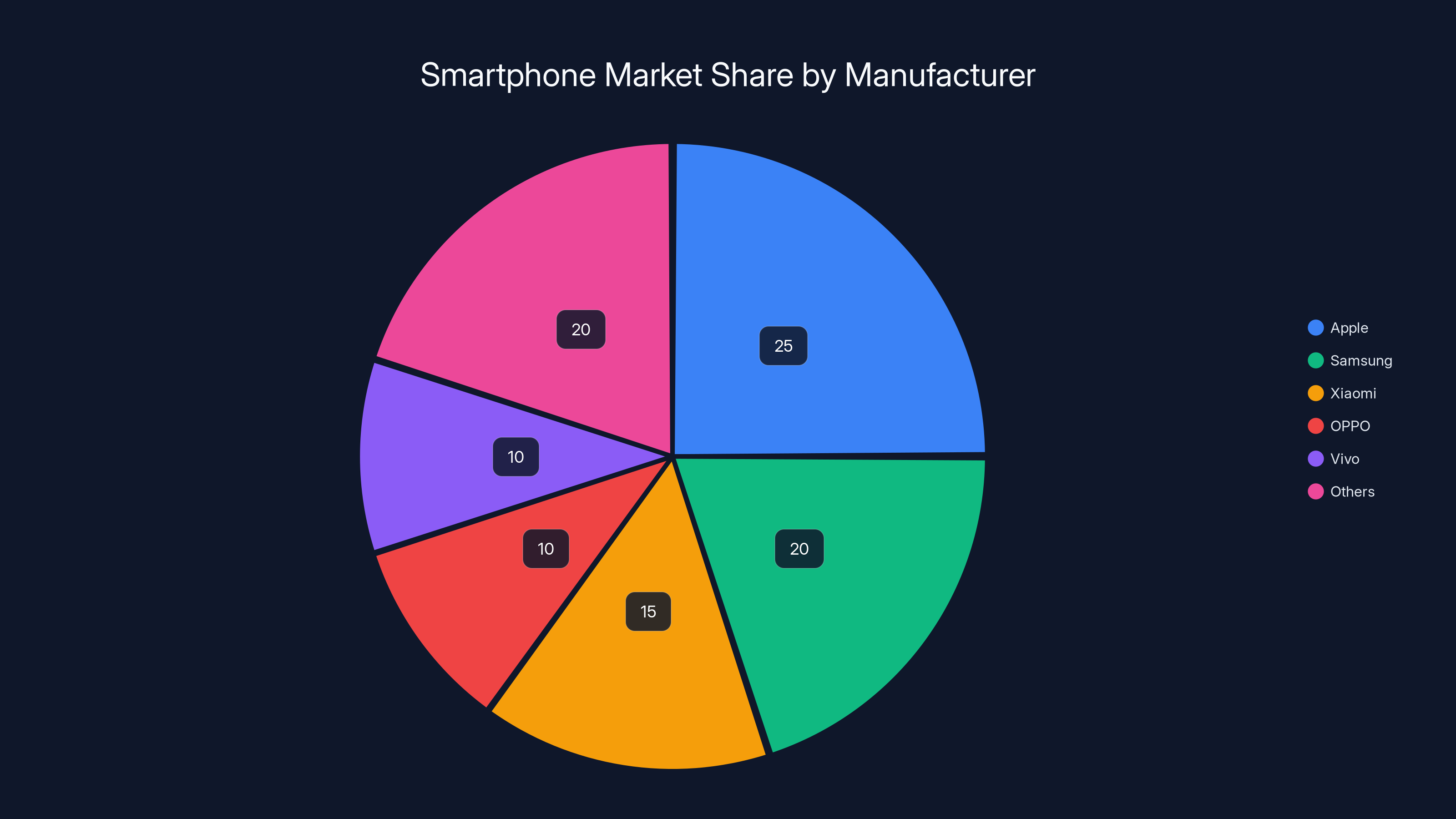

Smartphone chipsets account for 59% of MediaTek's Q4 2025 revenue, indicating a significant dependency on this market segment. Estimated data for other segments shows diversification is limited.

Understanding DRAM and NAND: Why Memory Shortages Are Crushing Margins

Here's a detail many people miss about semiconductor shortages: it's not always about the chips everyone talks about. In 2021-2022, everyone obsessed over processor shortages. But the real constraint chokepoint in 2025? Memory.

DRAM (Dynamic Random-Access Memory) is what devices use for working memory—RAM in your phone, laptop, or server. It's fast, temporary storage. NAND Flash is persistent storage—the SSDs in laptops, the storage in your phone, USB drives. Both are essential. And both have been in tight supply relative to demand throughout 2025.

Why does this matter to MediaTek specifically? Because smartphone makers don't just buy a processor. They buy a complete package: a CPU chip, GPU, modem, DRAM, NAND storage, and various other components. When NAND is tight and expensive, phone manufacturers have two choices. They either accept lower profit margins to maintain pricing and volume, or they cut production to protect margins. Either way, the demand for companion chips like what MediaTek makes declines.

