![YNAB Budgeting App: Take Control of Your Money [2025]](https://tryrunable.com/blog/ynab-budgeting-app-take-control-of-your-money-2025/image-1-1769370023340.jpg)

Introduction: The Money Problem Nobody Talks About

You know that feeling when you check your bank account and have no idea where the money went? Last month,

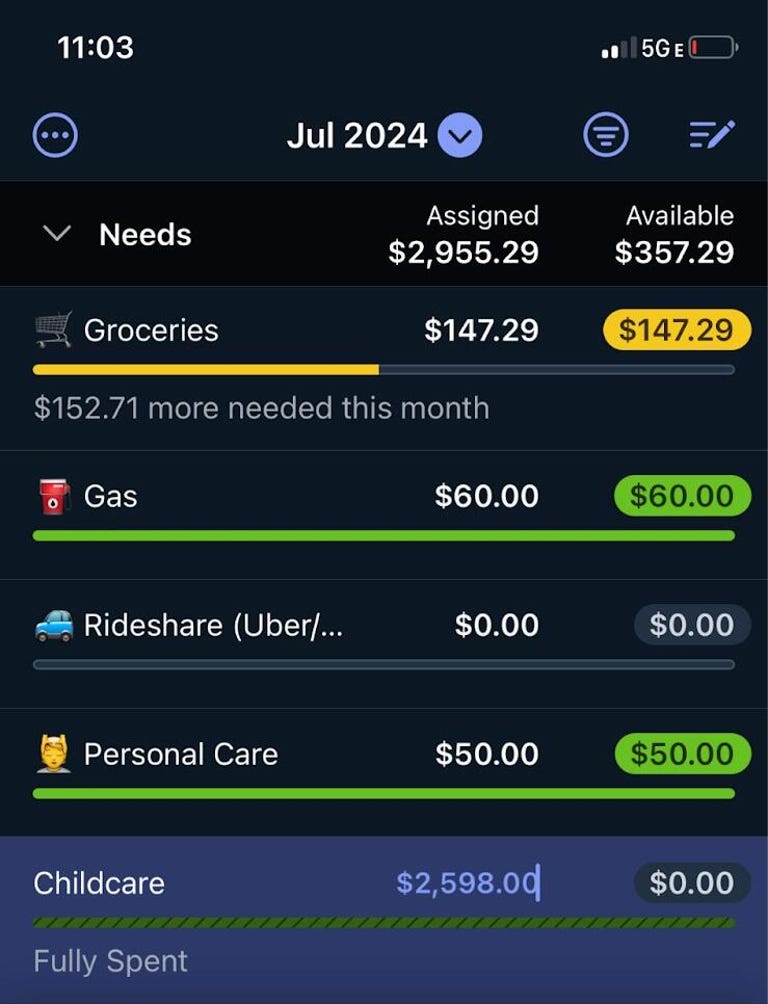

This is the reality for millions of people. According to recent surveys, about 73% of Americans don't have a clear budget, and 56% of people would struggle to cover a $1,000 emergency with cash on hand. Not because they're irresponsible—but because nobody taught them how to actually manage money. We're expected to figure it out ourselves.

That's where most budgeting apps fail. They show you a pie chart of where you spent money last month. Cool. But that doesn't help you decide where to send money next month. That doesn't change behavior. That doesn't give you control.

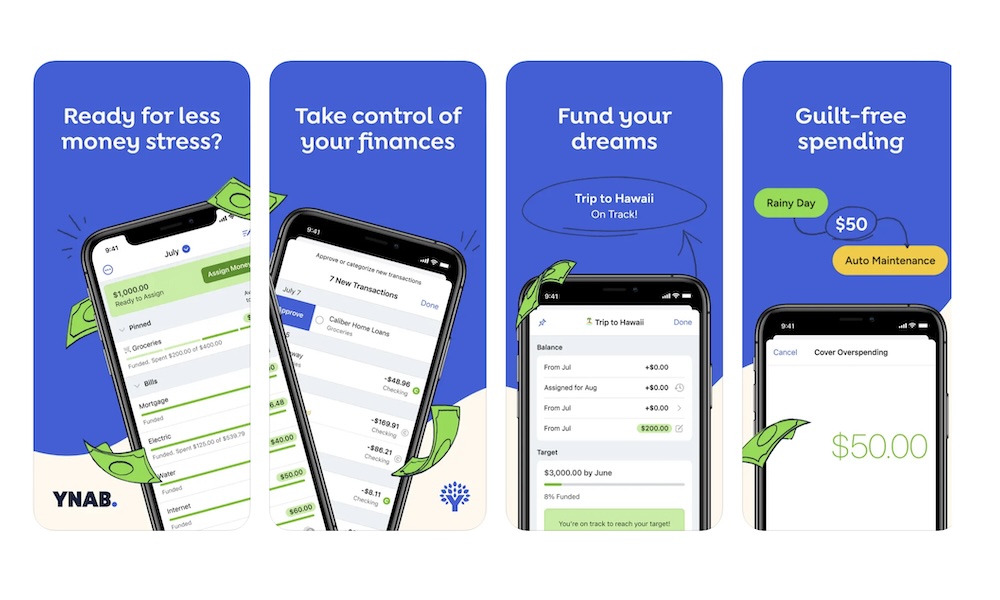

Then there's YNAB (You Need A Budget), which takes a completely different approach. Instead of tracking what you've already spent, it teaches you to allocate money intentionally before you spend it. It's radical. It's counterintuitive. And it actually works.

I've been using YNAB for about eighteen months. I'll be honest—the first three weeks were annoying. But somewhere around week four, something clicked. I stopped having anxiety about money. Not because I became rich. But because I knew exactly where every dollar was going, and I made that decision consciously.

This article isn't a sales pitch. It's a breakdown of what YNAB actually does, how it works, and whether it's worth your time and money. I'll show you the good stuff, the friction points, and how it compares to other budgeting tools. You'll understand if this is the right fit for your life.

TL; DR

- YNAB's Core Method: "Give every dollar a job" forces intentional spending decisions before money leaves your account