Consider the math. A smartphone might use:

- 1 MediaTek Dimensity processor (roughly $15-25 depending on model)

- 6-8GB of DRAM (roughly $3-5 depending on market conditions)

- 128-256GB of NAND (roughly $10-20 depending on density)

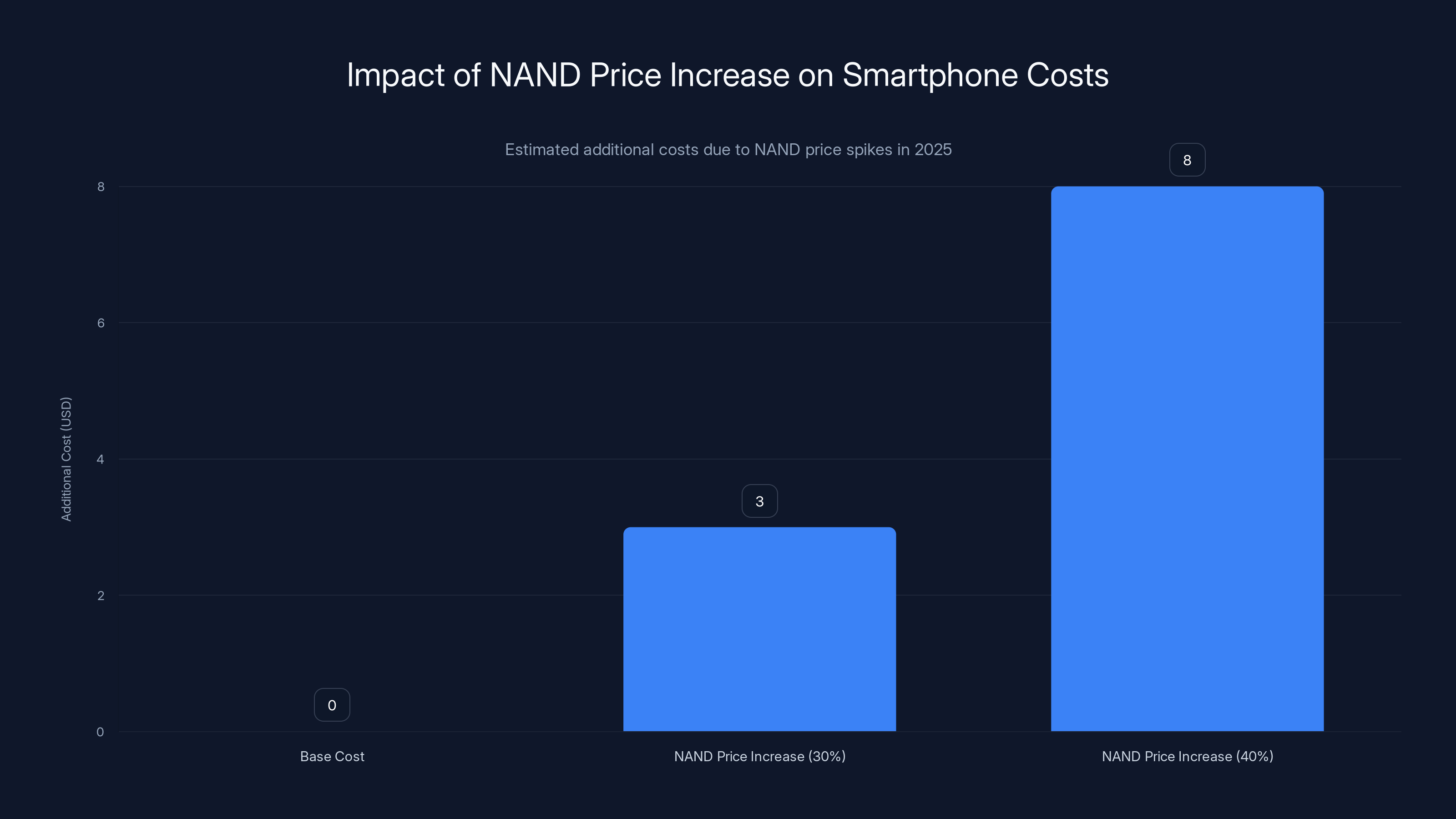

When NAND prices spike 30-40%, that adds $3-8 to the cost of a phone. Phone makers respond by either raising prices (which depresses demand) or accepting lower margins. Both scenarios reduce demand for MediaTek's chips.

Add to this the reality that smartphone sales growth has slowed dramatically compared to 2021-2023. The market is maturing. People aren't upgrading their phones as frequently. Even with flagship AI-powered devices entering the market in 2024-2025, overall unit sales growth is flat to slightly negative in many regions.

That combination—tight memory supply, elevated memory costs, slowing smartphone growth, and compressed margins—is exactly the environment that triggers bonus reductions.

MediaTek's Revenue Concentration Risk: 59% From Smartphone Chipsets

Here's a vulnerability most casual observers don't appreciate about MediaTek: they're extremely dependent on one market segment. Smartphone chipsets accounted for 59% of the company's total revenue in Q4 2025. That's nearly three-fifths of all revenue coming from a single product category.

For context, that's actually quite high. Qualcomm, MediaTek's biggest competitor, has more diversification—they make automotive chips, IoT processors, and enterprise solutions alongside smartphone processors. But MediaTek? They're betting the company on phones.

This concentration creates structural risk. When smartphone market dynamics shift—whether due to supply constraints, slowing demand, or competitive pressure—MediaTek feels it acutely. There's no cushion from other business segments to absorb margin pressure.

During the smartphone boom of 2017-2021, this concentration was actually an asset. Everyone wanted phones. Everyone upgraded regularly. MediaTek's market share in Asia soared. But as smartphone growth decelerated in 2023-2024 and supply chain complexity intensified in 2025, that same concentration became a liability.

The bonus cut is essentially management acknowledging: "We can't count on smartphone revenue growth to absorb margin pressure. We need to tighten our belts."

Additionally, MediaTek's premium segment remains smaller than Qualcomm's. While the Dimensity 9600 (expected on 2nm process) is competitive, Qualcomm's flagship Snapdragon 8 Elite still commands higher prices and greater market mindshare in premium phones. MediaTek's strength is in mid-range and budget segments, where volumes are higher but margins are thinner. When margins compress from supply chain pressure, those lower-margin segments feel the pain first.

MediaTek reduced employee bonuses by 15.7% in H2 2025 compared to H1, reflecting the impact of the global chip shortage on the semiconductor industry.

The Dimensity 9600: Innovation Alone Won't Solve Margin Compression

MediaTek is investing heavily in next-generation technology. The Dimensity 9600, expected to arrive on a 2nm process node from TSMC, represents a significant architectural and manufacturing advancement. 2nm manufacturing is cutting-edge—only TSMC and Samsung are there, and TSMC has the most mature process.

Advanced lithography does deliver real benefits: smaller transistors mean better power efficiency, higher performance, and potentially lower heat dissipation. For a smartphone processor, that translates to longer battery life, faster performance, and better thermal management. These are genuine selling points.

But here's the trap: moving to more advanced process nodes is expensive. R&D costs for 2nm designs are substantially higher than 5nm or 7nm. Manufacturing costs per wafer go up, even if the cost per individual chip might come down due to higher transistor density. MediaTek has to amortize those development costs across shipment volumes. If shipment volumes are constrained by memory shortages or market weakness, the R&D cost burden per unit rises.

Likewise, moving to 2nm doesn't automatically solve the margin problem. Qualcomm will also be on 2nm. Samsung will push their Exynos processors onto advanced nodes. The performance delta between competitors shrinks at advanced nodes because all companies are fighting for the same physics-based advantages and working with the same toolset constraints.

What actually determines margins in that scenario? Volume. Scale. And ability to secure supply of complementary components like DRAM and NAND at reasonable costs. The bonus cut suggests management doesn't feel confident about any of those factors through the rest of 2025 and into early 2026.

DRAM Price Dynamics: A Perfect Storm for Semiconductor Margins

Let's zoom out and look at DRAM pricing specifically, because it's a bellwether for the entire semiconductor supply chain health.

DRAM market dynamics are fascinating because they're driven by a weird combination of factors: manufacturing capacity (which is expensive and long-lead), sudden demand spikes from AI computing and data centers, legacy demand from smartphones and PCs, and geopolitical constraints on supply. In 2025, all of those factors converged to create tight supply.

AI chips—GPUs, TPUs, training processors—require massive DRAM for operations. The training alone for large language models consumes gigantic quantities of DRAM. Companies like NVIDIA, Google, Amazon, and Microsoft are all buying DRAM in unprecedented quantities for AI infrastructure. This pulls supply away from consumer electronics.

Meanwhile, smartphone demand isn't declining, but it's not growing strongly either. Older phones still work fine. 5G penetration is high in developed markets. The upgrade cycle has extended from 3 years to 4-5 years for many users. That means less DRAM demand from smartphones per capita, but still substantial in aggregate due to installed base.

Add in PC demand (which has stabilized but not exploded), IoT devices (growing but still smaller than consumer electronics), and automotive chips (growing rapidly, very high margin, getting access to premium DRAM supply due to automotive industry leverage). The result? DRAM supply is tight relative to total demand, prices are elevated, and device makers competing for allocation are getting squeezed.

MediaTek, as a company that needs to bundle DRAM with finished products or coordinate with device makers who buy DRAM separately, faces margin pressure on multiple fronts. If MediaTek is contracting design wins due to customers facing DRAM cost pressure, that's direct revenue impact. If MediaTek is bundling DRAM with chipsets, then DRAM cost increases flow directly to cost of goods sold and compress margins.

The bonus cut is management saying: "We think this stays tight for a while. We're preparing for sustained margin compression."