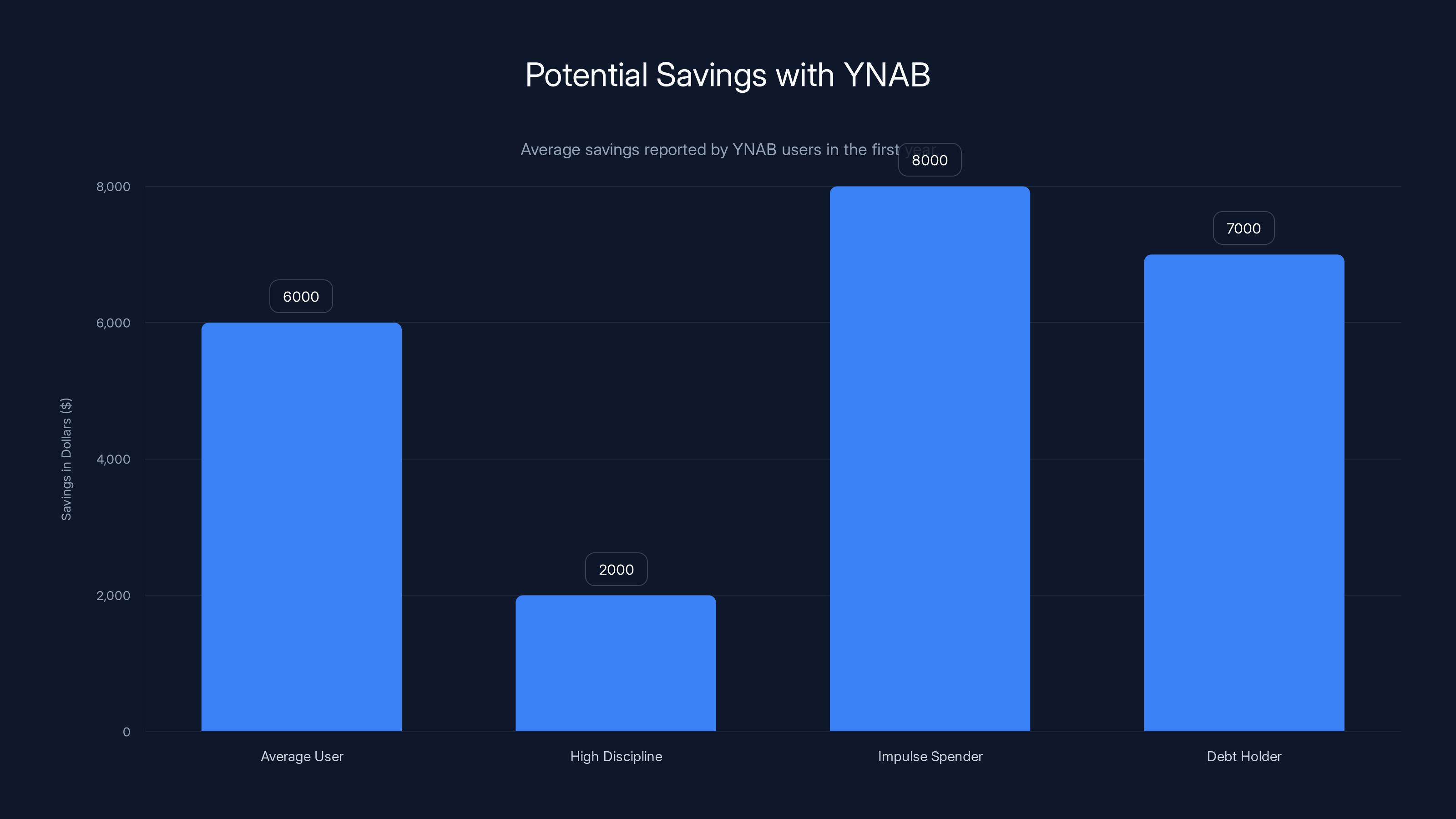

- Real Financial Impact: Users report average savings of $6,000+ per year after using the app for six months

- Learning Curve: Takes 2-4 weeks to grasp the methodology, but payoff is significant

- Pricing Model: 155 annually) with a free 34-day trial

- Best For: Anyone struggling with impulse spending, debt payoff, or lack of spending visibility

YNAB users report an average savings of $6,000 in the first year. Savings vary based on financial discipline and spending habits. Estimated data.

How YNAB Actually Works: The "Give Every Dollar a Job" Philosophy

Most budgeting apps work backward. You spend money, then the app categorizes it. YNAB flips this completely.

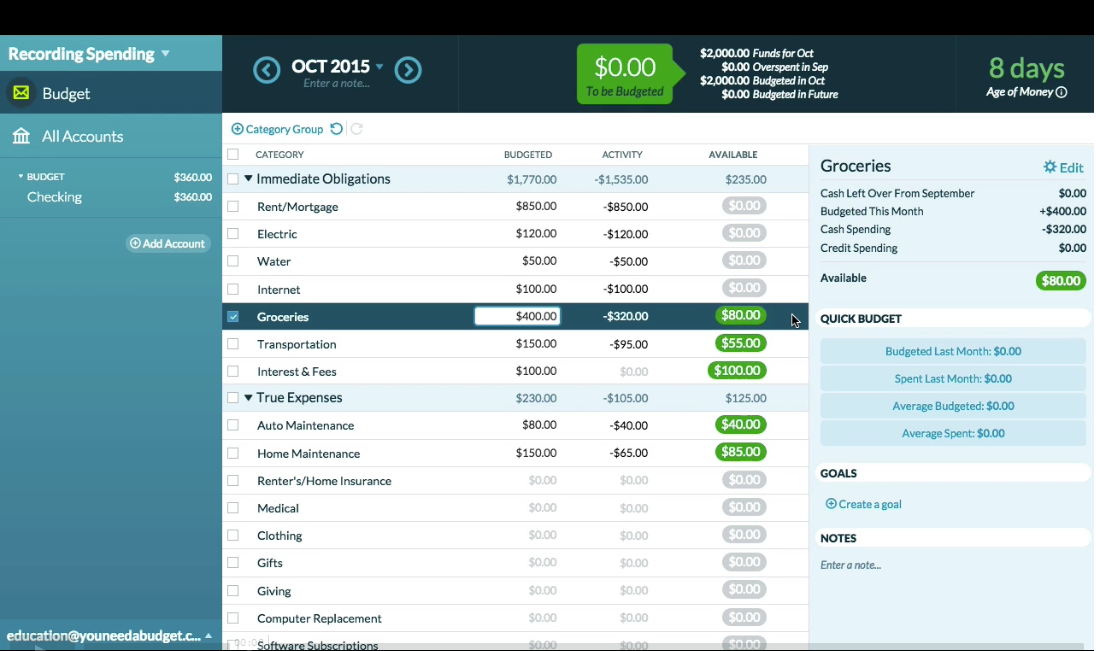

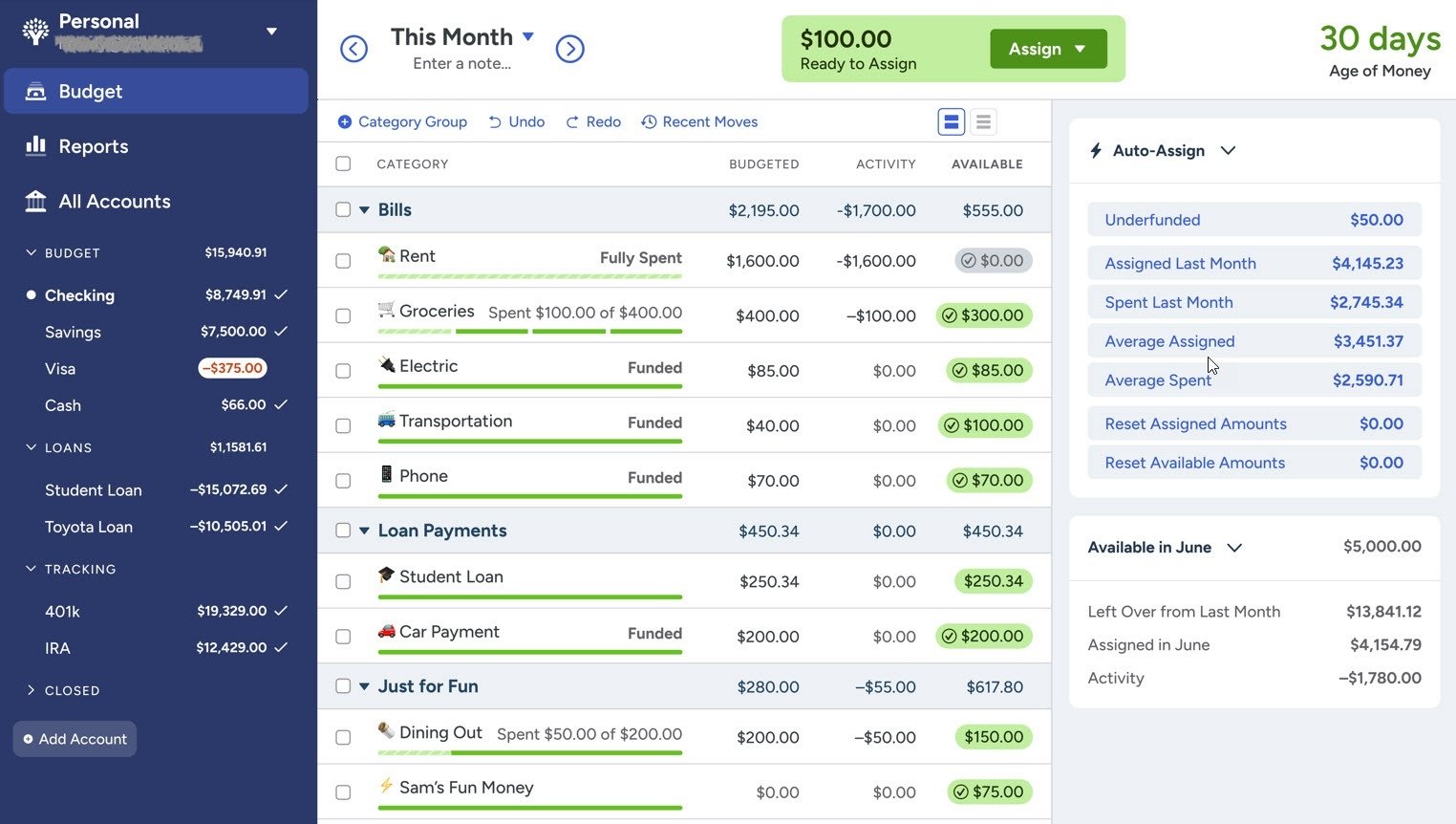

The core concept is called "give every dollar a job." Here's how it actually functions: You log into YNAB, you see your available money (what you have right now, not what you will have). Then you actively assign that money to categories. Rent gets

Now here's the critical part: when you spend money, the app pulls from that budget. Spent

This single change destroys impulse spending.