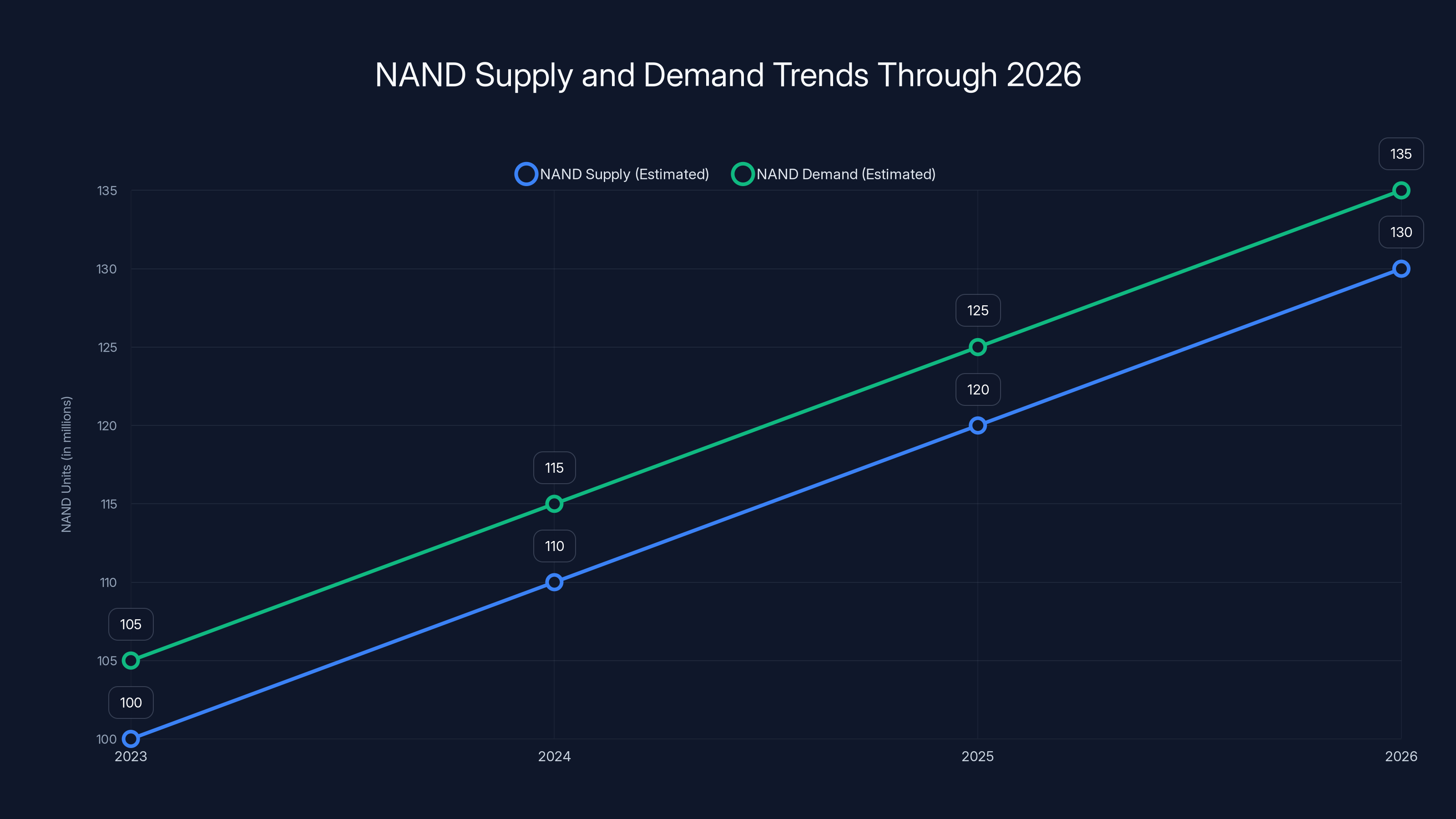

NAND Supply and Storage Market Constraints Through 2026

NAND Flash supply is even more complicated than DRAM because it plays multiple roles. SSDs for data centers and PCs require massive NAND capacity. Consumer devices (phones, tablets) need NAND for storage. IoT devices increasingly use NAND. And the transition to 3D NAND stacking has created a bifurcated market where some manufacturers excel at high-layer-count 3D NAND while others lag.

In 2025, smartphone makers faced pressure because they wanted to maintain storage options (128GB, 256GB, 512GB) at reasonable costs, but NAND pricing wasn't cooperating. Enterprise SSD demand for AI infrastructure was pulling NAND supply upmarket, leaving consumer electronics with tighter allocation and higher costs.

This created a cascading effect: phone makers couldn't hit their target bill of materials (BOM) costs, so they reduced storage options or increased phone prices. Storage reductions meant less NAND needed per device, but it also meant lower average selling prices (ASPs) due to consumer preference for lower storage SKUs. Either way, total revenue from smartphones dipped or margins compressed.

MediaTek's bonus cut happened in this context. Management was likely seeing—in real-time—their customer conversations shifting. Customers were saying: "We're cutting storage SKUs" or "We're deferring high-volume models due to BOM pressure" or "We're shifting to lower-tier processors to hit price targets." All of those conversations point to lower demand for high-performance MediaTek chips.

Projections into 2026 suggest NAND supply could normalize, but it will take time. New capacity is coming online, but fab expansion at major manufacturers like Samsung, Kioxia, and Micron takes years. The immediate outlook for late 2025 and early 2026 remains constrained.

Estimated data suggests NAND demand will continue to outpace supply through 2026, with potential normalization as new manufacturing capacities come online.

Smartphone Market Reality: Growth Isn't Coming Back

Here's the uncomfortable truth that nobody wants to say out loud in the smartphone industry: the growth era is over. Not permanently, but for the foreseeable future (the next 2-3 years minimum).

Global smartphone shipments peaked around 1.5 billion units annually in 2021. In 2025, analysts project roughly 1.2-1.3 billion units. That's a decline of 15-20% from peak. Sure, some of that was from the post-pandemic normalization and the chip shortage disruption of 2021-2023, but a significant part is structural: market saturation.

In developed markets (North America, Western Europe, Japan, South Korea), smartphone penetration exceeds 80% of the population. Growth there is purely replacement demand—existing users upgrading. The upgrade cycle has extended because phones are better and more durable, and because incremental improvements year-over-year are less dramatic.

In emerging markets where growth is stronger, price sensitivity is extremely high. Consumers in India, Indonesia, Vietnam, and Africa want affordable phones, not premium flagships. That means demand skews toward budget and mid-range processors, where margins are lower. MediaTek dominates this segment, but volumes don't translate to profitability the way flagship chips do.

The smartphone market is essentially mature. It's a replacement market, not a growth market. In mature markets, competition intensifies and margins compress. That's not MediaTek-specific—it's an industry-wide dynamic. But companies respond to mature market conditions by cutting costs, including compensation.

The bonus cut is management acknowledging: "We're not expecting smartphone unit growth to drive margin recovery. We're preparing for sustained competition in a flat market."

Competitive Pressure from Qualcomm: Premium Segment Challenges

Qualcomm remains the dominant player in premium smartphone processors. The Snapdragon 8 Elite, used in flagship phones from Samsung, OnePlus, and others, commands high prices and massive volumes. MediaTek's Dimensity 9600 will be competitive, but Qualcomm's brand equity in the premium market is harder to displace.

This matters for margins because premium chips carry higher prices and lower unit volumes (premium phones have smaller market share than budget phones). Losing ground in premium is losing the highest-margin revenue. MediaTek's strategy of focusing on mid-range and budget is sensible for volume, but it's vulnerable to margin compression.