Why? Because suddenly, spending

The second pillar of YNAB is called "rule two: embrace your true expenses." This is where most people find unexpected value. You have annual expenses that don't come up every month. Car insurance. Holiday gifts. Annual subscriptions. Medical deductibles. Most budgeting systems ignore these until they hit you and cause panic.

YNAB forces you to map them out. You know car insurance costs

The third rule is "roll with the punches." Budgets break. Life happens. Your car breaks down. You have an unexpected medical bill. YNAB doesn't shame you for this. Instead, you adjust. You move money from another category. You see the trade-off in real time. Maybe you reduce entertainment spending for a month to cover it. Or you delay something non-urgent. You're making the decision, not reacting to it.

The Real Financial Impact: Numbers People Actually See

YNAB publishes annual data about what users achieve. In their 2024 report, they found that the average YNAB user saves $6,000 in their first year. That's not theoretical. That's actual users tracking real money.

How does this happen? Not because the app is magic. But because it forces behavior change.

Let me break down what typically happens in month one of using YNAB: You discover your actual spending. Most people are shocked. That

In month two, you start making adjustments. Maybe you cancel two streaming services. That's

These aren't drastic changes. You're not eating ramen or living like a hermit. You're just becoming conscious about where money goes. And small adjustments compound.

But the real impact for most users isn't just cutting spending. It's intentionality. Someone using YNAB might keep their subscription services, reduce coffee spending, and instead put an extra $300/month toward debt payoff. Same net savings, but aligned with their actual priorities.

For people in debt, the results are more dramatic. Users report paying off credit cards 2-3x faster than they were before. Why? Because the app makes the math impossible to ignore. You see that

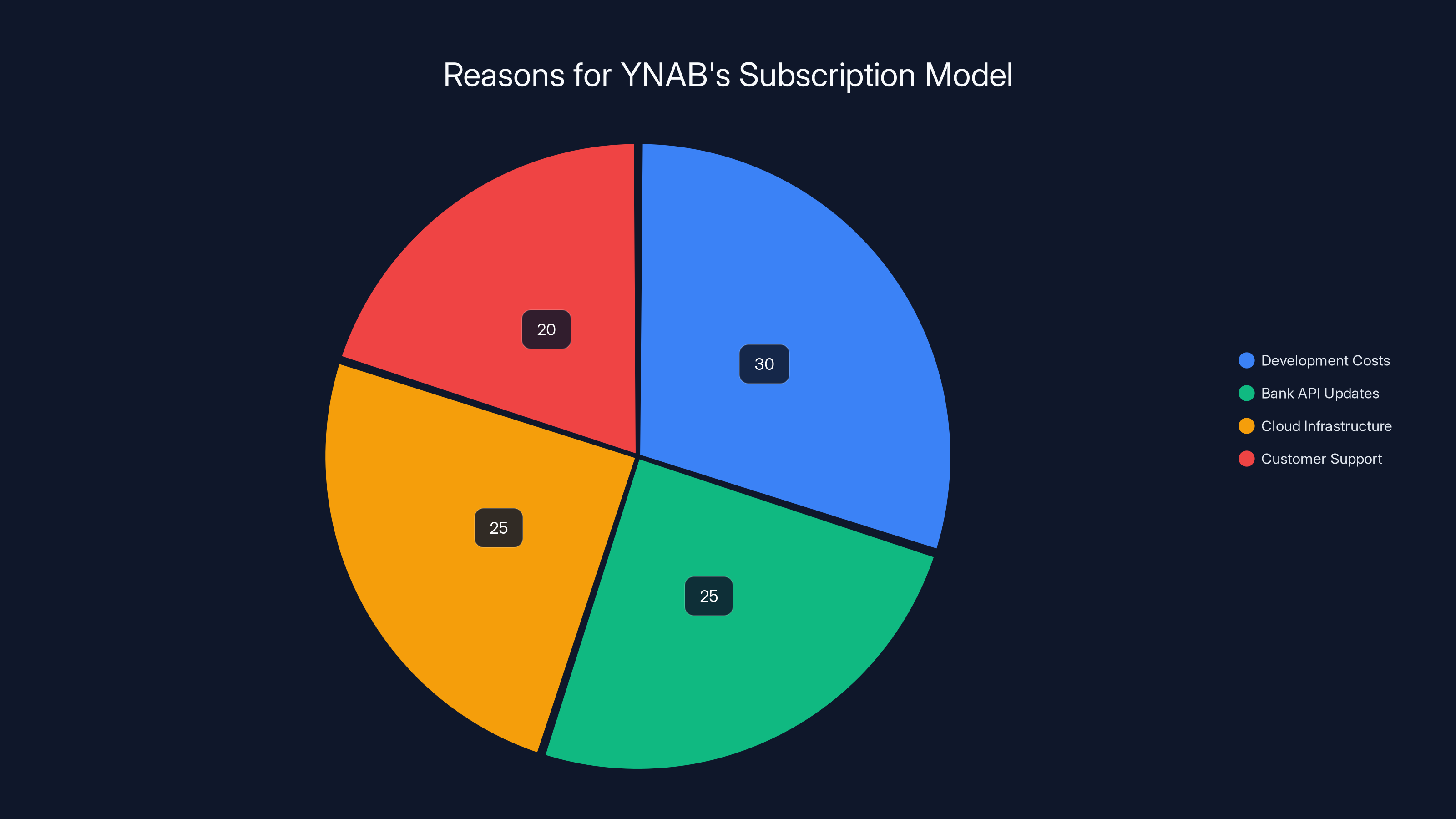

Estimated data shows that development costs and cloud infrastructure are the largest components of YNAB's ongoing expenses, justifying the subscription model.

Setting Up YNAB: The First Three Weeks (It's Awkward)

Let's be honest about the onboarding experience. It's not seamless. It requires work. But it's necessary work.

Day one: You connect your bank accounts. YNAB syncs with most major US banks, plus international banks depending on your location. The integration is smooth. Within five minutes, your transactions start populating in the app.

Days one through three: You start logging transactions. For the first few days, this feels tedious. Every coffee purchase. Every gas fill-up. Every grocery trip. You'll probably forget a few and have to go back through your banking app to find them. It's friction.

But here's the thing: this friction is intentional. The app is teaching you to be aware of your spending. By day four or five, you start noticing patterns. You realize you're spending more on food delivery than you thought. You see that Target trip became three Target trips.

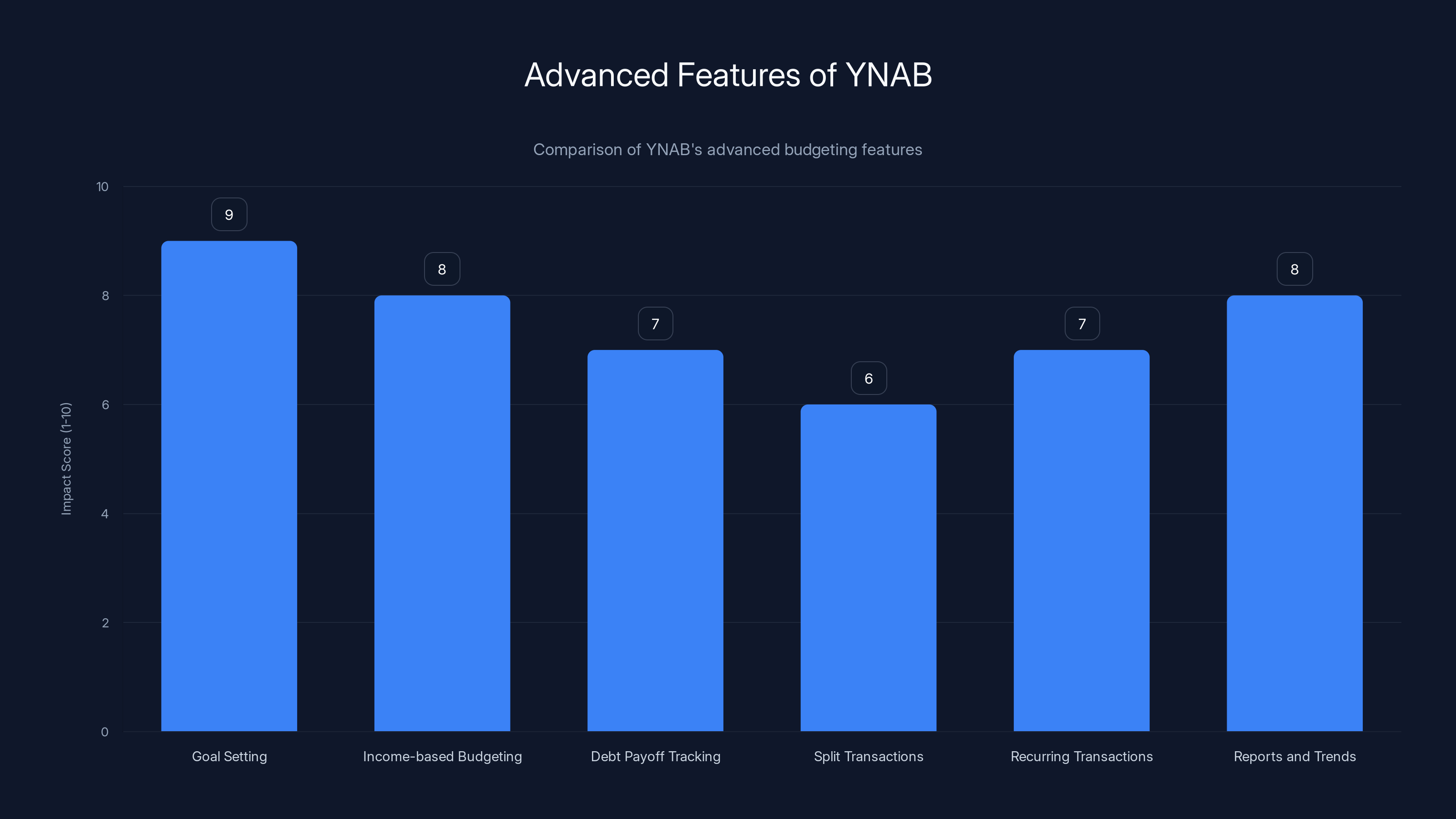

Days four through seven: You start setting up categories and assigning your first budget. This is where YNAB differs from competitors. You're not just selecting "Groceries" from a preset list. You're thinking about what you actually need for groceries this month. Are you meal-prepping? Did you stock up? Do you have guests coming? You set a realistic number.

Days eight through fourteen: You're actively budgeting. You assign money to categories as it comes in. Some income arrives. You decide:

Days fifteen through twenty-one: You've made your first adjustments. You realized you set entertainment too low. You moved $50 from "miscellaneous" to entertainment. You're rolling with the punches.

By day twenty-two, most users have the "ah-ha" moment. The system clicks. Suddenly, the friction becomes features. That transaction log? You love it. That forced categorization? It's revealing. That reminder that you only have $43 left in your entertainment budget? It's preventing a stupid purchase.

The free trial lasts 34 days. This is strategically longer than it takes to see value, but short enough that you need to commit. Most people who make it past day fourteen will buy the subscription. Most people who don't understand it by day fourteen will never get it.

The YNAB Interface: Beautiful and Confusing

Design-wise, YNAB is gorgeous. The app and web version are clean. The color scheme is minimal. The interface is organized. It's not cluttered like some finance apps that try to show you everything at once.

But beautiful doesn't mean intuitive. Not immediately.

The main budget view shows your categories and how much you have available in each. This part is clear. Groceries:

The accounts section shows your bank balances. Again, clear.

The transactions section is where it gets dense. You're looking at a list of every purchase, sorted by category, with the ability to assign transactions, split them across categories, or flag them. For someone new to budgeting, this is a lot. But for someone who wants control, it's powerful.

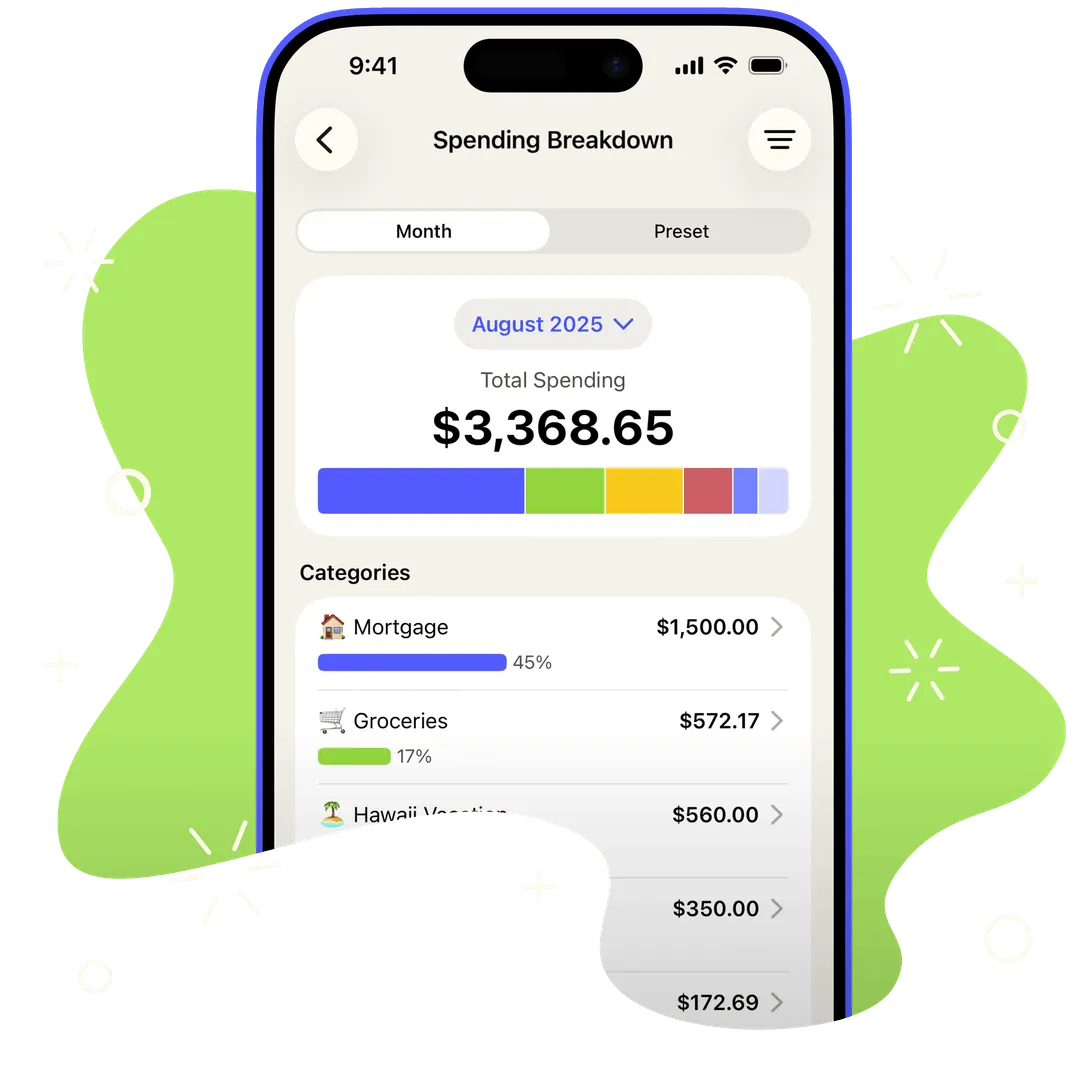

The reports section shows trends over time. How much you typically spend on groceries. How your entertainment spending varies by month. What percentage of income goes to debt versus discretionary spending. These are useful insights, but they're secondary to the budgeting function.

One notable friction point: the mobile app is good, but the web version is better. If you're primarily a phone user, some of YNAB's power gets lost. You can add transactions and see your budget, but detailed category management and report generation work better on desktop.

Also worth noting: the app's syncing is based on when you open it and is not always instant. If you spend money and immediately check the app, that transaction might not show up for a few minutes. This is intentional design—YNAB wants you to manually log transactions so you stay engaged, not just auto-categorize everything and forget about it.

YNAB vs. Other Budgeting Apps: How It Actually Compares

Let's talk competitors. There are dozens of budgeting apps out there. Here's how YNAB stacks up.

Versus Mint (or its replacement, Credit Karma Money): Mint is free. YNAB costs $12.99/month. Mint shows you where you spent money. YNAB tells you where to send money next. Mint is reactive. YNAB is proactive. For someone just starting to track expenses, Mint works fine. For someone serious about behavior change, it falls short. Also worth noting: Mint was shut down in January 2024 and transitioned to Credit Karma Money, which is still developing its feature set.

Versus Every Dollar: Every Dollar uses a very similar methodology to YNAB—allocate every dollar. It's free with limitations, or $12.99/month for the full version. The main difference? Every Dollar is simpler, with fewer features and less customization. Good for beginners. Less powerful for complex financial situations.