When Qualcomm cuts prices in response to supply chain pressure, MediaTek has to follow. The entire value chain gets compressed. And when you're dependent on 59% of your revenue coming from a single market segment facing that exact dynamic, bonus reduction becomes inevitable.

Qualcomm hasn't announced bonus cuts (or at least, it hasn't leaked to the media like MediaTek's has). But that's partly because Qualcomm has diversification—they make automotive chips, automotive solutions are growing margins, enterprise and IoT are diversified. MediaTek doesn't have that cushion.

Supply Chain Cascades: How One Shortage Becomes Industry-Wide Pain

Here's how semiconductor supply chain dynamics actually work, and why a DRAM shortage becomes everyone's problem:

-

Upstream constraint: DRAM capacity becomes tight. Manufacturers can't make enough at current prices.

-

Price spike: DRAM prices rise 30-40% as device makers compete for allocation.

-

Bill of materials (BOM) pressure: Phone makers, laptop makers, and server builders see their component costs rising. They have two options: accept lower margins or reduce functionality/specifications.

-

Design-in uncertainty: If a device maker is considering whether to include 12GB or 8GB of DRAM, they might reconsider the processor choice entirely. A slightly less powerful processor with lower cost becomes attractive if it means they can maintain their target price.

-

Volume uncertainty: Uncertainty about BOM costs translates into uncertainty about model quantities. Manufacturers become conservative with orders.

-

Processor demand volatility: Processor makers like MediaTek see more volatile, less predictable demand because the variable driving decisions is memory cost, not phone demand.

-

Margin compression: With more volatile demand and pricing pressure, processor makers compress margins or cut compensation.

MediaTek's bonus cut is somewhere between steps 5 and 7 in this cascade. The company was seeing demand volatility and anticipating margin pressure based on that volatility.

Estimated data shows that a 30-40% increase in NAND prices can add $3-8 to the cost of a smartphone, affecting profit margins and demand.

Q4 2025 Revenue Concentration: 59% Smartphone Exposure

Let's make this concrete with actual data. MediaTek's Q4 2025 results showed smartphone chipsets accounted for 59% of total revenue. That's the highest concentration among its major business segments.

Breaking down the remaining 41%:

- About 20-25% from IoT and smart home devices

- About 10-15% from automotive chips

- About 5-10% from other segments (legacy products, licensing, etc.)

Automotive is growing fastest (double-digit growth annually), but it's starting from a smaller base. IoT is stable but not explosive. The reality is that smartphone revenue is where the scale is, and it's also where the pressure is.

This revenue mix explains why a smartphone market slowdown hits so hard. MediaTek can't absorb the impact across a diversified portfolio. They're taking it directly to the bottom line.

The 12,000-Employee Impact: What This Means for Retention

MediaTek has roughly 12,000 employees eligible for the bonus reduction. Most of those are engineers, product managers, and operations staff—the people who design chips, manage production, and interact with customers.

A 15.7% bonus cut doesn't sound apocalyptic in isolation. But context matters. These people are highly skilled, in-demand professionals. They likely have other options. A software engineer in Taipei or Singapore could switch to NVIDIA, Google, or any other tech company. A product manager could move into management consulting.

When a company cuts bonuses unexpectedly, employees read it as: "Management thinks times are getting tougher." That creates subtle but real retention risk, especially among top performers who have options. A company can usually retain people through a one-year margin crunch. But if people believe the crunch is going to extend, they start job hunting.

MediaTek's message with this bonus cut is important: they're not panic-cutting compensation. Bonuses still exist. The reductions are moderate, not draconian. But they're also saying: "Prepare for 2026 to be tougher than 2025." That message ripples through the organization and affects hiring, retention, and morale.

Industry Signals: What Other Chipmakers Are Doing

MediaTek isn't alone in tightening compensation. Across the semiconductor industry, 2025 saw more conservative bonus structures than 2023-2024:

Qualcomm has been more selective with hiring and more conservative with external compensation growth, though they haven't announced across-the-board bonus cuts at the scale of MediaTek's.

AMD has indicated more cautious outlooks on margin trajectory, though their diversification (CPUs, GPUs, data center, gaming) gives them more resilience than fabless designers.

Broadcom remains heavily dependent on data center spending, which has been good but faces uncertainty due to AI infrastructure investment pullback cycles.

Marvell Technology similarly relies on data center and storage, which provides some margin protection but also creates exposure to capex cycles.

The common thread? Every chipmaker is either reducing compensation growth, being more conservative with hiring, or both. It's not about individual company failure. It's about industry-wide recognition that margins are under pressure and growth is uncertain.

MediaTek's bonus cut is an honest signal of that reality, maybe more honest than some competitors are being publicly.

MediaTek's average employee bonus decreased by 15.7% from H1 to H2 2025, reflecting tighter profit margins due to supply constraints and increased costs.

Geopolitical Factors: Taiwan and US-China Tensions

MediaTek is headquartered in Taiwan. Manufacturing happens at TSMC, also Taiwan. This creates geopolitical risk that compounds the supply chain pressure.

The US-China relationship remains tense, with restrictions on semiconductor exports to China, limitations on advanced manufacturing capabilities there, and unpredictable policy shifts. Taiwan's status remains ambiguous and occasionally fraught. These factors create strategic uncertainty about supply chain security and policy changes.

When management is already dealing with supply chain tightness and margin pressure, geopolitical uncertainty adds an additional layer of caution. Companies become more conservative with capital allocation, hiring, and compensation commitments.