Versus Nynab (I'm kidding, but it's a real alternative): Okay, not a real app name. But "Old YNAB" was a software tool people paid $15 to download once, and it still has users. New YNAB is cloud-based and subscription-based. Some loyalists prefer the old version. Most new users prefer the cloud version because it syncs across devices seamlessly.

Versus spreadsheets: Yes, people budget with spreadsheets. If you're disciplined and enjoy Excel, you can build a custom budget system. But this requires manual transaction logging, manual categorization, and manual updates. Spreadsheets don't sync with your bank. They don't send alerts. They don't show you spending trends. YNAB is a spreadsheet with automation and behavioral design built in.

Versus Goodbudget: Goodbudget is a free app that mimics the envelope budgeting method. You get virtual envelopes, you allocate money, you spend. It's simpler than YNAB, free, and works well for couples because it syncs across devices. The downside: it doesn't connect to your bank, so you're manually logging everything. And it has fewer reporting features.

Versus You Need A Budget's competitors from fintech startups: There are newer apps like Copilot, Rocket Money, and Qapital that offer budgeting with different angles. Some focus on savings goals. Some focus on investing. Some focus on bill management. YNAB is purely budgeting-focused. It's not trying to be an all-in-one finance app. This is actually a strength—it does one thing exceptionally well.

The honest take: YNAB isn't the cheapest option. It's not the most advanced. But the methodology it teaches is the most effective at changing spending behavior. You're not paying for software. You're paying for a system that works.

A significant 73% of Americans lack a clear budget, and 56% would struggle with a $1,000 emergency, highlighting widespread financial management challenges.

The Cost-Benefit Analysis: Is YNAB Worth $12.99/Month?

Let's do the math directly.

YNAB costs

But the real question isn't average. It's: will you save money using YNAB?

If you're already disciplined with money, keep a manual budget, and don't have spending leaks, YNAB won't help much. You'll pay $130/year for something you're already doing.

If you're spending money without visibility, have debt you want to pay off faster, or struggle with impulse purchases, YNAB will almost certainly pay for itself within the first month.

If you're somewhere in the middle—you have some spending awareness but not total control—YNAB is likely worth it, but the value depends on whether you'll actually use it.

Here's the psychological component: you're paying for the app monthly. This subscription cost creates what economists call "sunk cost attention." You've paid for YNAB, so you're more likely to actually use it. You'll log transactions. You'll check your budget. You'll adjust categories. You wouldn't do this with a free app because there's no psychological investment.

For the first month or two, YNAB might feel expensive. You're paying to spend time logging transactions and setting up categories. But by month three, when you realize you've naturally reduced spending by

Real User Stories: What Actually Happens

Let me share some real scenarios I've seen or directly experienced.

Scenario one: The impulse spender. Sarah had a habit of buying things online when stressed. Sometimes she'd spend

Scenario two: The debt carrier. Marcus had

Scenario three: The couple with money stress. James and Lisa fought about money constantly. They had no idea where money was going. One was trying to save, one was spending. YNAB forced a conversation: "What are our priorities?" They could see exactly where money went. They negotiated. Streaming services:

These aren't success stories in the sense of "YNAB made them rich." They're success stories in the sense of "YNAB gave them control and visibility." And that changes everything.

Mobile vs. Desktop: Where YNAB Shines and Where It Struggles

The YNAB app comes in three forms: iOS, Android, and web. Each has strengths.

The iOS and Android apps are excellent for on-the-go transaction logging. You buy a coffee. You open the app. You tap "Add transaction." It defaults to today's date, your most recent merchant, and asks you to confirm the amount. Takes fifteen seconds. This is where the magic happens—you're staying aware of spending in real time.

The apps also show your budget breakdown and category balances, so you know before you spend. About to go grocery shopping? Open the app, see that you have $340 in the grocery category, and shop accordingly.

Where the apps get limited: detail work. Setting up new categories? Much easier on desktop. Adjusting the budget structure? Better on desktop. Generating reports and analyzing trends? Way better on desktop. Reconciling accounts? Doable on mobile, but clunky.

The web version is full-featured. This is where serious budget work happens. You're on the couch with your laptop, looking at last month's trends, planning next month's categories, making adjustments to your budget strategy. It's where the system thinking happens.

One quirk: YNAB doesn't work great on tablets. It works, but the interface doesn't adapt well to larger screens. It's optimized for either mobile phones or desktop browsers, not the middle ground.

The syncing between versions is usually instant, but occasionally you'll log something on your phone, switch to the desktop, and it hasn't appeared yet. The lag is typically less than a minute, but for a real-time budget app, it's noticeable.

Estimated data shows that typical YNAB users can save significantly by adjusting spending habits, with potential annual savings reaching up to $3,600 through debt payoff.

The Learning Curve: How Long Until You Get It?

YNAB's learning curve is real. It's not like an Instagram app where you pick it up in two minutes. It requires thinking.

Week one: You're confused. You're not sure what categories you need. The distinction between budgeting and spending feels subtle and weird. You're spending time on this, and it's not clear why. This is the highest dropout point.

Week two: You're starting to get it, but you're not optimizing yet. You're setting up categories, logging transactions, trying not to mess it up. You're following the rules without understanding why.

Week three: The light bulb is getting brighter. You realize you have $40 left in entertainment and it's only the 25th. You make a conscious choice not to spend it. That choice doesn't feel like deprivation; it feels like power. You're starting to see the value.

Week four plus: You understand the system. You're making adjustments confidently. You're looking at trends. You're planning ahead. You've moved from confusion to mastery.

YNAB has recognized this and built a bunch of educational content to accelerate the learning curve. There are short videos (4-5 minutes each) on specific features. There's a "Getting Started" guide. There's an active community forum where people share strategies and ask questions. And there's the free 34-day trial, which gives you time to get through weeks one and two and decide if it's worth continuing.

The learning curve is steep compared to other budgeting apps, but it's not steep compared to, say, learning how to invest or understanding personal finance in general. You're looking at a 4-6 hour time investment to reach competence. Most of that is in week one.

Advanced Features: When YNAB Gets Powerful

After you grasp the fundamentals, YNAB has depth.

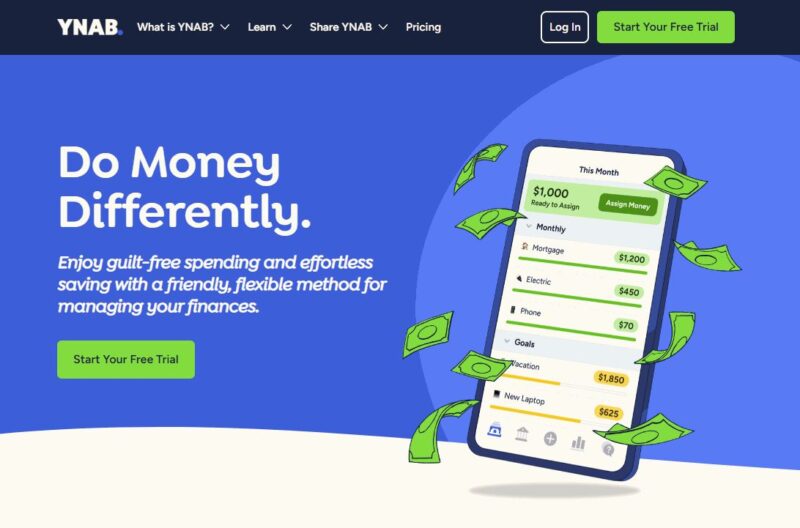

Goal setting: You can set goals for categories. Not just a monthly budget, but actual targets. "Save

Income-based budgeting: If you're freelance or have variable income, YNAB handles this differently. Instead of assuming the same income each month, you budget based on what actually comes in. Good month? Great, you allocate it. Slow month? You use what you budgeted from the previous month. This is where YNAB shines for freelancers and commission-based workers.

Debt payoff tracking: You can set a goal for debt reduction and watch the progress. Some people set a payoff date and work backward from there. YNAB tells you exactly how much extra you need to budget each month. Others just track the balance decline month to month and watch the progress. Both approaches work.

Split transactions: You spent $100 on groceries and gas in the same store visit. You can split that transaction 60/40 between groceries and transportation. This keeps your spending categories accurate and your insights valid.

Recurring transactions: Set up subscriptions or regular bills to auto-populate each month. They still show in your budget, but you're not manually logging them every month. You can edit or delete them, but YNAB handles the repetition.

Reports and trends: Over time, YNAB builds a database of your spending. It shows you average spending per category, how spending varies seasonally, where you have the most discretion, where you're most disciplined. This becomes powerful information for future planning.

Reconciliation: Each month, you can sync with your bank and make sure everything matches. YNAB shows you uncleared transactions (things you recorded but the bank hasn't posted yet) and flagged transactions (things in your bank account that YNAB doesn't know about). This keeps your system accurate and catches errors.

These features aren't essential for beginners. But once you've been using YNAB for a few months, they become standard workflow.

Common Mistakes People Make With YNAB

Just because you have the tool doesn't mean you'll use it correctly. Here are the most common missteps.

Mistake one: Over-budgeting. You set a grocery budget of

Mistake two: Not using the app regularly. You set it up, you're excited, you budget aggressively, and then you don't open the app for two weeks. You've had twelve purchases since then that aren't logged. You lose the real-time feedback loop. YNAB only works if you use it consistently. You need to log transactions daily or at least every few days.

Mistake three: Not being honest about what you spend. You love coffee, and you spend

Mistake four: Treating YNAB like a spending app instead of a planning app. YNAB is about deciding where money goes before you spend it. You get your paycheck, you budget it immediately. That's the power. If you wait until after you've spent to budget, you're just using it as an expense tracker. Most expense trackers will do that job fine. But for actual financial control, you need proactivity.

Mistake five: Ignoring the "true expenses" category. You know you have an annual car insurance bill. You know it's

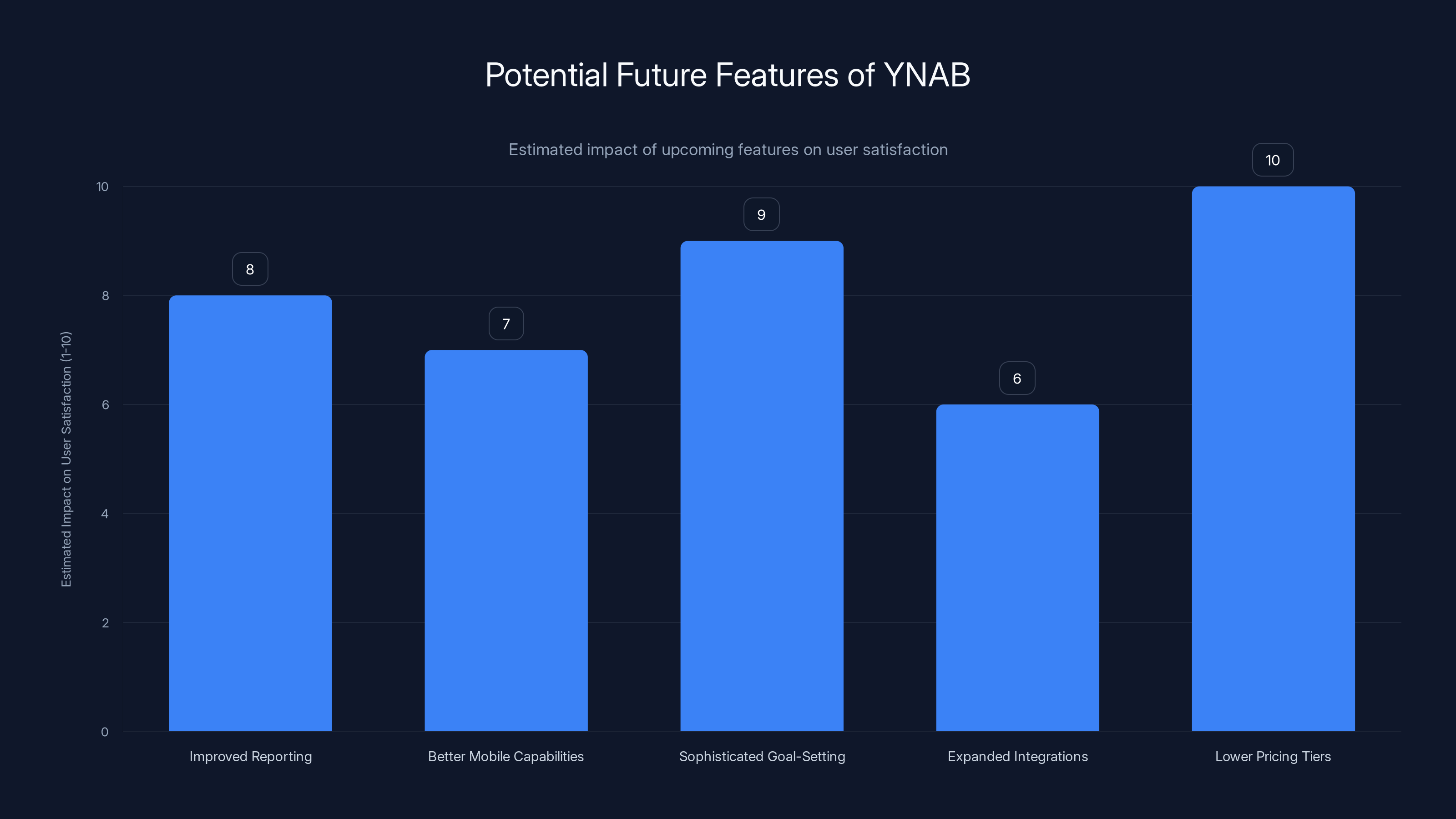

YNAB's goal setting and income-based budgeting features are highly impactful, scoring 9 and 8 respectively, for their ability to transform personal finance management. Estimated data based on feature descriptions.

YNAB for Different Life Situations

YNAB works for different scenarios, but the approach varies.

For students: You probably don't have regular income. YNAB can still help. You get financial aid or parent support in chunks. Budget that money for the semester. Track spending so you know when you're running low. For the first time, you see that beer money, food money, and textbook money all come from the same pool, and you have to choose.

For freelancers: Variable income makes budgeting hard, but YNAB shines here. You build up a buffer from good months and draw from it in slow months. You budget based on average expected income, then adjust when reality diverges. Many freelancers report that YNAB is the difference between financial stress and stability.

For couples: YNAB requires conversations about money. What are we prioritizing? How much should we spend on entertainment versus savings? These conversations are hard, but they're necessary. Once you're using YNAB together, you're literally looking at the same numbers. No more "I didn't know you spent that much." You both know. You both agreed to the budget. If spending has changed, you talk about it and adjust.

For single income earners: You earn money, you budget it, you spend it. The process is straightforward. Where YNAB adds value is visibility. You see exactly where every dollar goes. No surprises at the end of the month.

For FIRE enthusiasts: The "Financial Independence, Retire Early" community loves YNAB. You need to know exactly how much you spend to calculate your financial independence number. YNAB tracks this precisely. It's almost a mandatory tool in that space.

For high-income earners: If you earn six figures or more, you might think YNAB is for poor people learning to budget. Actually, many high-income earners use YNAB because they have complex finances. Multiple income streams. Investments. Tax planning. Charitable giving. YNAB helps them organize it all.

Privacy, Security, and Data: What You Should Know

YNAB has access to your financial data. This is important to think through.

The good news: YNAB uses bank-level encryption. Your bank login credentials are never stored on YNAB's servers. When you connect your bank, you're using a secure aggregation service (like Plaid) that encrypts the connection. YNAB sees your transactions, but not your password. This is industry standard for fintech apps.

The business model: YNAB makes money from subscriptions, not by selling your data. They have no incentive to monetize your financial information. Compare this to free budgeting apps, which might be tempted to sell anonymized spending data to marketers. YNAB's subscription model aligns their incentives with your privacy.

Data storage: Your data is stored on YNAB's servers, which are in the United States. If you're concerned about US-based data storage (particularly related to GDPR and European privacy), you should note this. YNAB does comply with GDPR, but your data physically resides in US data centers.

Account security: You can enable two-factor authentication on your YNAB account. This is standard but important. Use it.

Data retention: If you close your account, YNAB can export all your data to a CSV file. But after some period, your data is deleted from their servers. This is reasonable, but it means you're responsible for backups if you want historical records.

One thing worth considering: you're giving YNAB a complete picture of your spending. This is more exposure than most people give any service. If you're paranoid about financial data, you could manually log everything instead of connecting your bank. This defeats the purpose (the syncing is where much of the value is), but the option exists.

For most people, the security practices are solid. For people with significant security concerns, consider that no app is perfectly private, and decide if the benefits outweigh the risks.

Alternatives and Complementary Tools

YNAB doesn't exist in a vacuum. There are supporting tools and alternatives worth considering.

Every Dollar: Similar methodology, simpler interface, lower price point, less powerful. Good if YNAB feels overwhelming.

Goodbudget: Virtual envelope system, free, great for couples, requires manual transaction entry. Good for simplicity and avoiding subscriptions.