It's possible (and likely) that MediaTek's management included geopolitical uncertainty in their thinking when deciding on the bonus reduction. Not as the primary cause, but as a reason to be more cautious going forward.

Manufacturing Reality: TSMC Capacity and Cost Pressures

MediaTek designs chips, but TSMC manufactures them. That relationship matters for understanding the bonus cut.

TSMC has been transitioning to advanced nodes (3nm, 2nm, 1.6nm coming soon). These processes are expensive—both in terms of R&D amortization and per-wafer manufacturing costs. Moving to 2nm for the Dimensity 9600 means higher per-unit manufacturing costs than 5nm production.

TSMC prices these advanced nodes at a premium, which is completely rational—they're cutting-edge. But it means that to maintain competitive pricing on finished chips, MediaTek either has to accept lower margins or find other cost efficiencies.

Additionally, TSMC prioritizes customers and products based on a complex calculus of margin, volume, and strategic importance. MediaTek, while important, isn't TSMC's only major customer. NVIDIA (GPUs), AMD (CPUs), Apple (processors), Qualcomm (processors), and others all compete for TSMC allocation. During times of tight capacity, everyone feels pressure.

If MediaTek was getting hints from TSMC about allocation uncertainty or pricing increases for future nodes, that could have been a factor in the bonus decision. Management was likely hearing from manufacturing partners about cost structure and supply outlook.

Market Maturity and Buyer Power: The Customer Perspective

From the smartphone maker's perspective, the dynamics are equally brutal. Apple, Samsung, Xiaomi, OPPO, Vivo—all of these companies face:

- Slowing unit growth (smartphones as a category aren't growing)

- More intense competition on price and features

- Supply chain fragmentation (needing different suppliers for chips, DRAM, NAND, cameras, screens, batteries, etc.)

- Cost pressure from components like DRAM and NAND

- Pressure to launch new models regularly without meaningful performance differentiators

In this environment, they're consolidating suppliers and increasing their leverage. If MediaTek can't offer attractive terms or guaranteed allocation, phone makers switch to Qualcomm or design their own processors (as Apple does).

This buyer power is real and translates into pricing pressure on MediaTek. When customers have leverage, suppliers have to accept lower margins or lose share. MediaTek's bonus cut is an acknowledgment that they're seeing this pressure in real-time.

The smartphone market is dominated by a few key players, with Apple and Samsung leading. Estimated data reflects competitive pressures and market dynamics.

Semiconductor Industry Cycle: Where We Are Now

The semiconductor industry is cyclical. Boom periods (high demand, tight supply, rising prices, expanding margins) alternate with downturns (excess capacity, weakening demand, price competition, margin compression).

The industry experienced a boom from 2020-2021 (pandemic-driven demand, supply constraints from COVID). Then a partial downturn in 2022-2023 as inventory normalized. Then partial recovery in 2023-2024 as AI drove data center demand. Then mixed signals in 2025 as smartphone and PC markets remained weak while data center remained strong but had some pullback cycles.

Where are we now? Probably in the early-to-middle stages of a mature cycle where:

- Smartphone and PC markets are saturated and flat

- Data center demand is strong but more predictable (not explosive)

- Memory (DRAM, NAND) supply is tight but improving

- Margins are compressed relative to boom periods

- Competition is fierce

In this environment, fabless designers like MediaTek feel the pain acutely because they're dependent on consumer device markets (smartphones, PCs) that are mature. The bonus cut is consistent with that cycle position.

Projections for H2 2025 and Beyond: What's Expected

Industry analysts are roughly aligned on the 2025-2026 outlook:

Smartphone shipments: Expect roughly 1.2-1.3 billion units in 2025, flat to slightly declining in 2026. Premium segment growth will be modest. Volumes will come from budget and mid-range, where margins are thin.

DRAM pricing: Expected to decline modestly through late 2025 and into 2026 as new capacity comes online. But prices will remain higher than pre-shortage levels. Memory makers have learned not to over-build and crash prices.

NAND pricing: Similar trajectory—declining from current levels but not back to pre-shortage prices. 3D NAND layering continues to improve density, but pricing competition remains.

Processor pricing: Likely to remain competitive. Qualcomm, MediaTek, and others will all fight for share in a flat market, which means price competition. Margins stay compressed.

Bonus outlook: Companies across the industry are likely to remain conservative on compensation through 2026. Bonuses may stabilize but probably won't bounce back to 2024 levels for at least a year.

MediaTek's bonus cut is actually positioning them conservatively but realistically for this environment. Management is saying: "We expect this to be tough, and we're preparing accordingly."

What This Means for Chip Designers and Engineers Globally

The ripple effects of MediaTek's bonus cut extend beyond the company itself. It's a signal to the entire semiconductor industry about margin outlook and compensation trends.

For chip designers and engineers working at other fabless companies, the message is: expect bonus pressure in 2025-2026. This probably affects NVIDIA less (data center strength), but it could affect Broadcom, Marvell, and others more. Salary growth will probably slow. New hiring will be more selective.

For engineers considering career moves, this is a reality check: the semiconductor boom of 2021-2024 is moderating. Job security is probably still good (skilled engineers are still in demand), but compensation growth is slowing. The days of explosive stock option upside and massive bonuses are probably behind us for a few years.

For students considering semiconductor careers, the industry is still attractive long-term, but the short-term outlook (next 2-3 years) is more conservative than the hype around AI chips might suggest.

Strategic Implications: What MediaTek Needs to Do

MediaTek's real challenge isn't just navigating 2025-2026 margin pressure. It's positioning for future growth when smartphone market dynamics eventually stabilize.