Monarch Money: A newer platform that combines budgeting, net worth tracking, and investing. More comprehensive than YNAB, higher price point. Good if you want everything in one place.

Rocket Money (formerly Truebill): Bills, subscriptions, and budget tracking in one place. Free tier available. Good if you're trying to manage subscriptions and budgets together.

Personal Capital: Portfolio tracking and wealth management with some budgeting features. Better for people with investments. Pricier.

Copilot: Mobile-first budgeting app, free tier with limitations. Good for people who prefer phone-based financial management.

Spreadsheets: Honestly, if you're disciplined and willing to maintain a spreadsheet, a well-built Excel budget beats any app because it's fully customizable. But it requires discipline and work.

Complementary tools: YNAB works well alongside investment apps like Vanguard or Fidelity, retirement planning tools, and tax software. It's not designed to replace them; it's designed to manage cashflow and behavioral spending.

Lower pricing tiers are estimated to have the highest impact on user satisfaction, followed by sophisticated goal-setting. Estimated data based on potential user interest.

The Subscription Model: Why YNAB Went Subscription-Based

Historically, YNAB sold software. You paid once, you owned it. In 2015, they transitioned to a subscription model. This caused uproar. People were furious. "Why am I paying monthly for software I used to buy once?"

It's worth understanding why they made this change, because it affects whether the subscription is sustainable for you.

Reason one: development costs are continuous. YNAB needs to maintain servers, update the app for new iOS and Android versions, maintain security infrastructure, and add features. These costs don't stop. A one-time purchase model couldn't sustain this.

Reason two: bank APIs change constantly. Banks switch security protocols. Regulatory requirements shift. YNAB's technical team is constantly updating integrations. This requires ongoing engineering resources.

Reason three: the app syncs data in real-time across devices. This requires cloud infrastructure. Storage, computation, redundancy. Again, continuous costs.

Reason four: customer support is ongoing. Someone needs to answer forum questions, respond to support tickets, handle edge cases. This is a recurring expense.

So the subscription model isn't a cash grab; it's a realistic reflection of the cost to deliver the service. That said, YNAB's pricing at $12.99/month is on the higher end for budgeting apps. Whether it's worth it depends on whether you'll actually use it and benefit from it.

Setting Yourself Up for Success With YNAB

If you decide to try YNAB, here's how to maximize your chances of success.

First: Before signing up, watch three of their educational videos. Specifically: "How to Budget," "Your First Budget," and "Making Your Budget." These are ten minutes total and will frame your expectations.

Second: Start during a time when you're not in crisis mode. You want headspace to think about budgeting, not stress about an immediate problem. YNAB is a system for long-term control, not a fire extinguisher for financial emergencies.

Third: Actually use the free trial. Don't just cancel immediately if you don't get it in the first three days. Give yourself the full 34 days. Most people need 2-3 weeks to see value.

Fourth: Start with broad categories. Don't try to create fifteen custom categories right away. Start with the basics: housing, food, transportation, utilities, debt, savings, and discretionary. You can refine later.

Fifth: Set a recurring reminder to budget. Once a week, spend fifteen minutes on YNAB. Check how much you have left in each category. Adjust if needed. This habit is what separates users who see results from users who abandon the system.

Sixth: If you use YNAB with a partner, have a weekly money date. Fifteen minutes, no distractions, look at the budget together. Celebrate wins (you came in under budget in groceries). Discuss struggles (entertainment spending was higher than planned). Make adjustments together.

Seventh: Connect your bank automatically, not manually. The friction of manual entry is actually a feature for keeping you engaged. But the syncing is too valuable to skip.

The Psychology of Behavioral Finance and YNAB

Why does YNAB work when so many other budgeting apps don't? It comes down to behavioral economics.

Loss aversion: Humans feel the pain of losing money about twice as intensely as the pleasure of gaining money. YNAB leverages this. When you see that your entertainment budget is

Decision fatigue: Every purchase decision is a decision. By the time you've made 2,000 small decisions in a month, your willpower is depleted. YNAB reduces decision fatigue by constraining your choices. You have $50 for entertainment. That's the frame. Decisions become easier when they're within a clear boundary.

Sunk cost effect: You paid for YNAB this month. This psychological investment makes you more likely to actually use it. You have skin in the game.

Commitment and consistency: Once you've publicly (or even just mentally) committed to a budget, you're more likely to stick to it. YNAB makes the commitment explicit. You've written down your plan. Sticking to it becomes a test of integrity.

Progress and momentum: Every dollar saved becomes visible. Watching your "emergency fund" category grow from

None of these are tricks. They're just how humans work. YNAB is designed around human psychology, not against it. This is why it works for changing behavior when spreadsheets don't.

Potential Downsides and Honest Critiques

I've been very positive about YNAB, but it's not perfect. Here are legitimate concerns.

Cost:

Learning curve: YNAB takes time to master. This is a feature, not a bug, in my opinion, but it's a real barrier. Some people won't put in the effort. They'll quit after two weeks.

Bank syncing isn't universal: If your bank isn't supported by YNAB's aggregation partners, you're logging transactions manually. This sucks. It defeats much of the purpose.

Mobile app limitations: The iOS and Android apps are good for logging transactions and seeing balances, but they're not full-featured. Serious work requires the web version.

The subscription model fatigue: If you use YNAB for five years, you've paid $775. At some point, some people feel like they should own the software, not rent it. This is a philosophical disagreement, but it's real.

Data dependency: Everything lives in the cloud. If YNAB goes out of business (unlikely, but not impossible), you lose access. You can export your data, but it's not the same as having it locally.

Privacy concerns: YNAB has a complete picture of your spending. If you're privacy-focused, this is uncomfortable, no matter how secure their infrastructure is.

These are real concerns. They don't make YNAB bad. But they're reasons some people choose alternatives.

How to Use YNAB With Other Financial Tools

YNAB plays well with others in a financial ecosystem.

Investment accounts: YNAB tracks your spending and income, not your investments. If you're using Vanguard, Fidelity, or Betterment, YNAB doesn't manage those accounts. You might connect them in YNAB for net worth tracking, but they're not part of your budget. This is fine. Budget your income. Invest it. Track net worth separately.

Tax software: When April comes, you'll want to use tax software like TurboTax or TaxAct. YNAB's data can inform this (you know exactly how much you spent on business expenses or charitable giving), but YNAB doesn't replace tax software.

Debt payoff tracking: If you're using YNAB to pay off debt, you might also use a tool like Undebt.it to model different payoff strategies. YNAB tells you how much you can afford to pay. The payoff calculator tells you how long it'll take. Together, they're powerful.

Net worth tracking: Apps like Personal Capital or Net Worth track your overall financial health. You might use YNAB for budgeting and Personal Capital for net worth and investments. They're complementary.

Bill payment tools: Some people use separate apps like Truebill or Rocket Money specifically to manage subscriptions and bill reminders. YNAB can do some of this, but if you want a dedicated tool, you can use both.

Retirement planning: If you're using a tool to project retirement, you need to know your spending number. YNAB gives you that number. This is useful information for planning.

The point: YNAB is a piece of your financial system, not your entire system. Use it alongside other tools that make sense for you.

The YNAB Community and Resources

One underrated aspect of YNAB: the community.

There's an active community forum where people ask questions and share strategies. You can search for specific scenarios ("How do I budget for irregular income?" or "What do I do when I overspend a category?") and find detailed answers from experienced users and YNAB staff.

There are YouTube creators who focus on YNAB strategies. Some are official YNAB content. Some are independent creators sharing their workflows. These are incredibly valuable for seeing how experienced users structure their budgets.

There's a subreddit (r/YNAB) with thousands of active members. People share their experiences, ask questions, and celebrate milestones ("Paid off my credit card!" or "Hit my emergency fund goal!").

YNAB also hosts webinars and workshops on specific topics. Live sessions where you can ask questions in real-time.

This community aspect matters more than you might think. When you're confused or wondering if you're doing it right, having other people who've walked the same path is valuable.

Maximizing Your YNAB Investment: Pro Tips

If you're going to use YNAB, use it fully. Here are pro tips from experienced users.

Pro tip one: Use the mobile app to snap photos of receipts. The app has a camera feature where you can take a photo of a receipt. YNAB will try to OCR the amount (with varying success). Even if OCR fails, the photo is attached to the transaction as proof. This is useful at the end of the month if you need to verify something.

Pro tip two: Set up recurring transactions for everything predictable. Rent, insurance, subscriptions, regular utility payments. Let YNAB handle the repetition. You only decide about the variable stuff.