Options:

-

Accelerate automotive segment - Automotive chips are growing, have higher margins, and are less commodity-like. But automotive requires different design approaches (higher reliability, longer lifespans, safety certifications) and have long sales cycles.

-

Expand IoT and edge AI - Edge AI is hot. But competing against NVIDIA, Google, and others in edge computing is tough. MediaTek has advantages in low-power IoT but struggles in AI performance per watt against specialized competitors.

-

Licensing and IP monetization - Qualcomm makes significant revenue from patent licensing. MediaTek could expand this, but their patent portfolio is smaller.

-

Data center processors - This is where the growth and margins are. But NVIDIA, AMD, and others dominate. MediaTek would need transformational R&D investment and customer relationships they don't currently have.

The bonus cut suggests management is being disciplined about capital allocation while they figure out the long-term strategy. They're not panicking, but they're not betting the farm on immediate recovery either.

Employee Morale and Organizational Health

A 15.7% bonus cut is substantial enough to affect morale but not so draconian that it triggers mass exodus. MediaTek's likely scenario is:

- Some attrition among top performers who have other options

- Slight pullback in external hiring or hiring freeze for non-critical roles

- More conservative promotion cycles

- Heightened attention to project ROI and resource allocation

- Possible internal reorganization to reduce headcount or consolidate roles

Organizations that cut bonuses usually follow with other belt-tightening measures. MediaTek will probably be more selective about travel, consulting engagements, training budgets, and contractor usage.

From an organizational health perspective, the company is essentially saying: "We're in a defensive posture. We're protecting our cash. We're preparing for lean times." That's a legitimate strategic choice in a market facing the headwinds MediaTek is facing.

Capital Allocation and R&D Investment Implications

One question investors ask when companies cut compensation: does this mean they're also cutting R&D?

Not necessarily. Companies can cut bonuses while maintaining R&D budgets if they believe R&D is critical to future competitiveness. MediaTek's Dimensity 9600 development continued despite the bonus cut, suggesting they're protecting R&D investment even as they reduce compensation.

But capital allocation does get more conservative. Projects with uncertain ROI get scrutinized more carefully. Partnerships and joint development efforts are evaluated more rigorously. It's a slowdown in risk-taking, not a halt to innovation.

This makes sense given MediaTek's position: they need advanced processors to stay competitive, but they also need to preserve cash given uncertain demand outlook. Cutting bonuses lets them do both.

Looking Forward: Recovery Timeline

When will MediaTek restore bonuses to H1 2025 levels or higher? Probably not until 2026 at the earliest, and more likely 2027 if:

- Smartphone market stabilizes and shows growth or strong profitability

- DRAM and NAND supply normalize and costs stabilize

- Margin pressure eases across the industry

- MediaTek's product mix shifts toward higher-margin segments or new markets

Short-term (rest of 2025): Bonus cuts likely remain. No improvement expected.

Mid-term (2026): Possible stabilization. If market conditions don't worsen, bonuses might return to H2 2025 levels, but probably not to H1 2025 levels.

Longer-term (2027+): Recovery would require demonstrable market recovery or MediaTek's successful diversification into new segments with better margins.

The timeline suggests that MediaTek's management is expecting challenging conditions to persist through 2026. They're not anticipating a quick snap-back. This is consistent with their public guidance and with broader industry expectations.

The Broader Semiconductor Industry Health Check

MediaTek's bonus cut is a valuable data point for understanding semiconductor industry health. Here's what it tells us:

Supply chain normalization is real but uneven: DRAM and NAND are tight, but the shortage isn't as acute as 2021-2022. However, normalization is creating pricing pressure rather than relief.

Demand remains weak in consumer electronics: Smartphone and PC markets aren't showing growth momentum. Replacement cycles are extending. This creates headwind for companies dependent on these markets.

Margins are under pressure across the board: Not just at MediaTek, but across the fabless and foundry ecosystem. Companies are all fighting for share in flat or declining markets.

Data center remains the bright spot: But even data center demand has pullback cycles, and companies are being careful not to over-invest in capacity or over-promise growth.

Geopolitics adds uncertainty: Taiwan-based companies face additional strategic uncertainty that affects capital allocation and compensation decisions.

For investors, MediaTek's bonus cut is a yellow flag but not a red flag. The company isn't in distress. They're being prudent in a challenging environment. But it's a signal that near-term growth is unlikely.

Comparing to Historical Cycles: Is This Normal?

Bonus cuts during downturns are actually normal in the semiconductor industry. Companies that cut bonuses in 2020 (during the initial COVID shock) and 2022-2023 (during the inventory normalization downturn) both recovered with bonus increases by 2024.

MediaTek's situation in 2025 is different because the downturn isn't cyclical in the traditional sense. It's structural. Smartphones are maturing. Commodity competition is increasing. This isn't a temporary shortage followed by recovery. It's a new normal of slower growth and thinner margins.

Historically, that translates to longer periods of bonus depression. A cyclical downturn might last 12-18 months. A structural shift could take 3-5 years for compensation to fully normalize.

So comparing MediaTek's situation to 2020 or 2022 might be misleading. A better comparison is to companies in mature industries (like automotive semiconductors in the 1990s-2000s) where margins compressed permanently and compensation growth stalled for years.

Conclusion: Preparing for New Realities

MediaTek's 15.7% bonus cut is a lot more than just a compensation reduction. It's management saying: "The era of explosive smartphone chip growth is over. We're preparing for a different future."