Pro tip three: Use the split feature aggressively. If a transaction belongs to multiple categories, split it. A grocery store trip might be 80% groceries, 20% home goods. Split it. Your category tracking becomes accurate.

Pro tip four: Create a "buffer" category. Most people get to the end of their first month with YNAB and realize they overspent in a few categories. This is normal. Create a buffer category and put $50 in it every month for the first few months. When you overspend, you pull from the buffer instead of panicking. As you get better at budgeting, the buffer shrinks.

Pro tip five: Review your budget monthly, not daily. Check it daily to see balances. But review it monthly—actually think about categories, adjust based on actual spending, and plan for next month. This monthly review is where insights happen.

Pro tip six: Tag your transactions strategically. YNAB lets you add tags to transactions. You can tag "business meal" or "emergency" or "gift." Later, you can filter by tags to see spending patterns. This is optional but powerful.

Pro tip seven: Celebrate wins. Came in under budget in a category? Celebrate. Paid off a debt? Celebrate. Built your emergency fund to three months of expenses? Celebrate. YNAB is a long game. You need momentum.

Future of YNAB: What's Coming

YNAB is actively developing. The product roadmap includes new features, but they're cautious about scope creep. They don't want to become a financial superapp. They want to stay the best budgeting app.

Some likely developments: improved reporting and customization, better mobile capabilities, more sophisticated goal-setting, and expanded integrations with other financial tools. But YNAB's philosophy is that good budgeting solves most financial problems. They're not trying to replace investing platforms or retirement calculators. They're trying to be the best at helping you budget.

One thing I'd like to see: lower pricing tiers or a lite version. For students or very low-income users,

FAQ

What is YNAB and how is it different from regular budgeting apps?

YNAB (You Need A Budget) is a budgeting application built on the "give every dollar a job" philosophy. Unlike apps that track where you've already spent money, YNAB teaches you to allocate money intentionally before you spend it. You log your available money, assign it to categories (rent, groceries, entertainment, etc.), and then spend from those allocated amounts. This proactive approach changes spending behavior, whereas most budgeting apps take a reactive approach by showing you spending after the fact. YNAB's methodology is based on decades of proven envelope budgeting principles.

How much money can I save using YNAB?

The average YNAB user saves approximately $6,000 in their first year, according to YNAB's own data. However, actual savings depend on your specific situation. If you spend money without visibility, have debt, or struggle with impulse purchases, YNAB will likely generate significant savings. If you're already highly disciplined with money, the savings might be smaller. The primary value is behavioral change and financial awareness, not just spending reduction. Even users who don't dramatically cut expenses report reduced financial stress and improved control.

Is YNAB worth the $12.99 per month cost?

For most people, YNAB pays for itself within the first month through behavioral changes and reduced unnecessary spending. At

How long does it take to learn YNAB?

Most people reach functional competence within 2-4 weeks. Weeks one and two are confusing as you set up categories and log transactions. By week three, the system usually clicks and you see immediate value. The free trial lasts 34 days, which is strategically designed to give you enough time to get past the initial learning phase and see if the methodology works for you. Some users benefit from watching YNAB's educational videos (4-5 minutes each) before starting, which can accelerate understanding.

Does YNAB work if I have irregular or variable income?

Yes, YNAB actually excels for people with variable income. Instead of assuming the same income each month, you budget based on actual money received. In good months, you allocate more. In slow months, you use money set aside from previous months. This is one of YNAB's strongest use cases. Freelancers, commission-based workers, and business owners often report that YNAB gives them stability despite income variability because it smooths out cash flow and prevents overspending in low-income months.

Can I use YNAB with a partner or spouse?

Absolutely. YNAB supports multiple users on a single account. Both partners can access and update the budget from their phones or computers. Many couples report that YNAB forces necessary conversations about financial priorities ("How much should we spend on entertainment versus savings?") and provides transparency so there are no surprises. The app syncs in real-time, so both partners always see the same numbers. This removes the friction of "I didn't know you spent that" arguments.

What happens if I overspend a category in YNAB?

You "roll with the punches," which is YNAB's term for adjusting when life happens. If you overspend groceries by $50, you move money from another category to cover it. This isn't a failure; it's a reality check. You see the trade-off immediately. Maybe you reduce entertainment spending for the month, or you postpone a non-urgent purchase. The key is that you're making the decision consciously, not discovering a problem at the end of the month. Some users create a "buffer" category specifically to cover overages while they're learning.

Is my financial data secure with YNAB?

YNAB uses bank-level encryption and doesn't store your bank login credentials. When you connect your bank account, a third-party service called Plaid manages the secure connection, which is industry standard. YNAB's subscription business model means they have no incentive to sell your data to advertisers or marketers, unlike free budgeting apps. You can enable two-factor authentication on your account for additional security. Your data is stored in US-based servers, which is worth noting if you have GDPR or privacy concerns.

What are the best alternatives to YNAB?

The main alternatives depend on your priorities. Every Dollar uses similar methodology to YNAB and is free with limitations. Goodbudget is free, uses a virtual envelope system, and works well for couples, but requires manual transaction entry. Rocket Money focuses on bill and subscription management alongside budgeting. Monarch Money is a newer platform that combines budgeting, net worth tracking, and investing in one place. For simplicity and lower cost, spreadsheet-based budgeting works if you're disciplined. The trade-off is that YNAB automates syncing and calculations that spreadsheets require manually.

Can YNAB help me pay off debt faster?

Yes, and this is one of YNAB's primary strengths for people with debt. You set a goal for debt reduction and YNAB calculates exactly how much to allocate each month to pay off the debt by a target date. For example, if you have a

How does YNAB handle one-time and irregular expenses?

YNAB's solution is the "true expenses" category. You identify all your annual or irregular expenses (car insurance, property taxes, annual subscriptions, medical deductibles, gifts, etc.), calculate the total, and divide by twelve. You set aside that amount monthly. When the bill arrives, the money is already there. This prevents the panic of unexpected large expenses and the false sense of having "extra" money in a month when an annual bill doesn't hit. This feature alone justifies YNAB's cost for many users because it eliminates cash flow surprises.

Conclusion: Is YNAB Right for You?

YNAB isn't magic. It's not going to make you rich. It won't eliminate financial stress if you're dealing with serious debt or income instability.

But it will do something profound: it will give you control.

For eighteen months, I've logged transactions, adjusted budgets, hit targets, and occasionally overspent and had to roll with the punches. The net effect is that money is no longer a mystery. I know where it goes. I choose where it goes. I sleep better because of that control.

That's the real value proposition. Not savings, though savings happen. Not features, though the app is well-built. But the fundamental shift from "I don't know what happened to my money" to "I decided where my money went."

If that resonates with you, if you've ever been shocked by your bank balance, if you want to pay off debt faster, if you want to build savings but don't know how, YNAB is worth trying.

Use the free trial. Give it four weeks. Don't evaluate it after four days. Let the system work. Watch your behavior change. See what becomes visible.

If it clicks, it's $155/year for something that could change your financial life. If it doesn't click, you've spent nothing and lost a bit of time. But most people who actually engage with YNAB for four weeks find that it clicks. The methodology is proven. The tool is solid. The only question is whether you'll commit to using it.

The answer to that question determines everything.

Ready to take control of your finances? Start your free 34-day trial of YNAB and experience the budgeting methodology that's changed millions of people's financial lives. No credit card required. Just honest budgeting and real control.

Key Takeaways

- YNAB's "give every dollar a job" methodology forces intentional spending decisions before money leaves your account, fundamentally changing financial behavior

- Average users save $6,000+ in their first year—not through deprivation, but through visibility and conscious choice about priorities

- Learning curve takes 2-4 weeks, but most users see immediate value by week three when the system clicks and behavioral changes begin

- At 155 annually), YNAB typically pays for itself in savings within the first month for most users

- YNAB excels for specific situations: impulse spenders, people with debt, variable income earners, and couples who need financial transparency

- Bank syncing, mobile access, and psychological design create accountability that spreadsheets and free apps lack

- Privacy is solid (bank-level encryption, subscription-based revenue model), and data security follows industry standards

Related Articles

- Best Budgeting Apps: Monarch Money 50% Off Deal [2025]

- Monarch Money Budgeting App: $50/Year Deal + Complete Review [2025]

- Monarch Money Deal: $50 for One Year (50% Off) [2025]

- Monarch Money Annual Deal: Save 50% on Premium Budgeting [2025]

- Monarch Money 50% Off Deal: Complete Guide to Annual Budgeting [2025]

- Best Budgeting Apps 2025: Complete Guide After Mint Shutdown