That future is probably characterized by:

- Flatter smartphone markets with extended upgrade cycles

- Thinner margins from commodity competition

- More importance of non-smartphone segments (automotive, IoT, edge AI)

- Greater reliance on design innovation rather than volume growth

- Persistent supply chain complexity and cost pressure

For MediaTek employees, it's a reality check: the good times of 2021-2024 won't repeat in the near term. For industry investors, it's a signal that fabless designers dependent on consumer electronics will face margin pressure through at least 2026. For the semiconductor ecosystem, it's evidence that the post-COVID normalization is complete, and the industry has settled into a new equilibrium.

The bonus cut is not a disaster. MediaTek will survive and eventually recover. But it's an honest acknowledgment of where the market is and where it's headed. Other companies should probably be paying attention.

FAQ

What caused MediaTek to cut employee bonuses in 2025?

MediaTek reduced H2 2025 bonuses by 15.7% due to margin pressure created by tight DRAM and NAND supply, slowing smartphone market growth, and component cost inflation. These factors compressed profit margins and forced the company to be more conservative with compensation while maintaining R&D investment in advanced processors like the Dimensity 9600.

How significant is the 15.7% bonus reduction for MediaTek employees?

The reduction means eligible employees receive approximately NT

Why do DRAM and NAND shortages impact MediaTek's profitability?

MediaTek designs smartphone processors but doesn't manufacture them; they rely on TSMC for production. When DRAM and NAND become scarce, smartphone makers face higher component costs and must reduce production or lower margins, which decreases demand for MediaTek's chips. Additionally, if MediaTek bundles memory components with processors, the cost increases flow directly to their bill of materials and compress margins.

What percentage of MediaTek's revenue comes from smartphones?

Smartphone chipsets accounted for approximately 59% of MediaTek's Q4 2025 revenue, making the company heavily dependent on a single market segment. This concentration creates vulnerability when smartphone markets face headwinds, as the remaining business segments (IoT, automotive, other) cannot absorb the margin pressure.

Will MediaTek's Dimensity 9600 processor offset margin compression?

The Dimensity 9600, expected on a 2nm process, will improve performance and efficiency, but won't automatically solve margin issues. While advanced lithography provides real benefits, all competitors (including Qualcomm) will also move to advanced nodes, reducing the performance differentiation. Margins depend more on volume, scale, and supply chain security than on technology node alone.

Is the smartphone market expected to grow in 2026?

Analysts project smartphone shipments to remain flat or slightly decline in 2026, with growth coming primarily from budget and mid-range segments where margins are thinner. The market is maturing with extended upgrade cycles, particularly in developed countries with high smartphone penetration. This structural shift explains why MediaTek expects challenging conditions to persist.

How does MediaTek's bonus cut compare to other chipmakers?

While MediaTek's cut is among the most publicly visible, other semiconductor companies are also tightening compensation due to similar margin pressures. However, companies with more diversified business (like Qualcomm, AMD, or Broadcom) have more resilience. MediaTek's concentration on smartphones and fabless design makes it more vulnerable to consumer electronics market weakness.

When will MediaTek restore bonuses to previous levels?

Bonus recovery is unlikely before 2026 at the earliest, and more realistically 2027 if smartphone markets stabilize, DRAM/NAND supply normalizes, and MediaTek's margins improve. Unlike cyclical downturns that last 12-18 months, the structural challenges MediaTek faces could extend margin pressure for 3-5 years, making long-term bonus restoration uncertain.

What are the geopolitical factors affecting MediaTek's outlook?

MediaTek is Taiwan-based and manufactures through TSMC, also in Taiwan. U.S.-China trade tensions, export restrictions on advanced semiconductors, and uncertainty about Taiwan's status all create strategic risk that makes management more cautious with capital allocation, hiring, and compensation. Geopolitical uncertainty reinforces conservative positioning in an already challenging market.

Could the bonus cut trigger significant employee attrition at MediaTek?

A 15.7% reduction is substantial enough to trigger some attrition among top performers with alternative opportunities, but probably not mass exodus. However, the cut signals management's expectation of tough conditions ahead, which could affect long-term retention, hiring plans, and organizational morale. Companies typically follow bonus cuts with other cost-reduction measures like hiring freezes or headcount consolidation.

Key Takeaways

- MediaTek cut H2 2025 bonuses by 15.7% for 12,000 employees, averaging NT30,247.74), signaling expectation of sustained margin pressure through 2026.

- DRAM and NAND supply shortages combined with smartphone market maturity created cost pressure and demand uncertainty that compressed profit margins industry-wide.

- Smartphone chipsets represent 59% of MediaTek's revenue, creating vulnerability to market downturns and limiting ability to absorb margin pressure from other business segments.

- The Dimensity 9600 2nm processor represents technological advancement but won't solve margin issues since all competitors are moving to advanced nodes, eliminating performance differentiation.

- Smartphone market is structurally maturing with extended upgrade cycles, flat unit growth projections for 2026, and competition concentrated in lower-margin budget and mid-range segments.

- Supply chain cascade effect means memory component shortages propagate upstream to chip designers through reduced device manufacturer demand and compressed BOM costs.

- The bonus cut is not panic-driven but signals management's preparation for a new normal of slower growth and thinner margins persisting through 2027.

Related Articles

- RAM Shortage Crisis 2026: How Memory Scarcity Could Bankrupt Companies [2025]

- Lenovo Warns PC Shipments Face Pressure From RAM Shortages [2025]

- Steam Deck Out of Stock 2026: What RAMaggedon Means [2025]

- Why Samsung's Galaxy S26 Faces Massive Hype Crisis [2025]

- AMD's Strong Financial Results Despite PC Market Decline [2025]

- Nvidia RTX 50 Super Delayed: RTX 60 Series May Miss 2027 [2025]